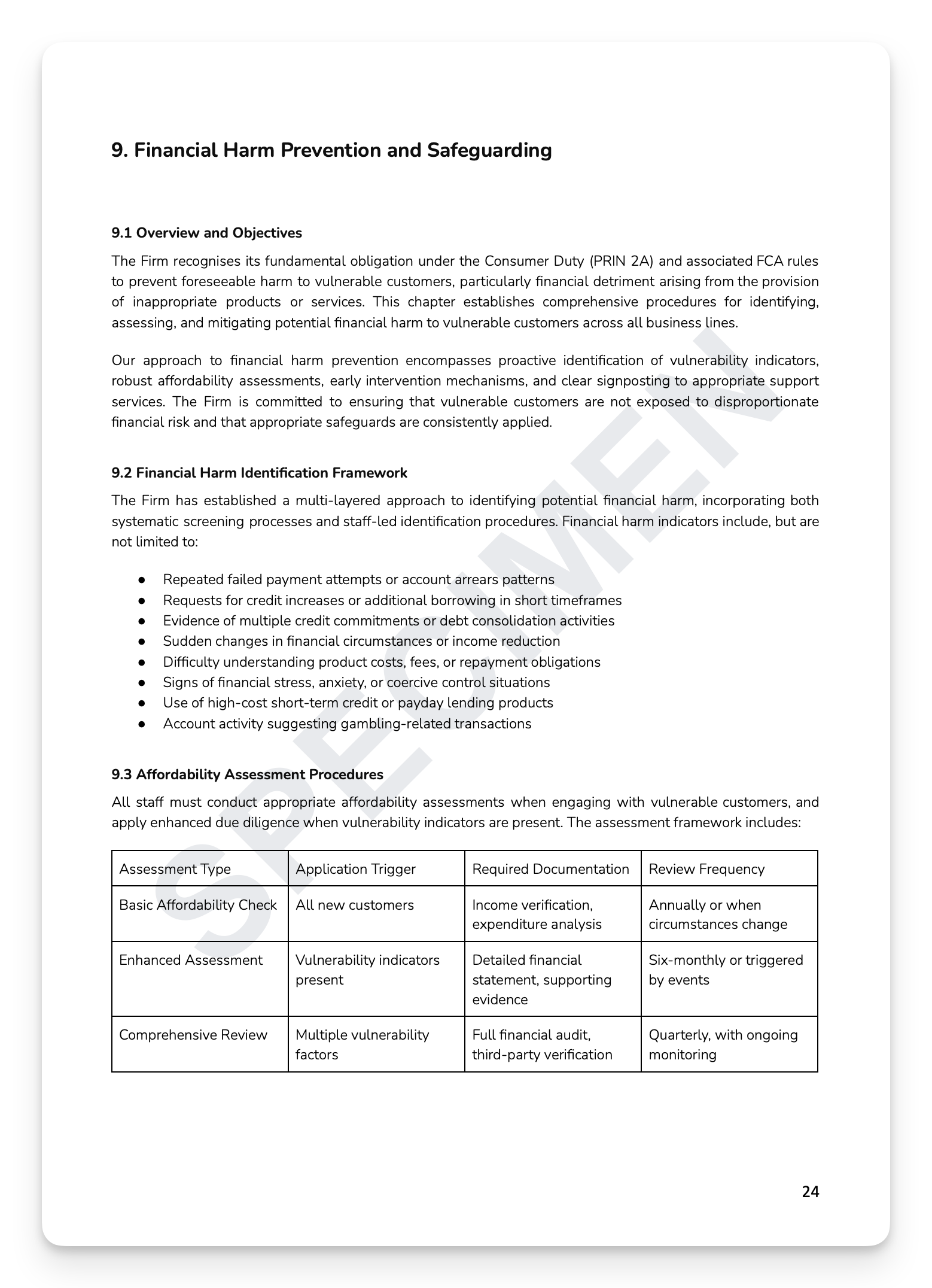

Consumer Duty's Customer Support outcome isn't satisfied by having a helpline and a complaints process. Under PRIN 2A.6, firms must monitor whether their support is actually working, segment vulnerable customers, evidence service quality, and report to the Board with data that demonstrates genuine outcome delivery. The FCA expects MI that goes beyond call volumes and response times. The FCA doesn't wait.

What's included:

