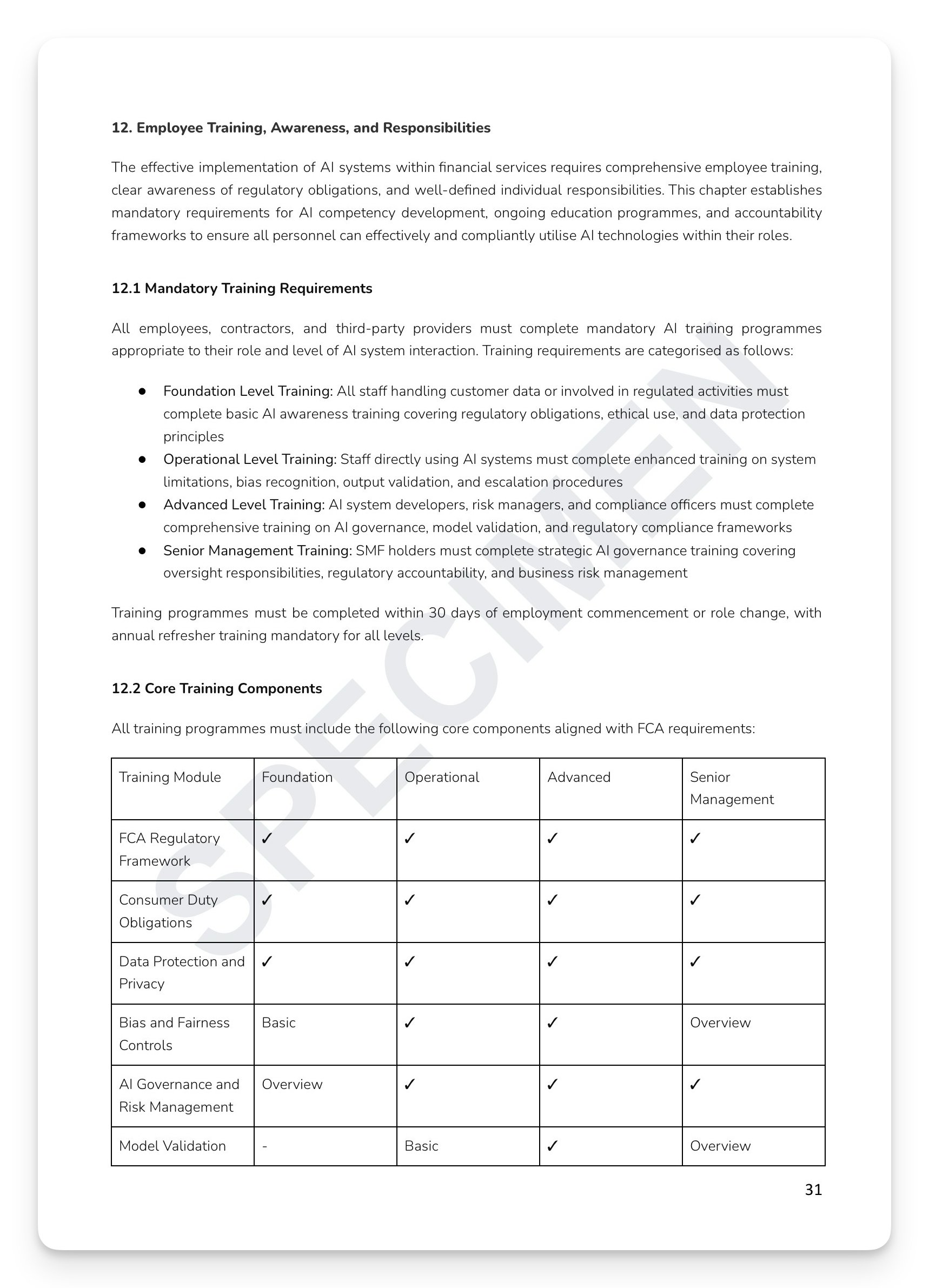

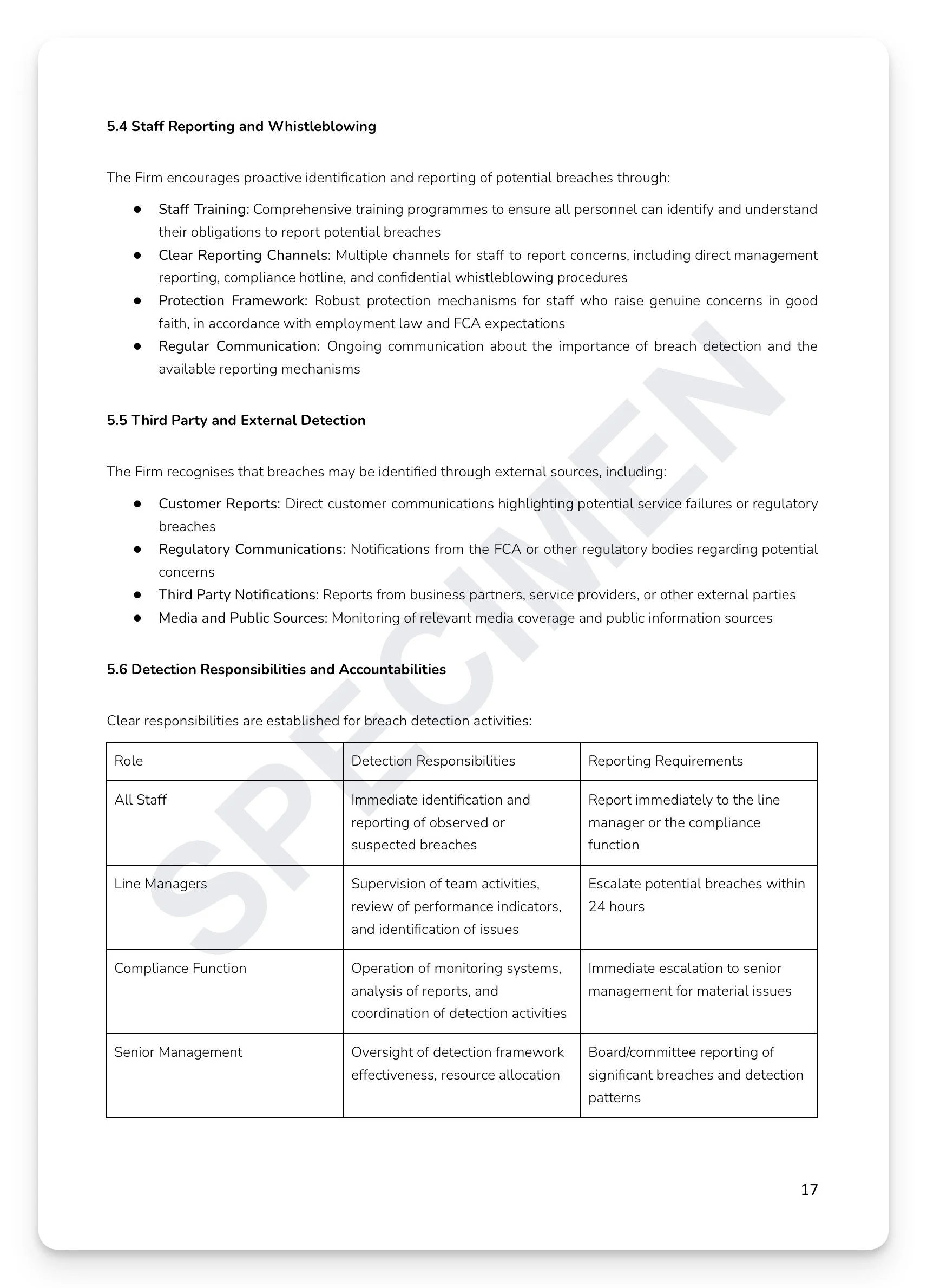

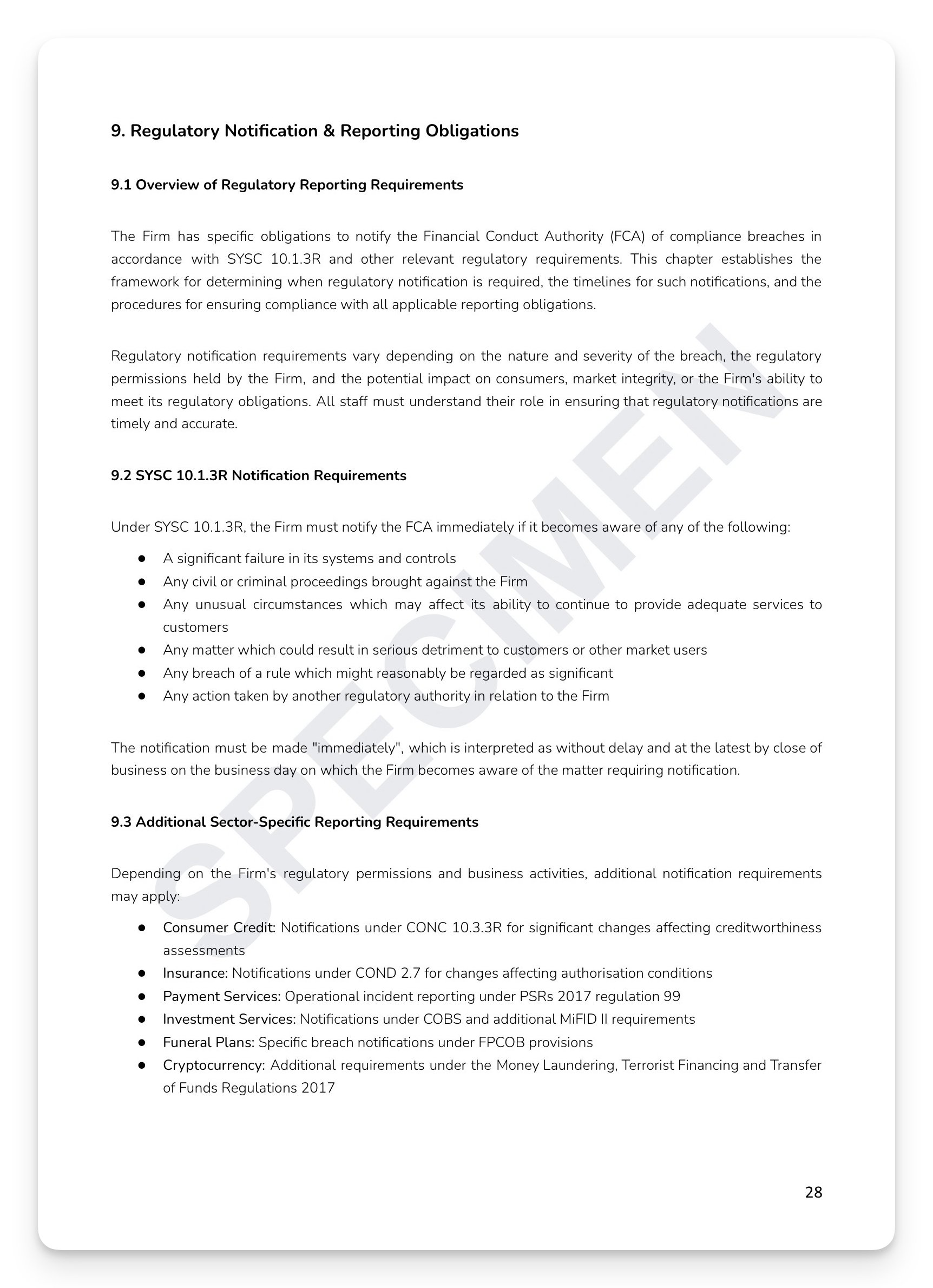

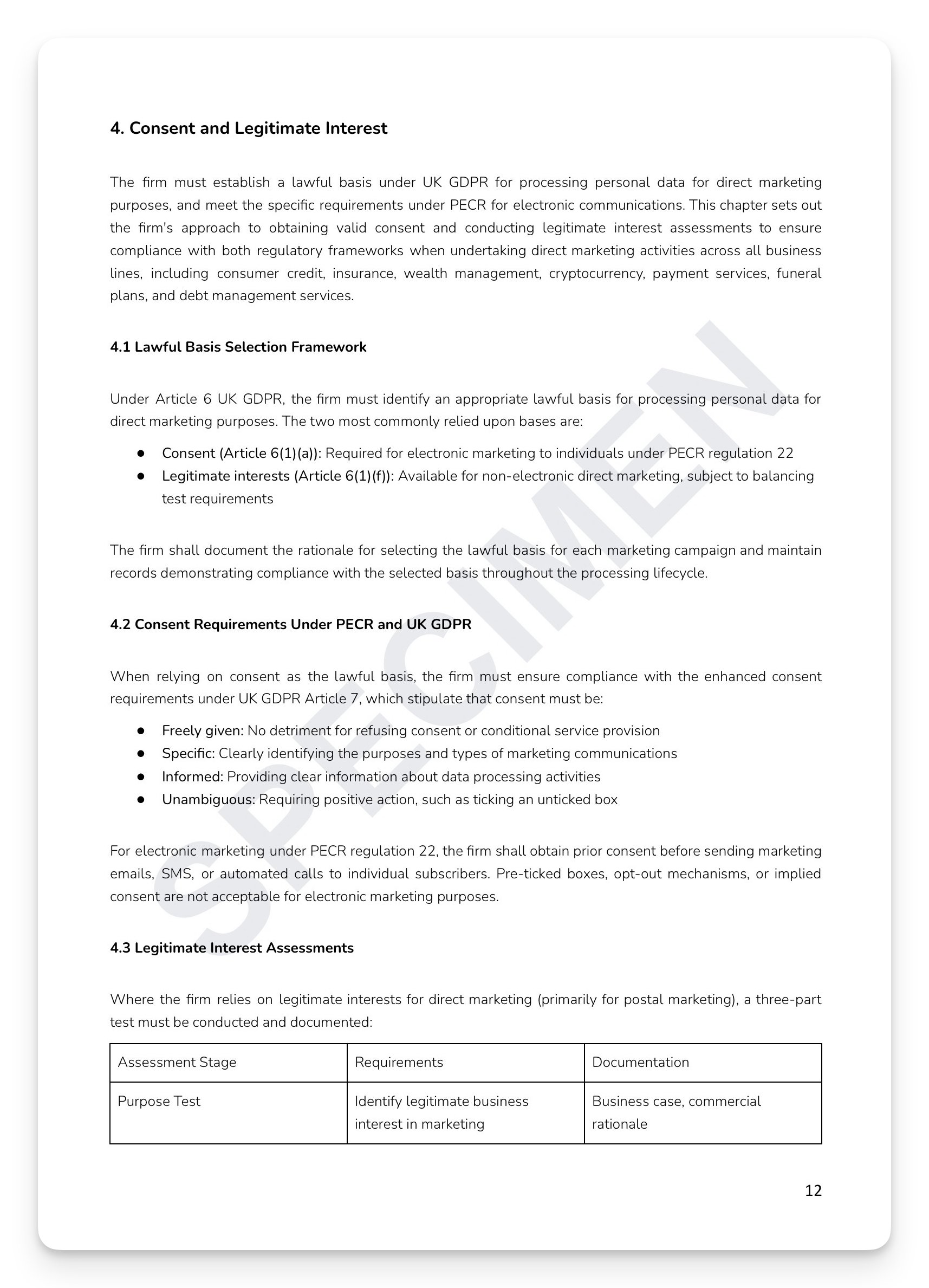

Distance marketing is one of the highest-risk customer touchpoints for FCA-regulated firms. Without a physical interaction, pre-contractual disclosures can be missed or buried, vulnerability is harder to spot, cancellation rights are easily obscured, and the absence of a paper trail creates acute regulatory exposure. The Consumer Contracts Regulations 2013, COBS 5.1, CONC 2.7, ICOBS, and Consumer Duty all impose specific distance marketing obligations layered on top of each other — each with their own timing requirements, content standards, and channel-specific rules. A telephone call that makes a sale without confirming cancellation rights isn't just bad practice — it's a breach. Distance marketing without documented controls isn't a compliance gap. It's an open enforcement door.

