The single biggest reason FCA applications fail, stall, or get returned isn't a missing document or an incorrect form — it's an inadequate Regulatory Business Plan. The RBP is the centrepiece of every Connect submission, where the FCA assesses whether your firm genuinely understands what it's applying to do, whether your governance and controls are real or aspirational, and whether the people running the firm are fit to hold the permissions they're requesting. A thin, generic RBP signals the FCA that a firm isn't ready. A comprehensive, well-evidenced RBP signals the opposite — and materially increases the probability of first-time approval without information requests or delays that can set an application back by months.

What's included:

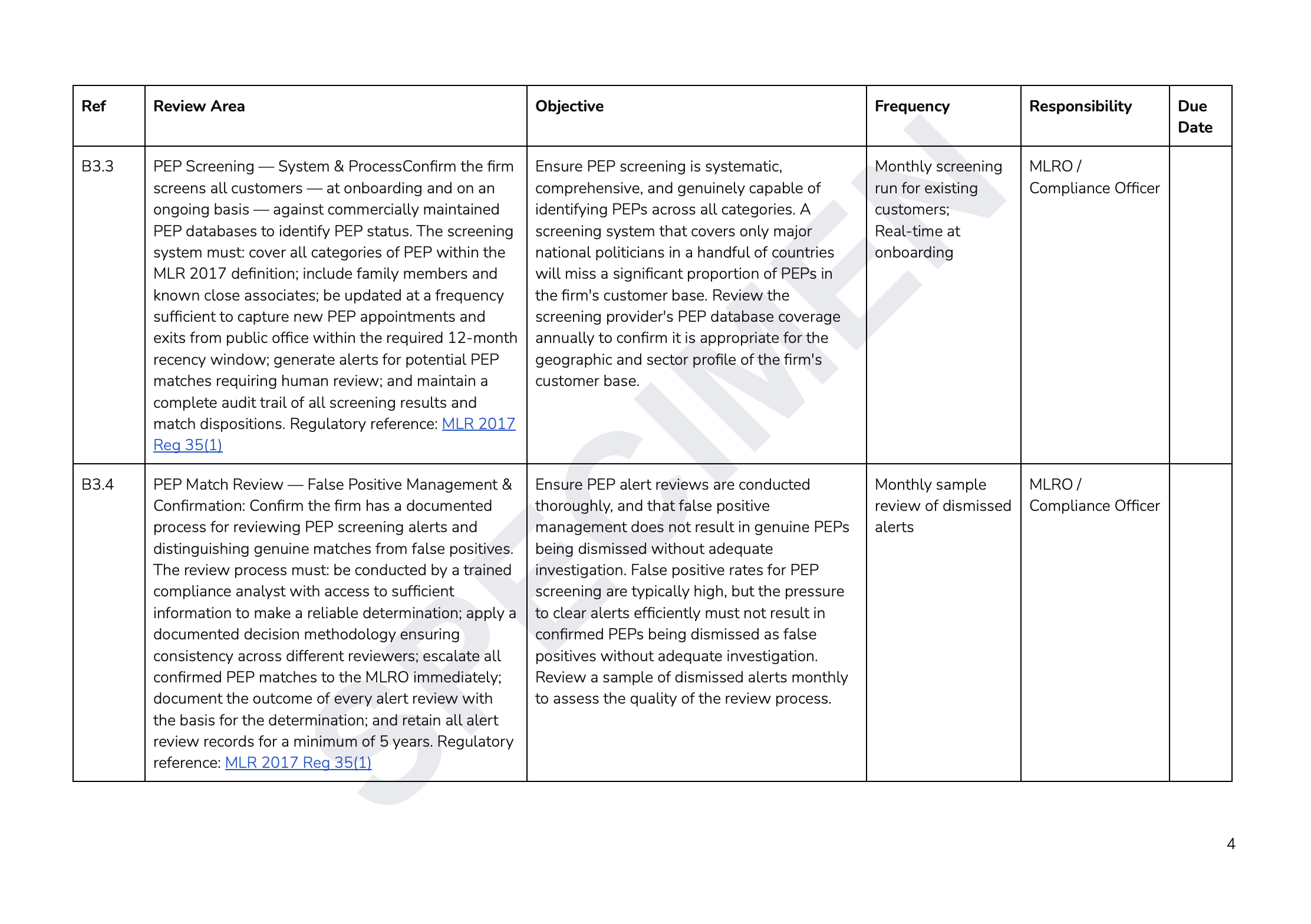

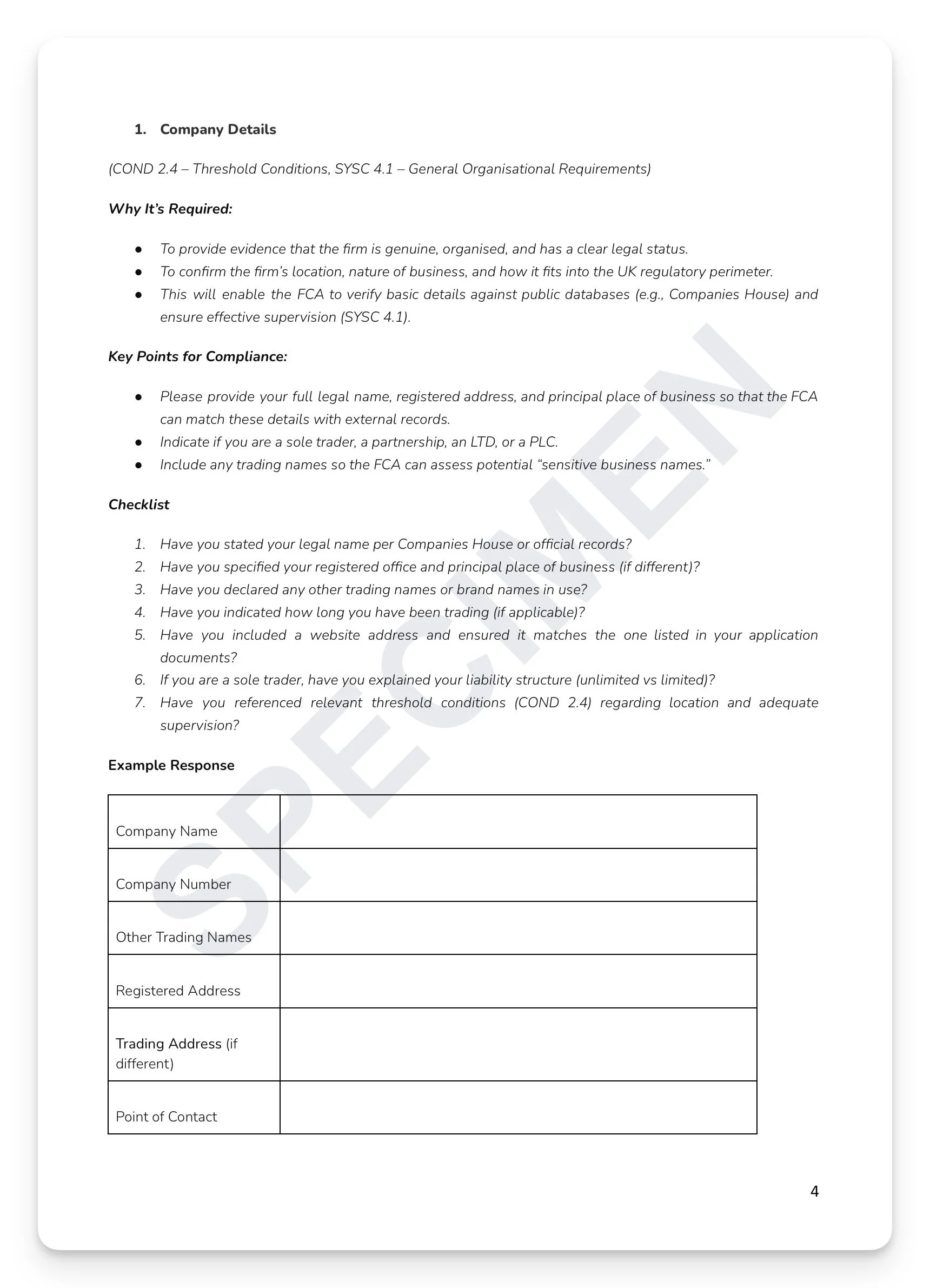

Full regulatory grounding: COND 2.4 & 2.7, SYSC 3.2/4.1/5.1/6.1/8, SUP 10C, FIT 2, COBS 4.1, PRIN 2, DISP 1, and Consumer Duty PS22/9

Company structure and financials: ownership and controllers above 10%, group structure diagram, three-year financial projections, capital adequacy, liquidity buffers, and CASS treatment where applicable

Key personnel: SUP 10C SMF schedule covering SMF16, SMF17, and SMF3 — with qualifications, experience, and supervision arrangements per role

Business model: regulated vs non-regulated activities, target market, revenue model, five-dimension risk identification with mitigation strategies, Consumer Duty embedding, and COND 2.7 viability narrative

Customer journey: full lifecycle mapping from lead generation through onboarding, advice, disclosure, vulnerability identification, after-sales, complaints, and financial promotions approval

