Fair value isn't a tick-box exercise — it's one of the FCA's highest supervisory priorities under Consumer Duty. Under PRIN 2A.4, firms must demonstrate that the price customers pay bears a reasonable relationship to the overall benefits they receive. Firms that cannot produce this evidence face intervention, remediation requirements, and enforcement action. The FCA doesn't wait.

What's included:

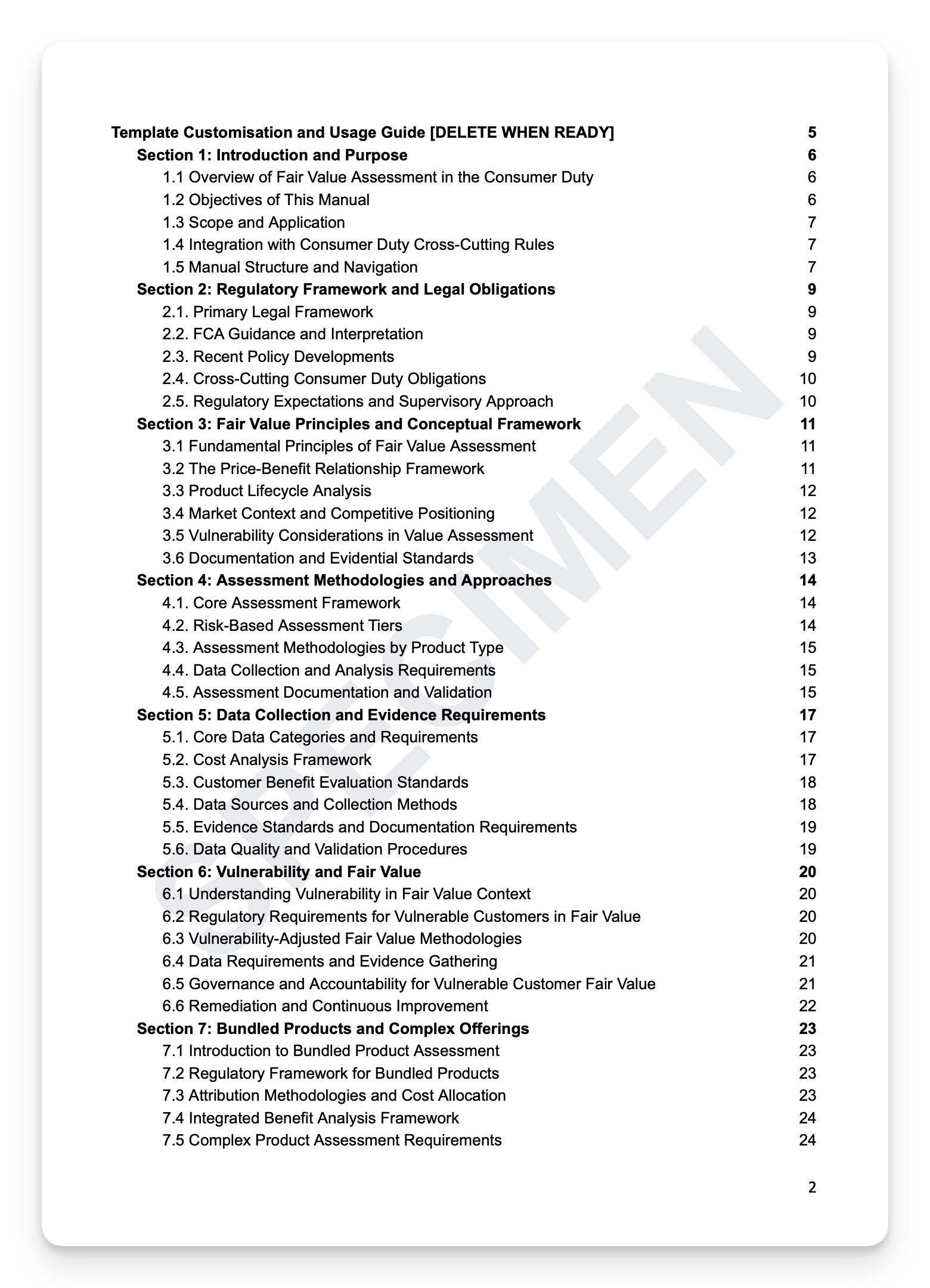

Assessment methodologies: core framework, risk-based assessment tiers, methodologies by product type, and data collection requirements

Vulnerability-adjusted fair value: regulatory requirements, vulnerability-specific methodologies, data requirements, and governance

