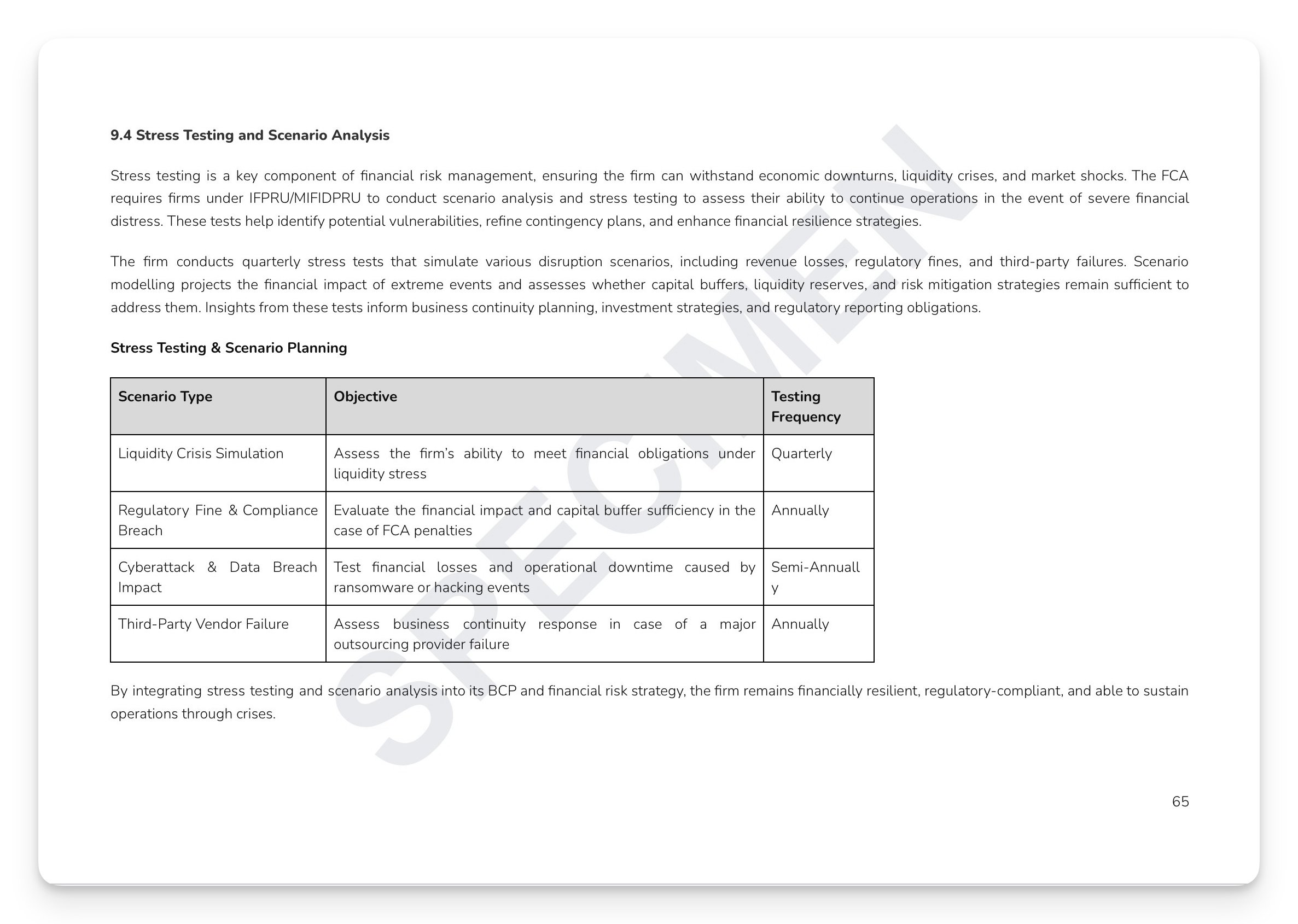

Having trained people and being able to demonstrate to the FCA that your people are competent are two entirely different things. The TC Sourcebook requires systematic competence assessment before unsupervised regulated activity, structured supervision calibrated to individual competence levels, mandatory qualifications aligned to TC Appendix 1, sector-specific CPD hours, and comprehensive records retained for six years. A training completion spreadsheet isn't a T&C framework. When the FCA comes in, it looks for documented evidence that individuals were assessed as competent before performing regulated functions independently. Gaps in any of those areas generate findings. Under SM&CR, incompetence isn't just a training failure — it's an accountability failure.

