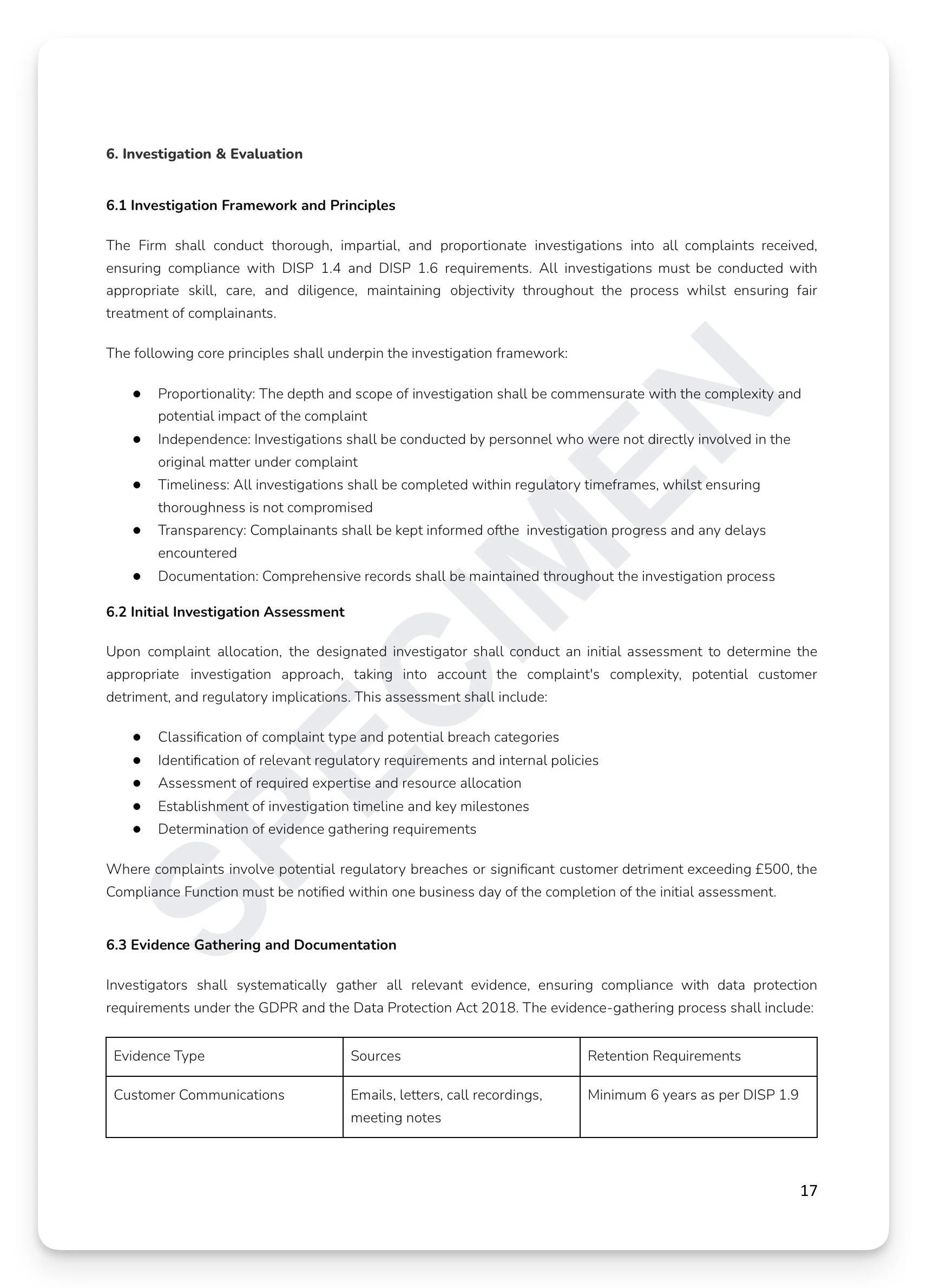

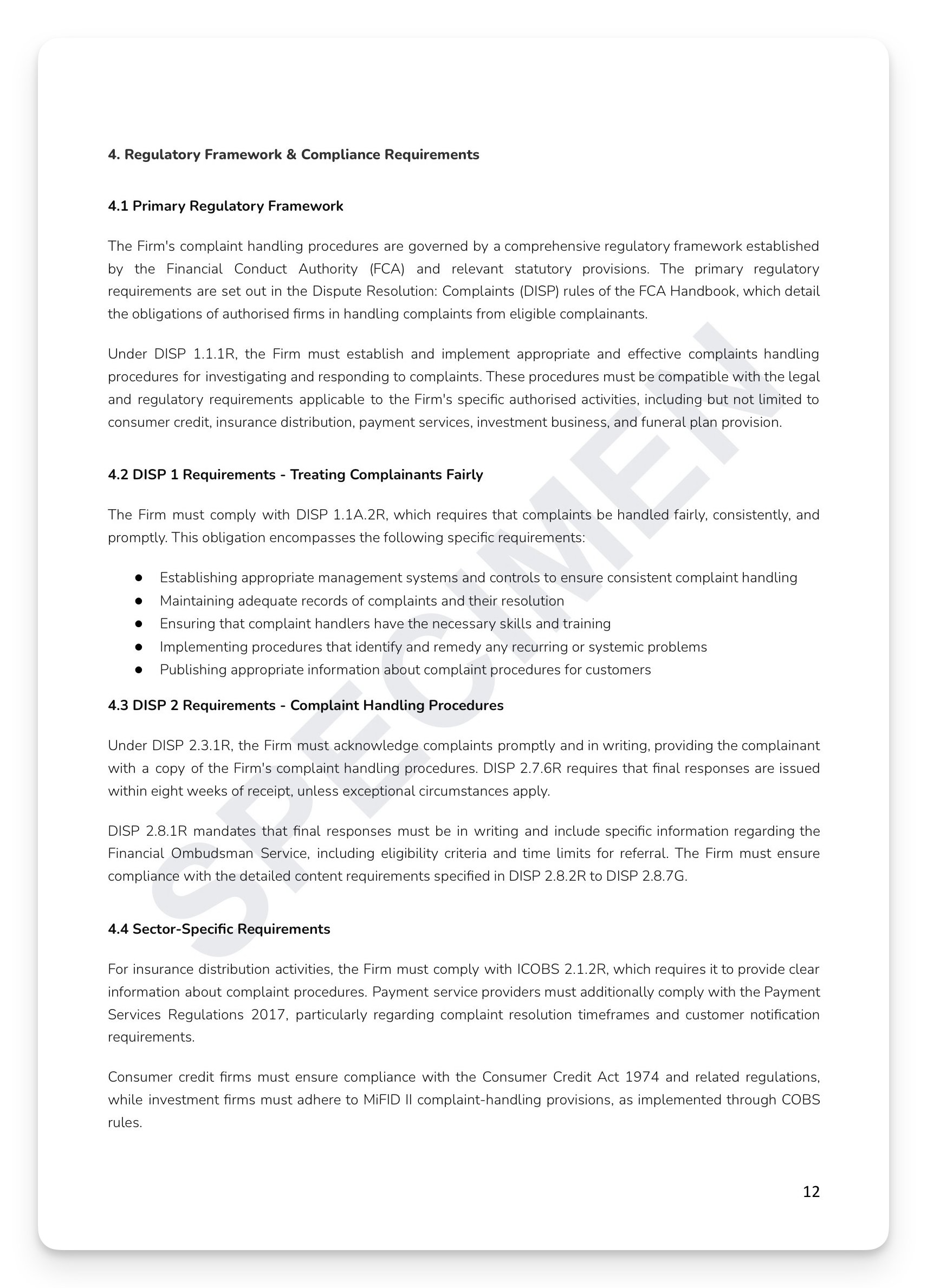

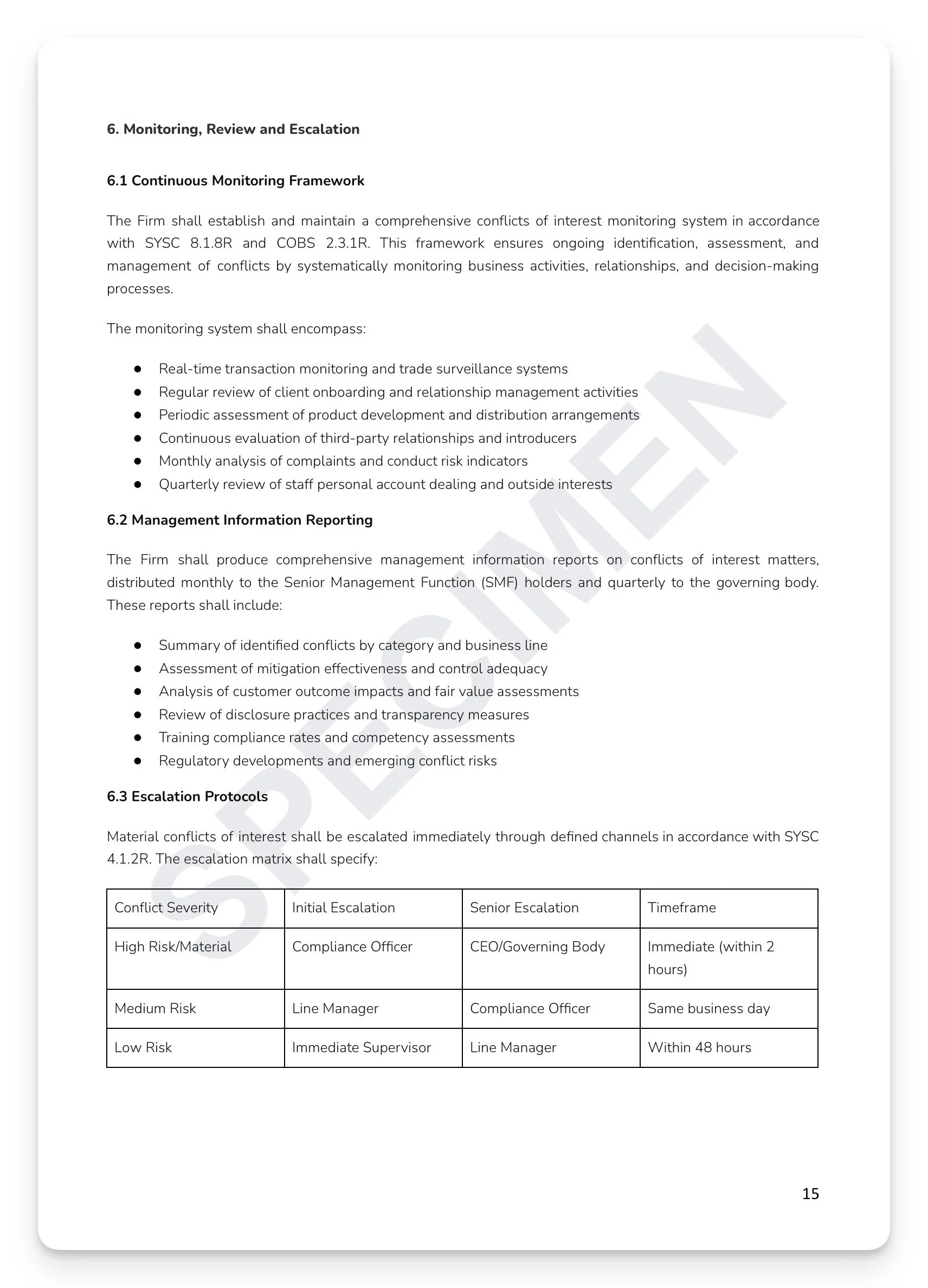

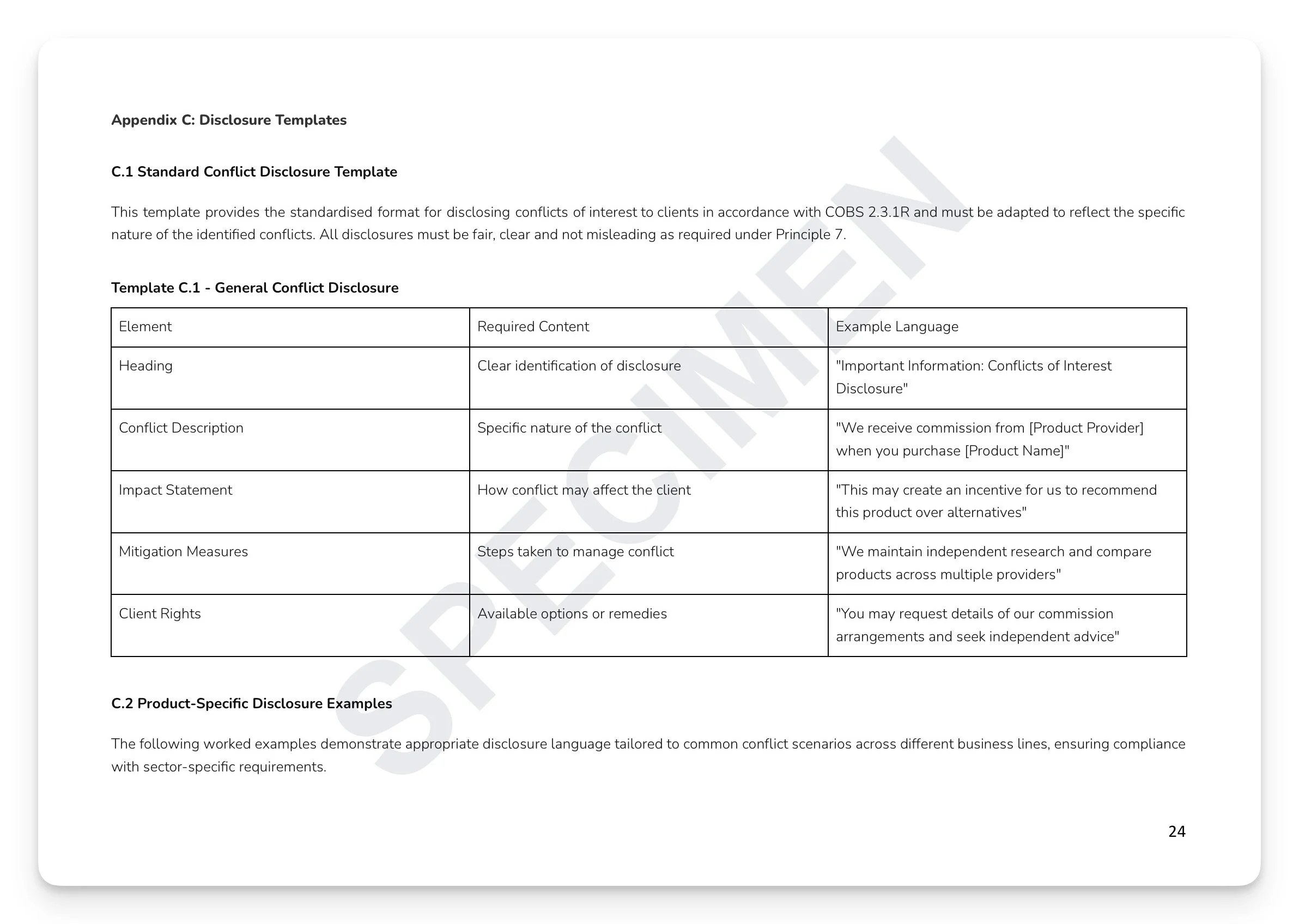