What's included:

Full regulatory mapping: Consumer Contracts Regulations 2013, COBS 4.2.1R/5.1/6/15.2–15.4, CONC 2.7/3.3.1R/11.2, ICOBS 2/6/7.1, PSR 2017, Consumer Duty PS22/9, SYSC 6.1/9, and PECR

Five approved channel framework: telephone (CLI mandatory/script approval/call recording/5-year retention), electronic (PECR consent/unsubscribe/timing restrictions), digital platforms (COBS 4.5/mobile security/social media pre-approval), direct mail (MPS compliance), and video conferencing

Mandatory pre-contractual information matrix across five product categories: Consumer Credit, Insurance, Investment, Payment Services, and Funeral Plans — each with sector-specific disclosure requirements

Four-stage vulnerable customer framework: data screening, initial contact assessment, ongoing monitoring, and specialist referral — aligned to Consumer Duty four outcomes

Five-tier cancellation rights matrix: Investment, Consumer Credit, Insurance, Payment Services, and Funeral Plans — all 14 days with sector-specific regulatory reference

Three-tier dispute resolution: immediate front-line, formal 8-week DISP process, and FOS referral

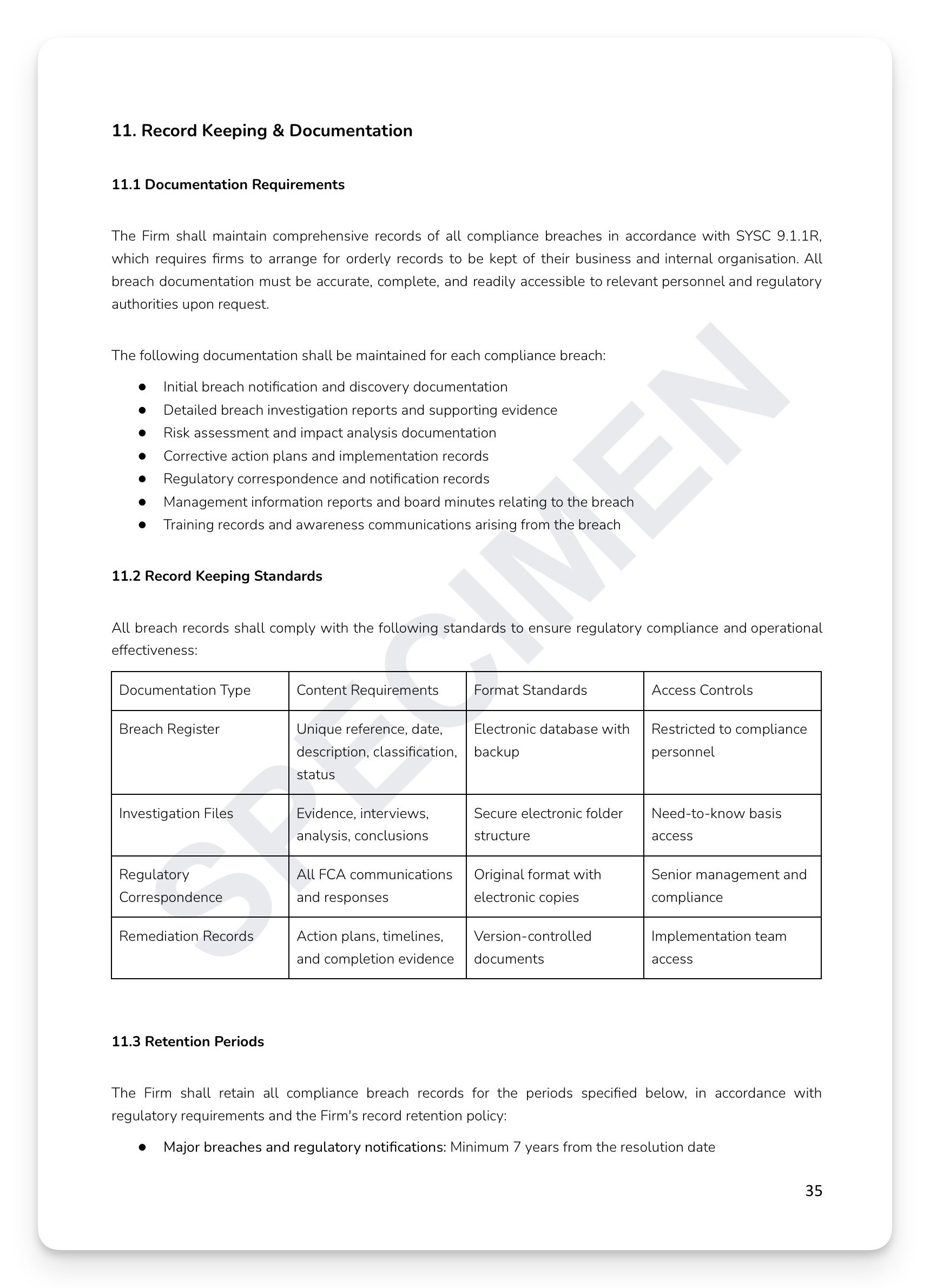

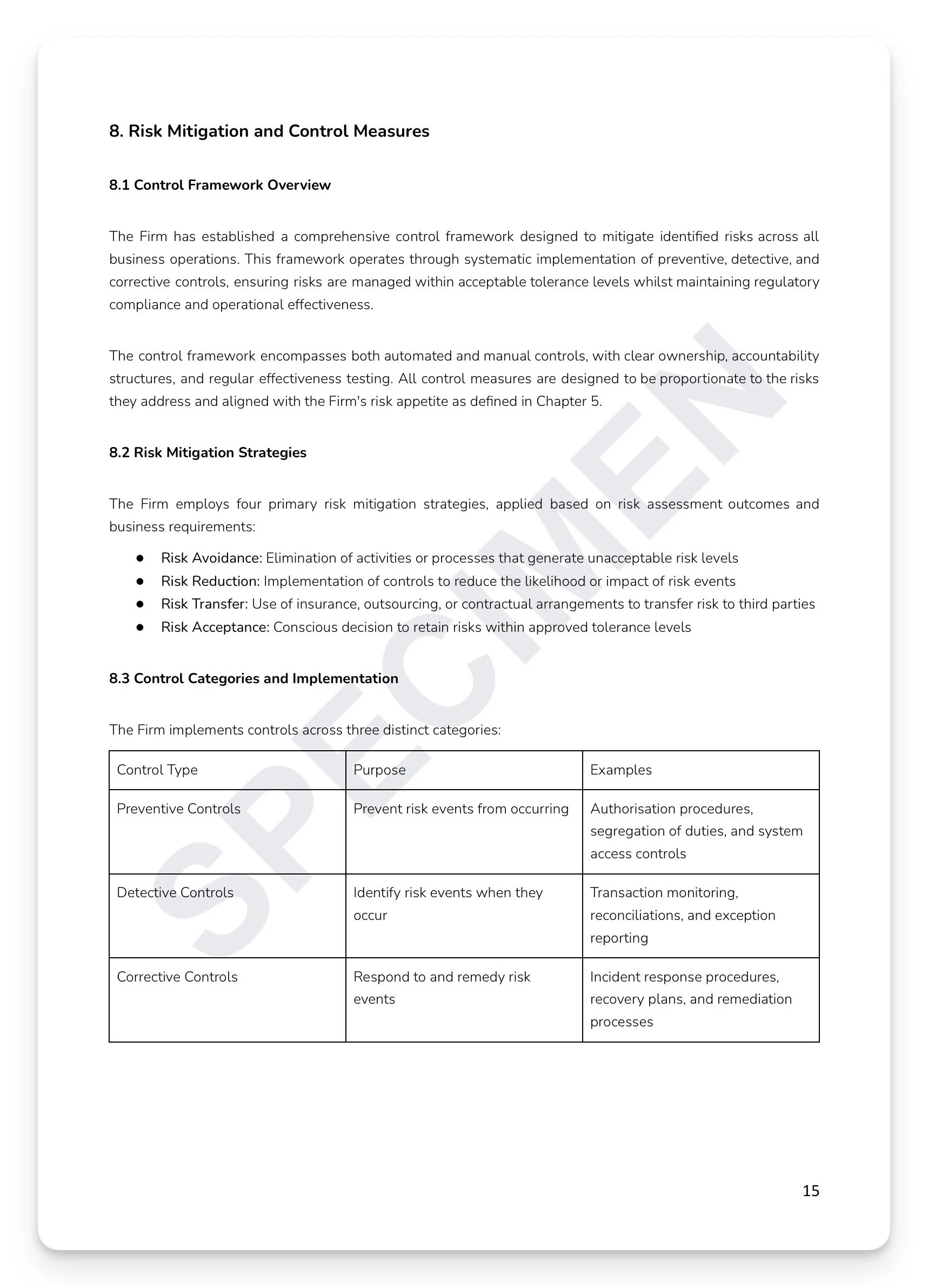

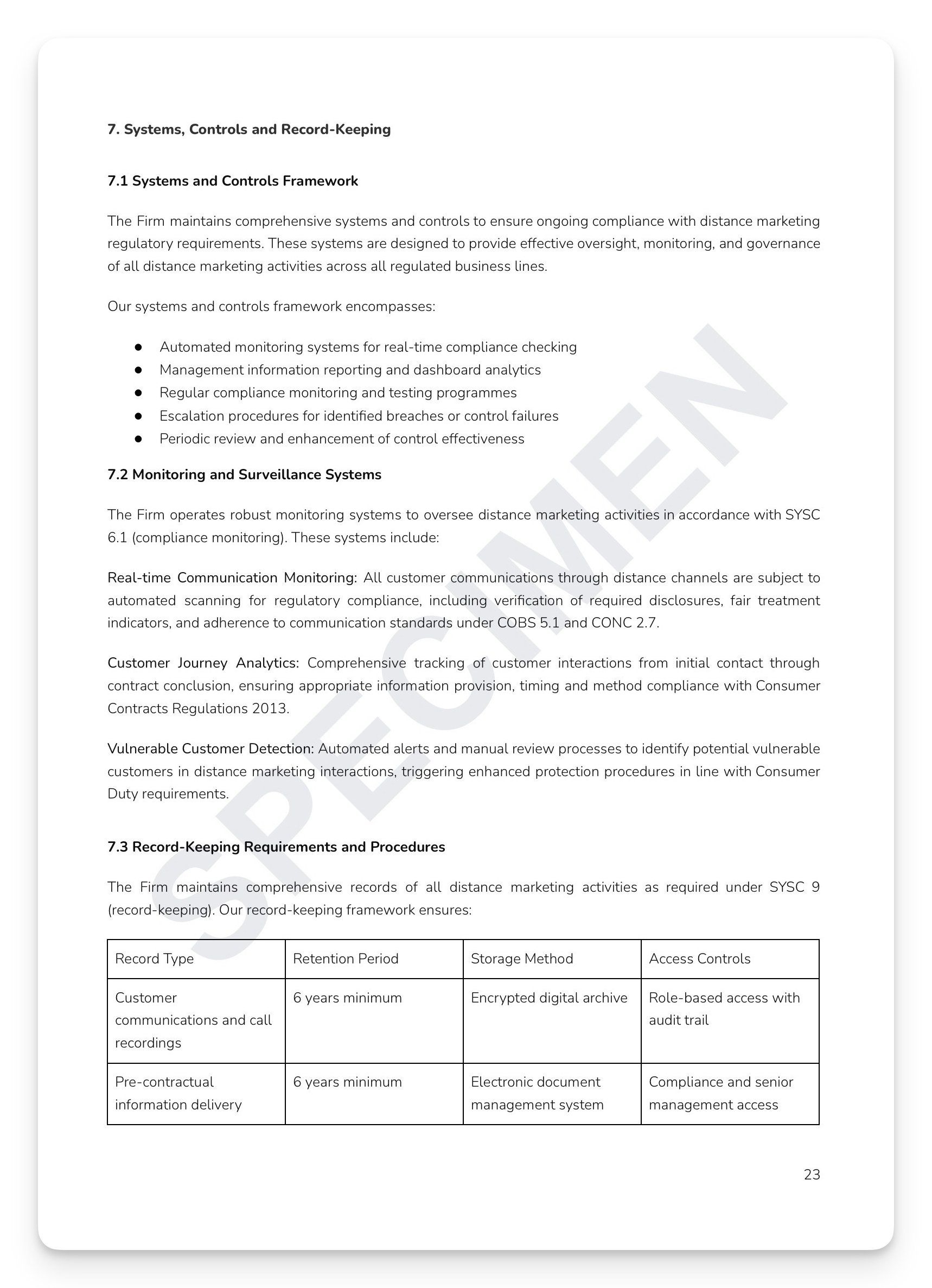

Record retention schedule: customer communications and call recordings (6 years), financial promotions (3 years), and training records (3 years post-employment) + much more

Who is this for?

Compliance Officers, SMF holders, Marketing Directors, and operational managers at FCA-regulated firms conducting any form of remote customer acquisition or servicing who need a complete, board-approved Distance Marketing Policy satisfying the intersecting obligations of the Consumer Contracts Regulations, FCA conduct rules, and sector-specific sourcebooks.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Distance marketing is one of the highest-risk customer touchpoints for FCA-regulated firms. Without a physical interaction, pre-contractual disclosures can be missed or buried, vulnerability is harder to spot, cancellation rights are easily obscured, and the absence of a paper trail creates acute regulatory exposure. The Consumer