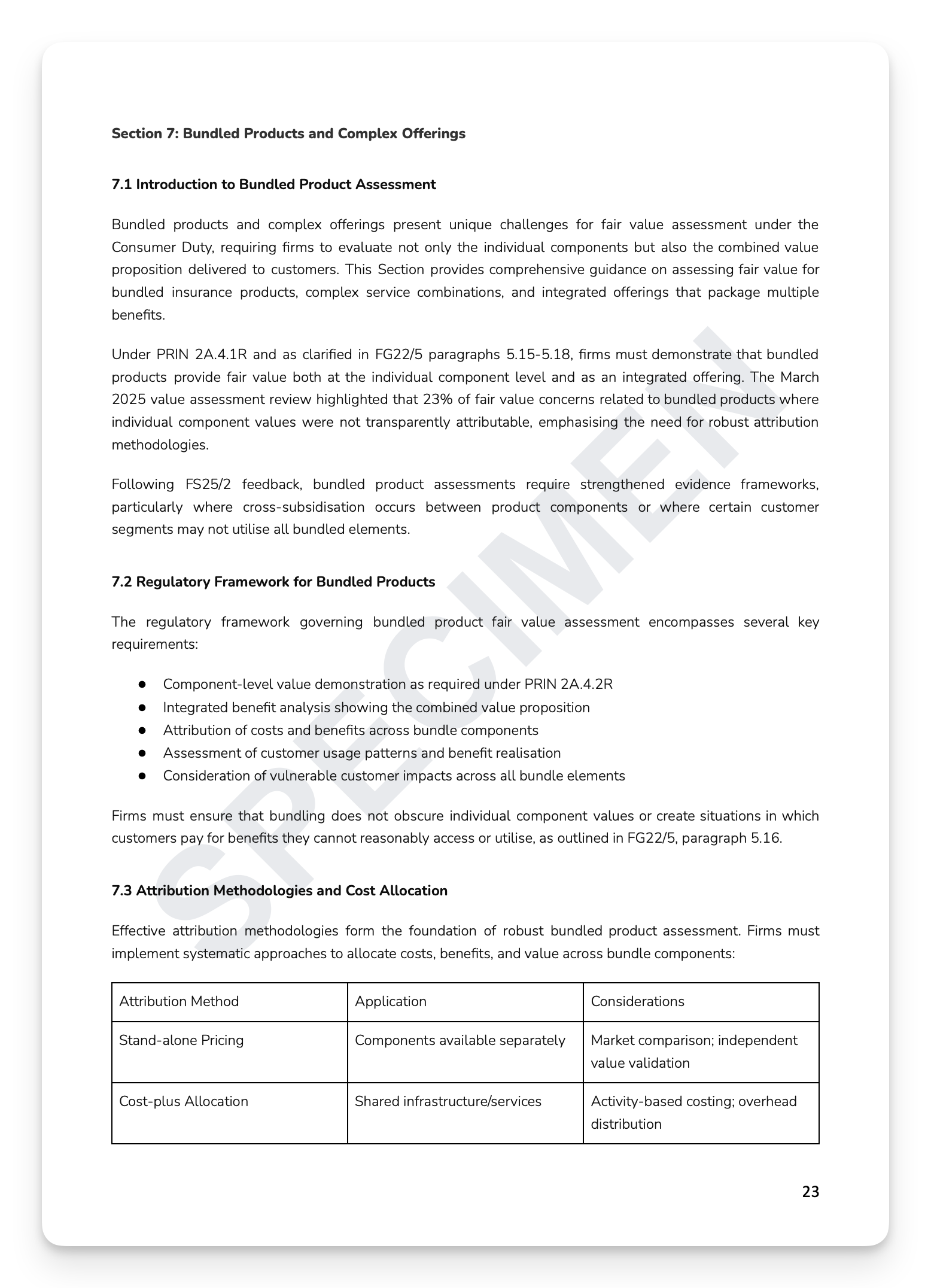

Bundled products and complex offerings: attribution methodologies, cost allocation, integrated benefit analysis, and customer segmentation