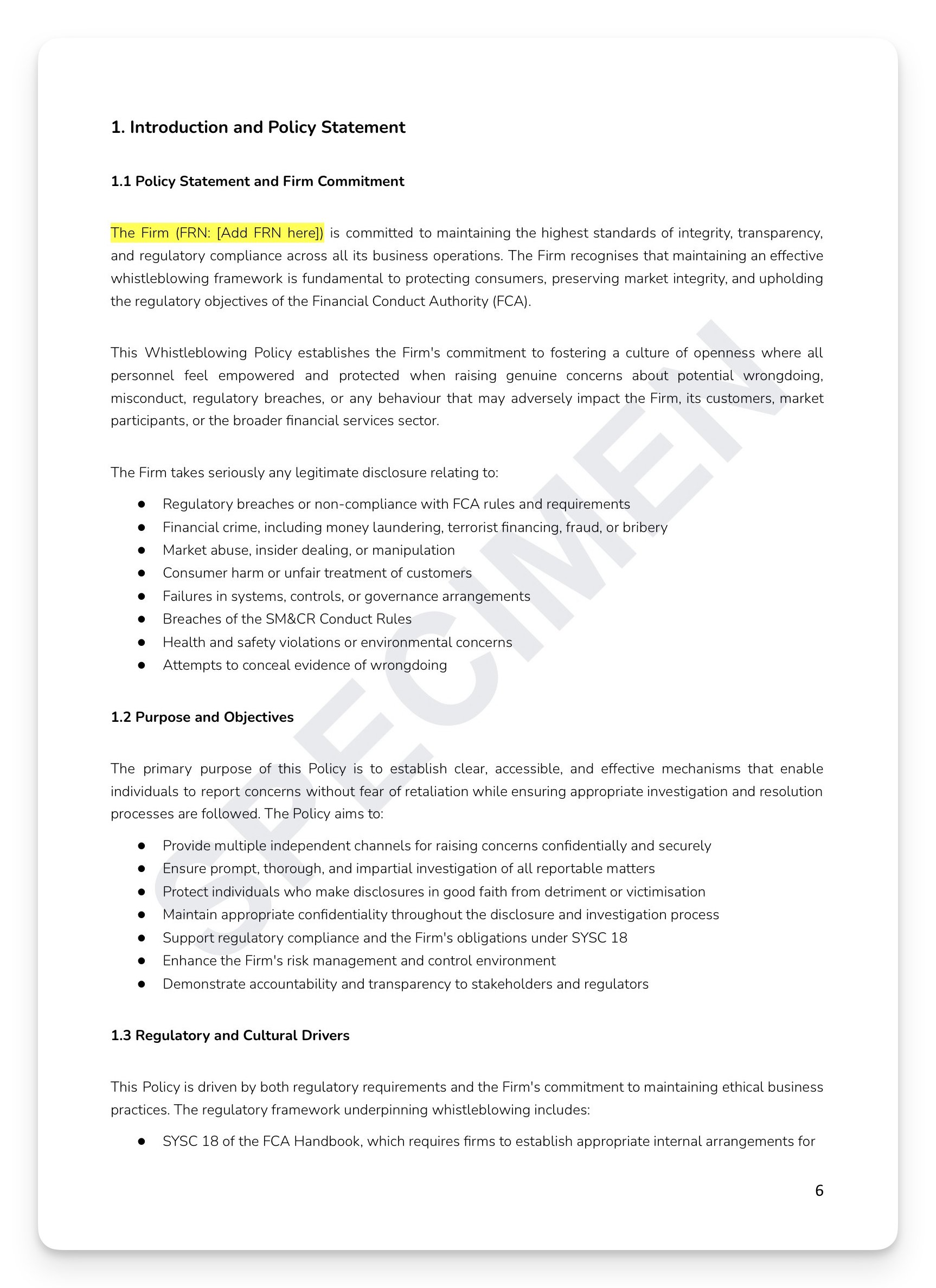

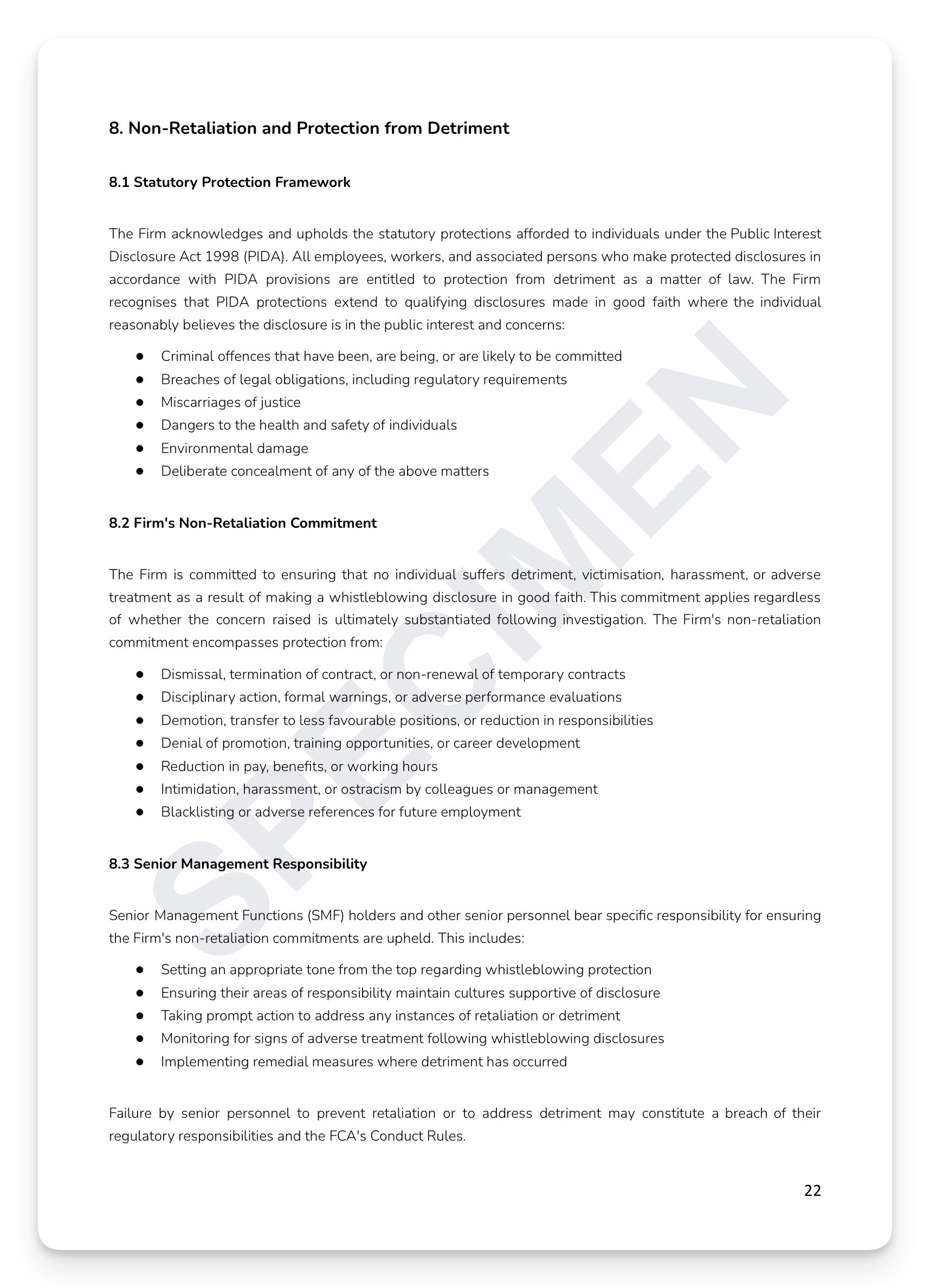

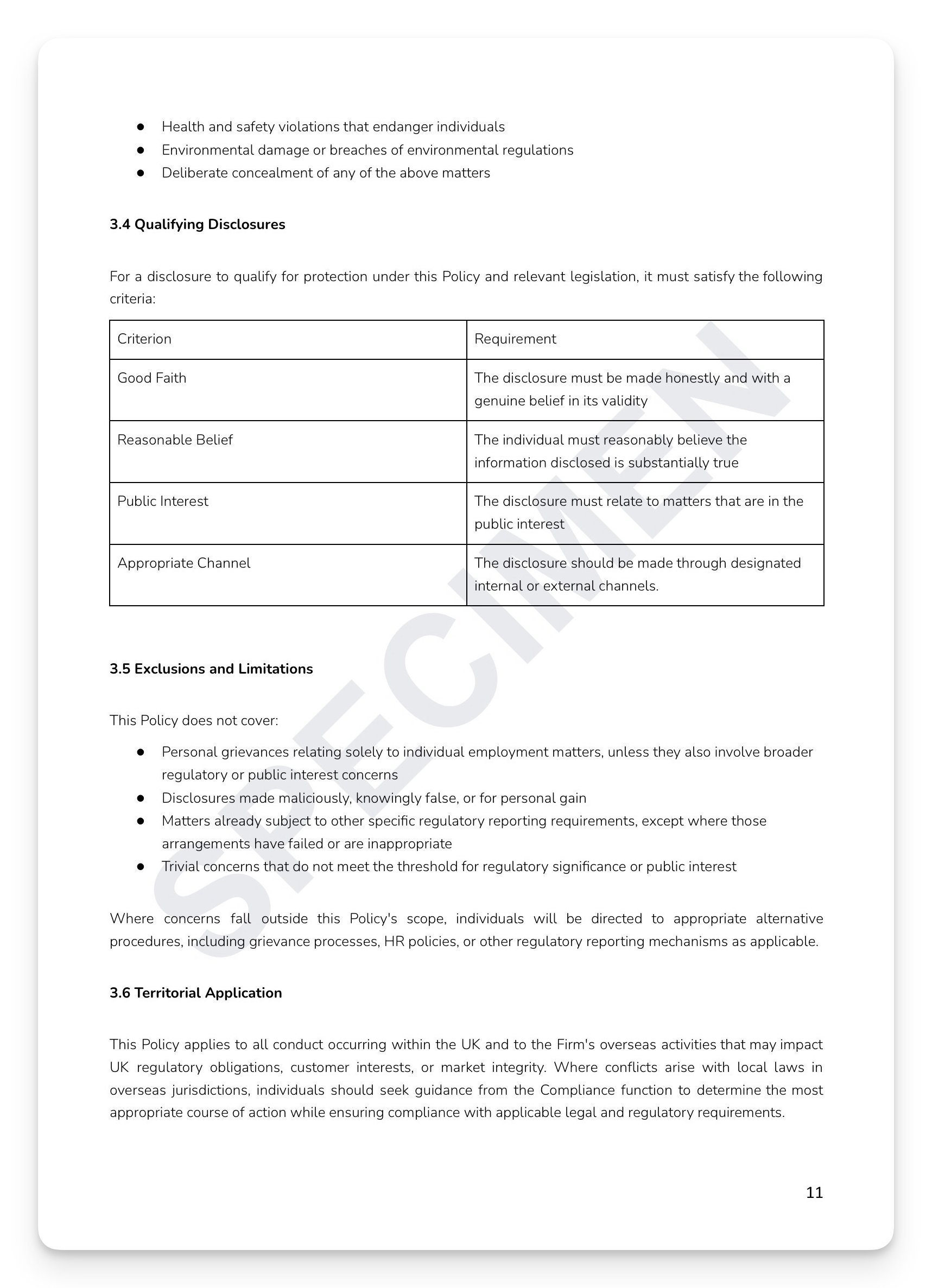

Having a whistleblowing policy and having whistleblowing arrangements that genuinely work are two different things. SYSC 18.3.1R requires appropriate and effective arrangements — with independently operating channels, enforced confidentiality protections, actively monitored non-retaliation commitments, and documented investigation processes. What the FCA finds when it looks is often a generic document, a single reporting channel routing straight to management, no anonymous option, and no SM&CR integration. For a regime designed to surface the problems that internal management won't surface itself, that architecture defeats the purpose entirely. Whistleblowing arrangements that only work when nothing serious happens aren't arrangements — they're decoration.