What's included:

Full regulatory mapping: TC Sourcebook, TC 2.1.17R, TC Appendix 1, SYSC, COBS, ICOBS, MCOB, CONC, and SM&CR SYSC 24–27

Multi-sector qualification framework: investment advisers, insurance intermediaries, consumer credit, payment services, debt management, and funeral plans — all TC Appendix 1 compliant with 70%+ pass standard

Three-tier supervision intensity model: Close Supervision (daily), Regular Supervision (structured weekly/periodic file reviews), and General Supervision (monthly/quarterly) — calibrated to individual competence stage

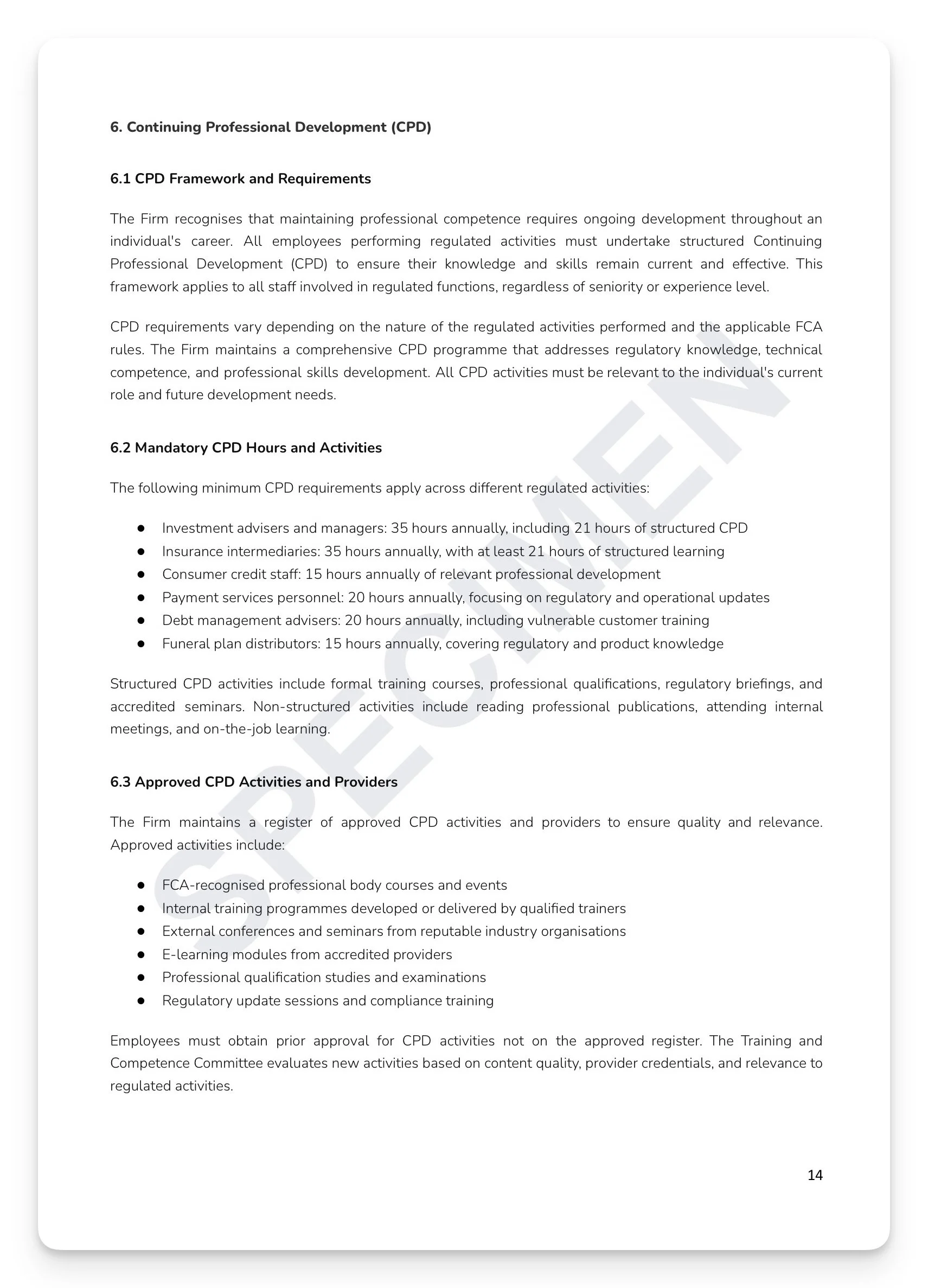

Sector-specific CPD mandatory hours: investment advisers (35hrs/21 structured), insurance intermediaries (35hrs/21 structured), consumer credit (15hrs), and payment services (20hrs)

Competence Improvement Plan: 5-day assessment, 10-day CIP development, monthly progress reviews — with immediate risk mitigation including enhanced supervision and restricted activities

Contractor and AR equivalence: same competence standards, initial assessment, CPD requirements, and supervision as permanent employees

KPI framework: 100% training completion, 85% first-attempt pass rate, 100% CPD compliance, and time-to-competence within 12 months

+ much more

Who is this for?

Compliance Officers, SMF16 holders, T&C managers, HR Directors, and line managers at FCA-regulated firms across all sectors who need a complete, board-approved Training and Competence Policy that produces the documented evidence the FCA expects during supervisory review.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Having trained people and being able to demonstrate to the FCA that your people are competent are two entirely different things. The TC Sourcebook requires systematic competence assessment before unsupervised regulated activity, structured supervision calibrated to individual competence levels, mandatory qualifications aligned to TC Appendix 1, sector-specific