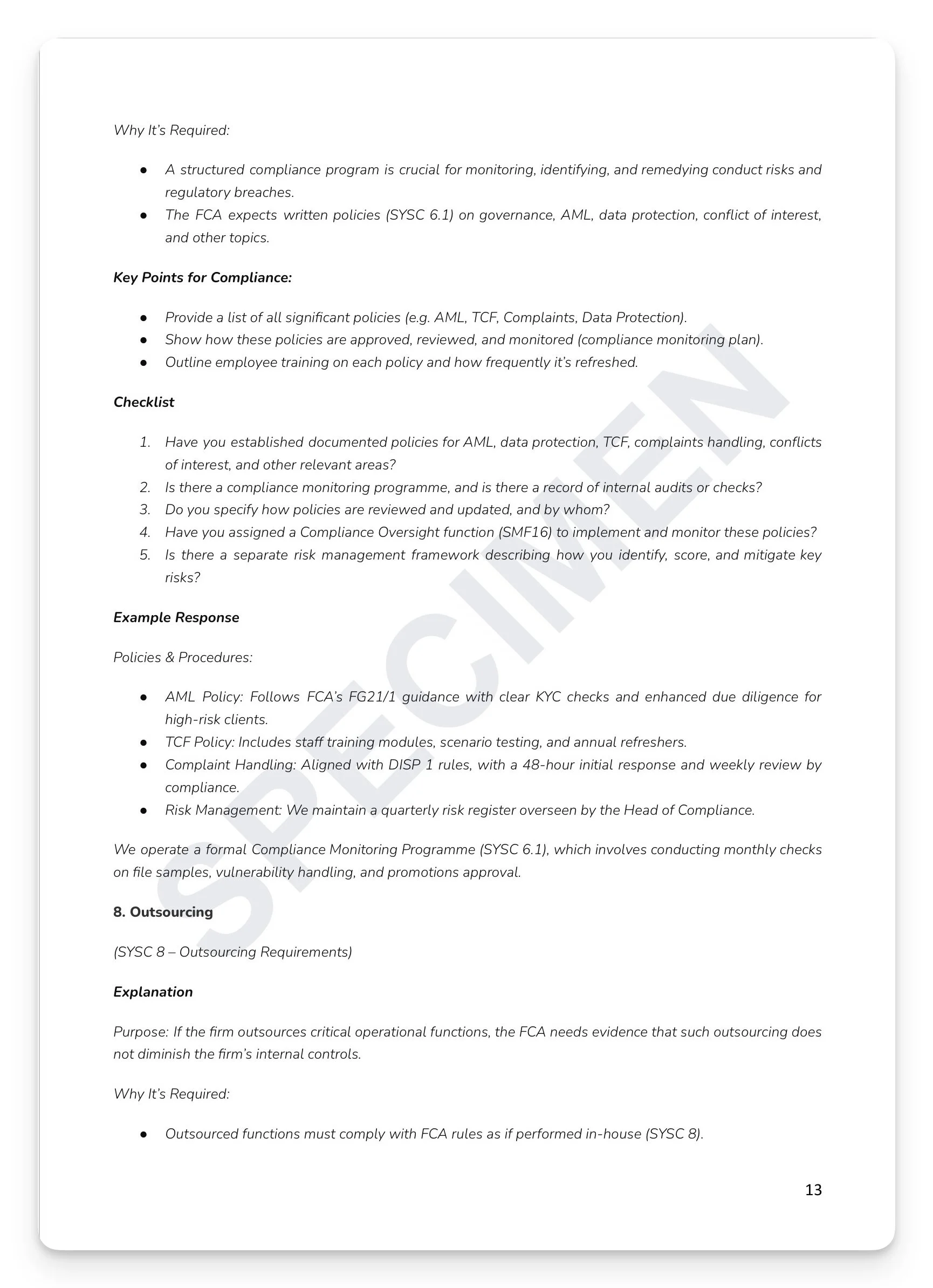

Compliance programme: policy register covering AML, TCF, complaints, data protection, conflicts, and SM&CR — with monitoring programme under SYSC 6.1 and SMF16 accountability

For every section: FCA assessment criteria explained, compliance checklist with evidential requirements, worked example at the standard the FCA expects, and common rejection reasons identified and addressed

+ much more

Who is this for?

Firms seeking initial FCA authorisation across all regulated sectors, existing authorised firms pursuing Variations of Permission, compliance consultants preparing applications on behalf of clients, and newly-appointed SMF holders preparing for Connect submission.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

The single biggest reason FCA applications fail, stall, or get returned isn't a missing document or an incorrect form — it's an inadequate Regulatory Business Plan. The RBP is the centrepiece of every Connect submission, where the FCA assesses whether your firm genuinely understands what it's applying to do, whether your governance and controls are real or aspirational, and whether the people running the firm are fit to hold the permissions they're requesting. A thin, generic RBP signals the FCA that a firm isn't ready. A comprehensive, well-evidenced RBP signals the opposite — and materially increases the probability of first-time approval without information requests or delays that can set an application back by months.

What's included:

Full regulatory grounding: COND 2.4 & 2.7, SYSC 3.2/4.1/5.1/6.1/8, SUP 10C, FIT 2, COBS 4.1, PRIN 2, DISP 1, and Consumer Duty PS22/9