What's included:

Full regulatory mapping: SYSC 18.3.1R/18.3.3R/18.4.1R, PIDA 1998, ERA 1996 ss47B/103A, SM&CR Conduct Rules 1–4, FSMA 2000, POCA 2002, UK GDPR/DPA 2018, and Consumer Duty PS22/9

Seven-category reportable concern framework: Regulatory Breaches, Financial Crime and Market Abuse, Consumer Harm, SM&CR and Conduct Rules Breaches, Operational Failures, Health and Safety, and a zero-tolerance Financial Crime statement

Five internal reporting channels: Designated Whistleblowing Officer, Anonymous Hotline, Secure Encrypted Email Portal, Written Communications, and Third-Party Reporting Service with guaranteed anonymity

Identity protection framework: access restrictions, encrypted storage, anonymisation procedures, code names and reference numbers, and consent protocols before any identity disclosure

Non-retaliation monitoring matrix: 30/60/180-day follow-up contact, ongoing HR data analysis of employment actions affecting disclosers, and quarterly Board reporting

Financial crime escalation matrix: money laundering (immediate MLRO/SAR), fraud (law enforcement liaison), market abuse (immediate FCA notification), and sanctions (OFSI and FCA immediate)

SM&CR integration: Conduct Rules breach identification, Senior Manager accountability assessment against Statement of Responsibilities, and regulatory reporting obligations matrix

+ much more

Who is this for?

Compliance Officers, SMF16 holders, Audit Committee Chairs, HR Directors, and governance teams at FCA-regulated firms who need a complete, board-approved Whistleblowing Policy with genuinely independent reporting channels, enforceable confidentiality protections, and investigation procedures that withstand both regulatory scrutiny and Employment Tribunal challenge.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Having a whistleblowing policy and having whistleblowing arrangements that genuinely work are two different things. SYSC 18.3.1R requires appropriate and effective arrangements — with independently operating channels, enforced confidentiality protections, actively monitored non-retaliation commitments, and documented investigation processes. What the FCA finds when it looks is often a generic document, a single reporting channel routing straight to management, no anonymous option, and no SM&CR integration. For a regime designed to surface the problems that internal management won't surface itself, that architecture defeats the purpose entirely. Whistleblowing arrangements that only work when nothing serious happens aren't arrangements — they're decoration.

What's included:

Full regulatory mapping: SYSC 18.3.1R/18.3.3R/18.4.1R, PIDA 1998, ERA 1996 ss47B/103A, SM&CR Conduct Rules 1–4, FSMA 2000, POCA 2002, UK GDPR/DPA 2018, and Consumer Duty PS22/9

Seven-category reportable concern framework: Regulatory Breaches, Financial Crime and Market Abuse, Consumer Harm, SM&CR and Conduct Rules Breaches, Operational Failures, Health and Safety, and a zero-tolerance Financial Crime statement

Five internal reporting channels: Designated Whistleblowing Officer, Anonymous Hotline, Secure Encrypted Email Portal, Written Communications, and Third-Party Reporting Service with guaranteed anonymity

Identity protection framework: access restrictions, encrypted storage, anonymisation procedures, code names and reference numbers, and consent protocols before any identity disclosure

Non-retaliation monitoring matrix: 30/60/180-day follow-up contact, ongoing HR data analysis of employment actions affecting disclosers, and quarterly Board reporting

Financial crime escalation matrix: money laundering (immediate MLRO/SAR), fraud (law enforcement liaison), market abuse (immediate FCA notification), and sanctions (OFSI and FCA immediate)

SM&CR integration: Conduct Rules breach identification, Senior Manager accountability assessment against Statement of Responsibilities, and regulatory reporting obligations matrix

+ much more

Who is this for?

Compliance Officers, SMF16 holders, Audit Committee Chairs, HR Directors, and governance teams at FCA-regulated firms who need a complete, board-approved Whistleblowing Policy with genuinely independent reporting channels, enforceable confidentiality protections, and investigation procedures that withstand both regulatory scrutiny and Employment Tribunal challenge.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7