CPD hours, and comprehensive records retained for six years. A training completion spreadsheet isn't a T&C framework. When the FCA comes in, it looks for documented evidence that individuals were assessed as competent before performing regulated functions independently. Gaps in any of those areas generate findings. Under SM&CR, incompetence isn't just a training failure — it's an accountability failure.

What's included:

Full regulatory mapping: TC Sourcebook, TC 2.1.17R, TC Appendix 1, SYSC, COBS, ICOBS, MCOB, CONC, and SM&CR SYSC 24–27

Multi-sector qualification framework: investment advisers, insurance intermediaries, consumer credit, payment services, debt management, and funeral plans — all TC Appendix 1 compliant with 70%+ pass standard

Three-tier supervision intensity model: Close Supervision (daily), Regular Supervision (structured weekly/periodic file reviews), and General Supervision (monthly/quarterly) — calibrated to individual competence stage

Sector-specific CPD mandatory hours: investment advisers (35hrs/21 structured), insurance intermediaries (35hrs/21 structured), consumer credit (15hrs), and payment services (20hrs)

Competence Improvement Plan: 5-day assessment, 10-day CIP development, monthly progress reviews — with immediate risk mitigation including enhanced supervision and restricted activities

Contractor and AR equivalence: same competence standards, initial assessment, CPD requirements, and supervision as permanent employees

KPI framework: 100% training completion, 85% first-attempt pass rate, 100% CPD compliance, and time-to-competence within 12 months

+ much more

Who is this for?

Compliance Officers, SMF16 holders, T&C managers, HR Directors, and line managers at FCA-regulated firms across all sectors who need a complete, board-approved Training and Competence Policy that produces the documented evidence the FCA expects during supervisory review.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7