Company structure and financials: ownership and controllers above 10%, group structure diagram, three-year financial projections, capital adequacy, liquidity buffers, and CASS treatment where applicable

Key personnel: SUP 10C SMF schedule covering SMF16, SMF17, and SMF3 — with qualifications, experience, and supervision arrangements per role

Business model: regulated vs non-regulated activities, target market, revenue model, five-dimension risk identification with mitigation strategies, Consumer Duty embedding, and COND 2.7 viability narrative

Customer journey: full lifecycle mapping from lead generation through onboarding, advice, disclosure, vulnerability identification, after-sales, complaints, and financial promotions approval

Compliance programme: policy register covering AML, TCF, complaints, data protection, conflicts, and SM&CR — with monitoring programme under SYSC 6.1 and SMF16 accountability

For every section: FCA assessment criteria explained, compliance checklist with evidential requirements, worked example at the standard the FCA expects, and common rejection reasons identified and addressed

+ much more

Who is this for?

Firms seeking initial FCA authorisation across all regulated sectors, existing authorised firms pursuing Variations of Permission, compliance consultants preparing applications on behalf of clients, and newly-appointed SMF holders preparing for Connect submission.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 5

Image 1 of 5

Image 2 of 5

Image 2 of 5

Image 3 of 5

Image 3 of 5

Image 4 of 5

Image 4 of 5

Image 5 of 5

Image 5 of 5