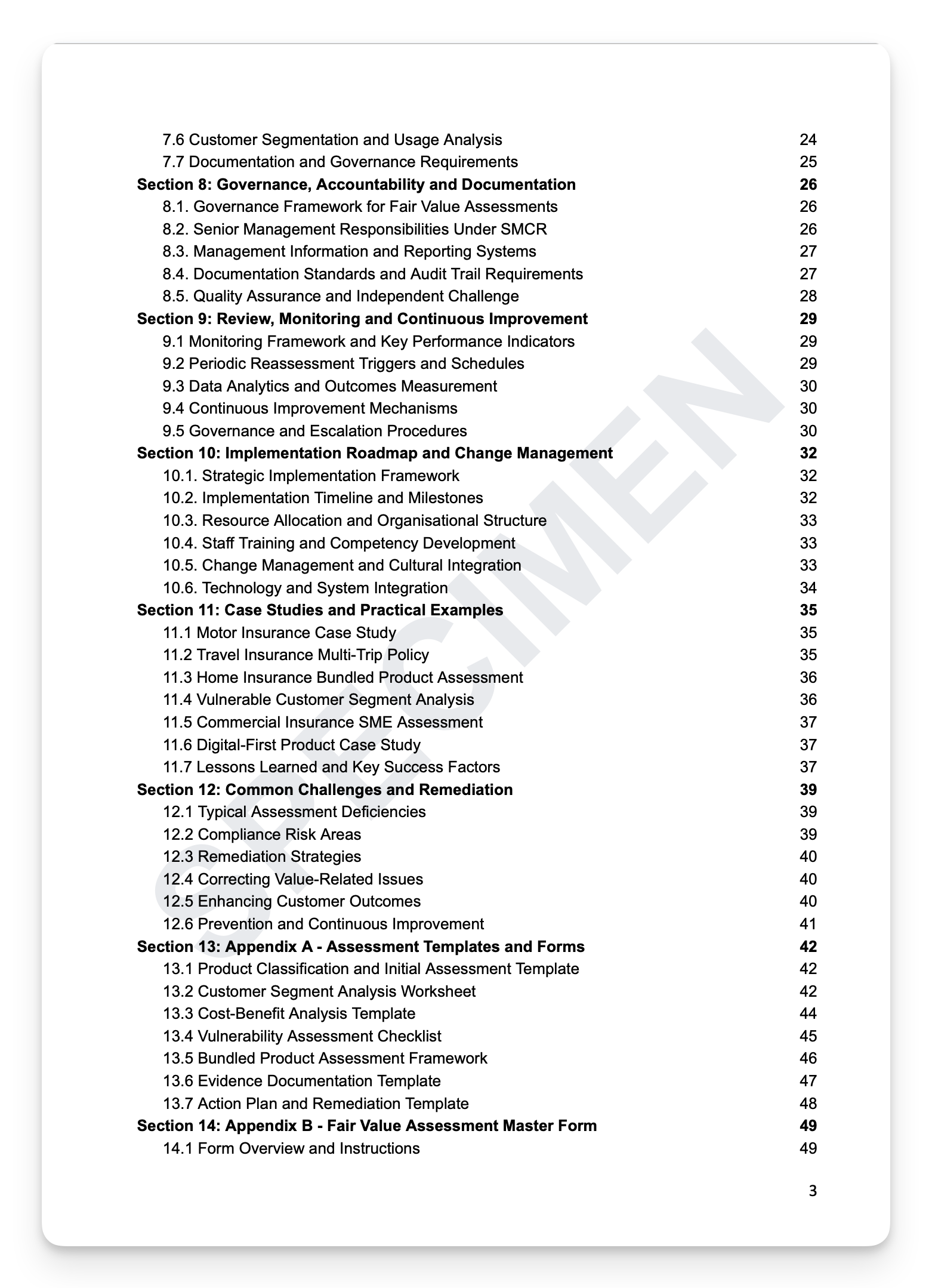

Governance and documentation: SM&CR responsibilities, MI and reporting systems, documentation standards, and quality assurance

Continuous monitoring: KPIs, periodic reassessment triggers, data analytics, and escalation procedures

Case studies: motor insurance, travel insurance, home insurance, vulnerable customer analysis, SME assessment, and digital-first products