Contracts Regulations 2013, COBS 5.1, CONC 2.7, ICOBS, and Consumer Duty all impose specific distance marketing obligations layered on top of each other — each with their own timing requirements, content standards, and channel-specific rules. A telephone call that makes a sale without confirming cancellation rights isn't just bad practice — it's a breach. Distance marketing without documented controls isn't a compliance gap. It's an open enforcement door.

What's included:

Full regulatory mapping: Consumer Contracts Regulations 2013, COBS 4.2.1R/5.1/6/15.2–15.4, CONC 2.7/3.3.1R/11.2, ICOBS 2/6/7.1, PSR 2017, Consumer Duty PS22/9, SYSC 6.1/9, and PECR

Five approved channel framework: telephone (CLI mandatory/script approval/call recording/5-year retention), electronic (PECR consent/unsubscribe/timing restrictions), digital platforms (COBS 4.5/mobile security/social media pre-approval), direct mail (MPS compliance), and video conferencing

Mandatory pre-contractual information matrix across five product categories: Consumer Credit, Insurance, Investment, Payment Services, and Funeral Plans — each with sector-specific disclosure requirements

Four-stage vulnerable customer framework: data screening, initial contact assessment, ongoing monitoring, and specialist referral — aligned to Consumer Duty four outcomes

Five-tier cancellation rights matrix: Investment, Consumer Credit, Insurance, Payment Services, and Funeral Plans — all 14 days with sector-specific regulatory reference

Three-tier dispute resolution: immediate front-line, formal 8-week DISP process, and FOS referral

Record retention schedule: customer communications and call recordings (6 years), financial promotions (3 years), and training records (3 years post-employment) + much more

Who is this for?

Compliance Officers, SMF holders, Marketing Directors, and operational managers at FCA-regulated firms conducting any form of remote customer acquisition or servicing who need a complete, board-approved Distance Marketing Policy satisfying the intersecting obligations of the Consumer Contracts Regulations, FCA conduct rules, and sector-specific sourcebooks.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7