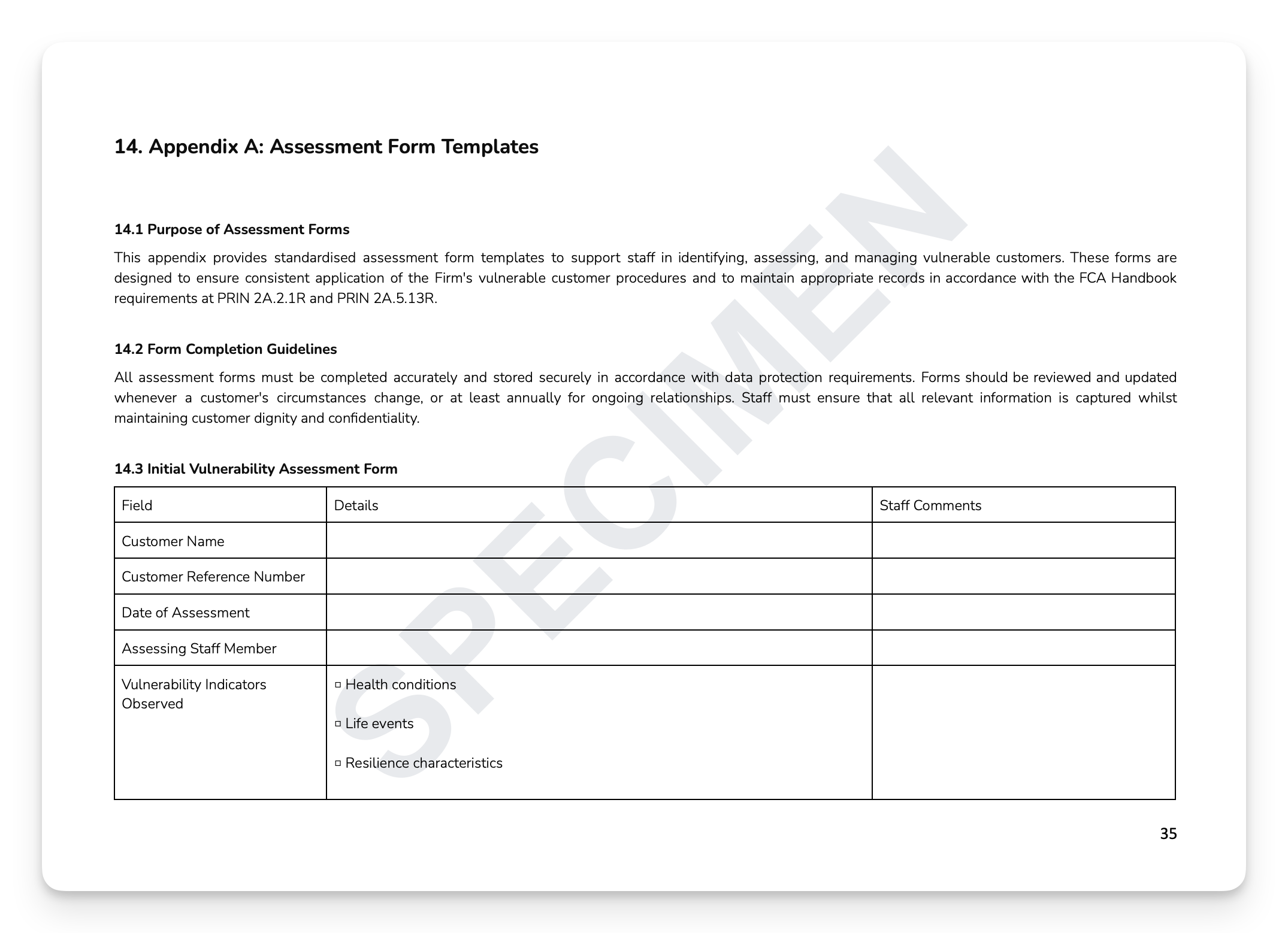

Customer segmentation and vulnerability assessment: identification framework, segmentation methodology, data sources, and dynamic review processes

Channel accessibility: telephone support standards, digital channel vulnerability assessment, and multi-channel consistency

Service quality metrics: response time standards, resolution effectiveness, and quality assessment framework

Vulnerable customer monitoring: specialised support metrics, data-led validation, and inclusive practice implementation

Complaint and feedback analysis: classification framework, root cause analysis, systemic issue identification, and remediation

Board reporting and accountability: documentation requirements, MI standards, and Board reporting framework

Ready-to-use appendices: Vulnerability Assessment Template, Channel Accessibility Audit, Service Quality Scorecard, and MI Data Validation Framework

+ much more

Who is this for?

Compliance Officers, Consumer Duty leads, Customer Operations Directors, SMF holders, and Boards at FCA-regulated firms.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Consumer Duty's Customer Support outcome isn't satisfied by having a helpline and a complaints process. Under PRIN 2A.6, firms must monitor whether their support is actually working, segment vulnerable customers, evidence service quality, and report to the Board with data that demonstrates genuine outcome delivery. The FCA expects MI that goes beyond call volumes and response times. The FCA doesn't wait.

What's included:

Customer segmentation and vulnerability assessment: identification framework, segmentation methodology, data sources, and dynamic review processes

Channel accessibility: telephone support standards, digital channel vulnerability assessment, and multi-channel consistency

Service quality metrics: response time standards, resolution effectiveness, and quality assessment framework

Vulnerable customer monitoring: specialised support metrics, data-led validation, and inclusive practice implementation

Complaint and feedback analysis: classification framework, root cause analysis, systemic issue identification, and remediation

Board reporting and accountability: documentation requirements, MI standards, and Board reporting framework

Ready-to-use appendices: Vulnerability Assessment Template, Channel Accessibility Audit, Service Quality Scorecard, and MI Data Validation Framework

+ much more

Who is this for?

Compliance Officers, Consumer Duty leads, Customer Operations Directors, SMF holders, and Boards at FCA-regulated firms.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7