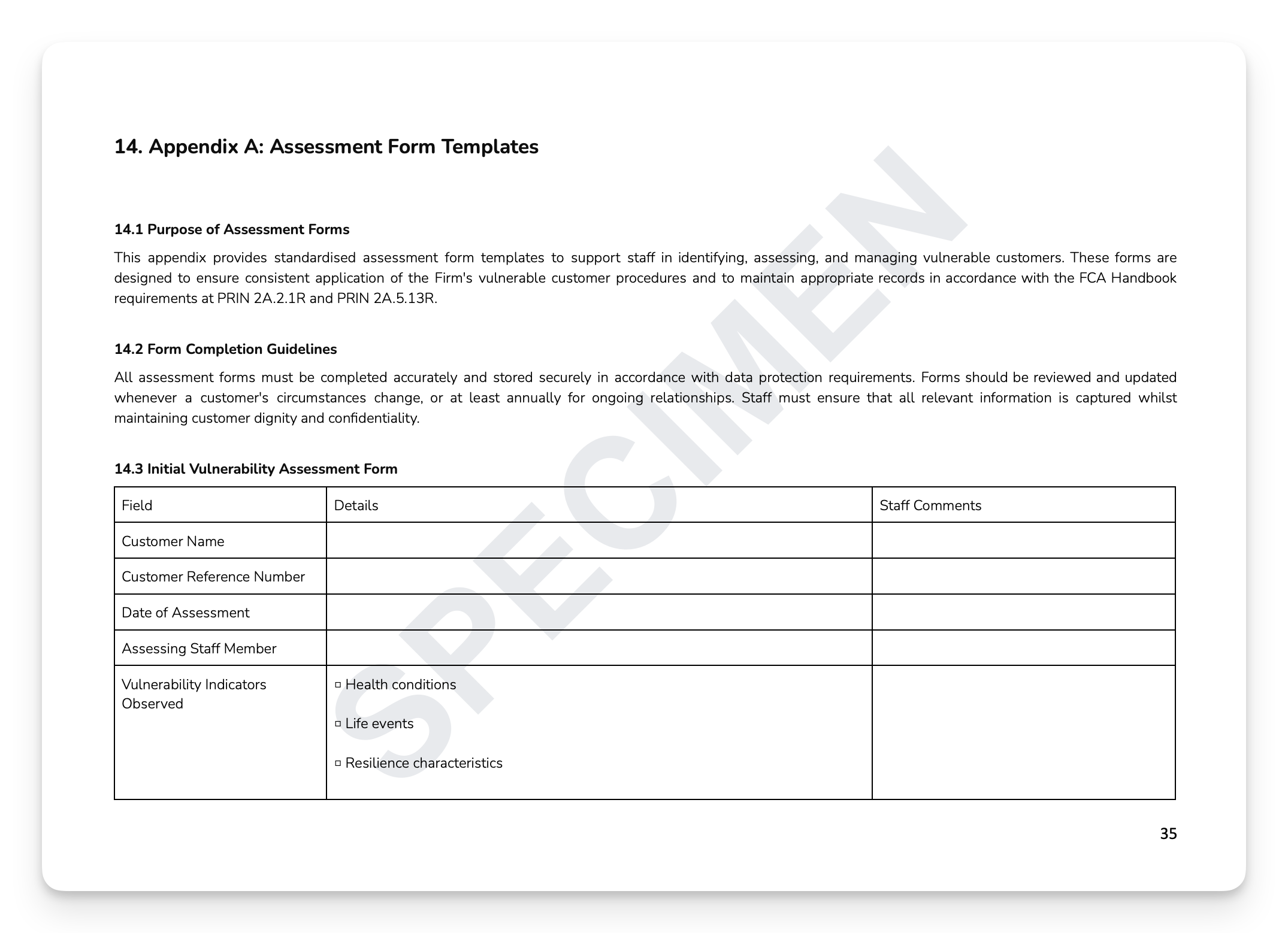

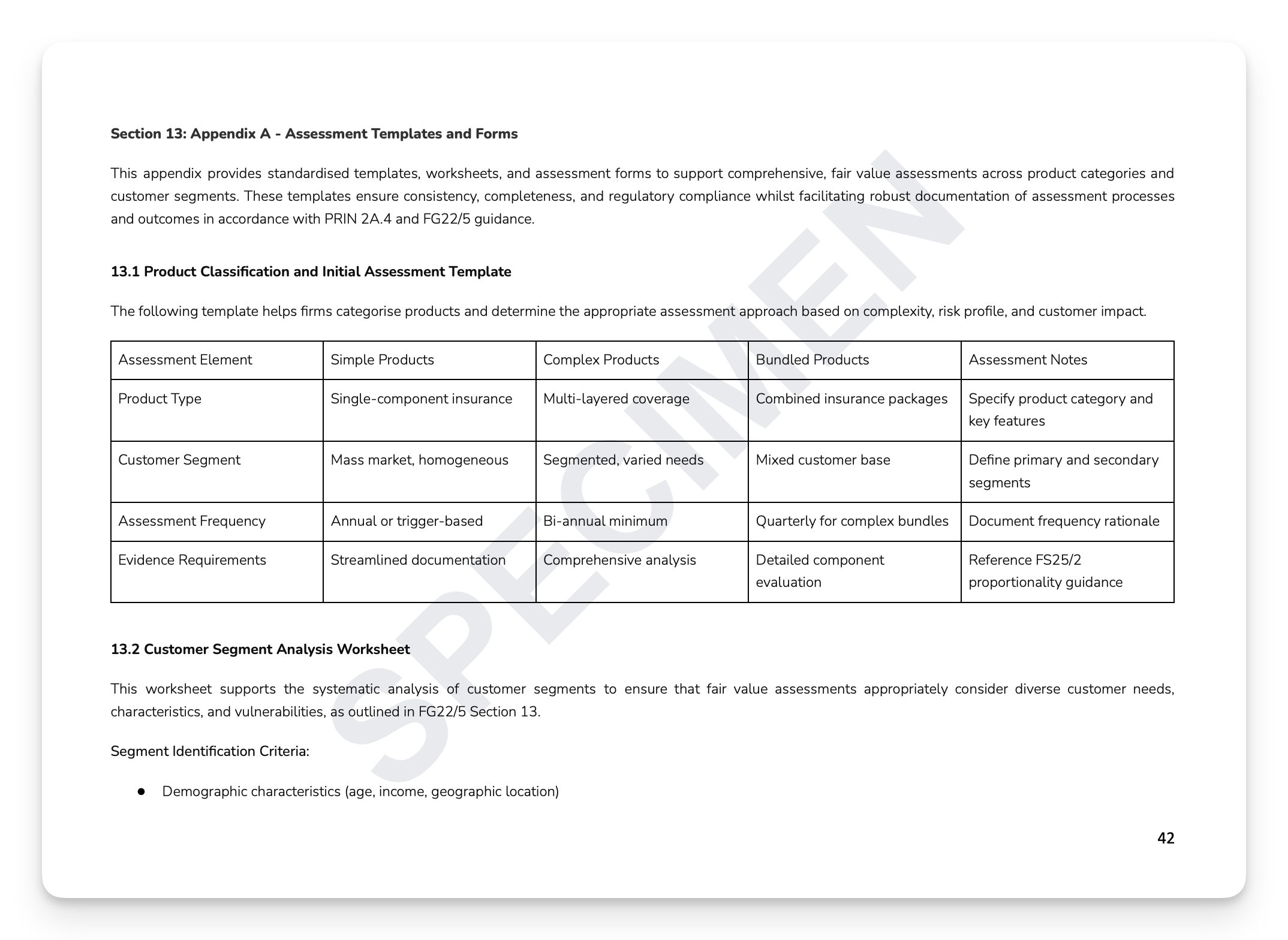

Ready-to-use appendices: Cost-Benefit Analysis Template, Vulnerability Assessment Checklist, Bundled Product Assessment Framework, and Fair Value Assessment Master Form

+ much more

Who is this for?

Compliance Officers, Consumer Duty leads, Actuaries, Product Managers, SMF holders, and Boards at FCA-regulated insurance, investment, and retail financial services firms.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Fair value isn't a tick-box exercise — it's one of the FCA's highest supervisory priorities under Consumer Duty. Under PRIN 2A.4, firms must demonstrate that the price customers pay bears a reasonable relationship to the overall benefits they receive. Firms that cannot produce this evidence face intervention, remediation requirements, and enforcement action. The FCA doesn't wait.

What's included:

Assessment methodologies: core framework, risk-based assessment tiers, methodologies by product type, and data collection requirements

Vulnerability-adjusted fair value: regulatory requirements, vulnerability-specific methodologies, data requirements, and governance

Bundled products and complex offerings: attribution methodologies, cost allocation, integrated benefit analysis, and customer segmentation

Governance and documentation: SM&CR responsibilities, MI and reporting systems, documentation standards, and quality assurance

Continuous monitoring: KPIs, periodic reassessment triggers, data analytics, and escalation procedures

Case studies: motor insurance, travel insurance, home insurance, vulnerable customer analysis, SME assessment, and digital-first products

Ready-to-use appendices: Cost-Benefit Analysis Template, Vulnerability Assessment Checklist, Bundled Product Assessment Framework, and Fair Value Assessment Master Form

+ much more

Who is this for?

Compliance Officers, Consumer Duty leads, Actuaries, Product Managers, SMF holders, and Boards at FCA-regulated insurance, investment, and retail financial services firms.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 8

Image 1 of 8

Image 2 of 8

Image 2 of 8

Image 3 of 8

Image 3 of 8

Image 4 of 8

Image 4 of 8

Image 5 of 8

Image 5 of 8

Image 6 of 8

Image 6 of 8

Image 7 of 8

Image 7 of 8

Image 8 of 8

Image 8 of 8