Every FCA-regulated firm knows financial promotions must be "clear, fair and not misleading." What few firms have is a complete, documented framework that operationalises that standard across every sector they operate in, every channel they use, every product they promote, and every customer segment they serve. FSMA Section 21 sets the floor. PRIN 7 raises it. Consumer Duty changes the entire assessment framework from "did we technically comply?" to "did we genuinely support customer understanding and avoid foreseeable harm?" Financial promotions aren't a marketing function — they're a compliance obligation with a three-tier approval structure, a six-year record retention requirement, and a 4-hour internal breach notification standard. Most firms have a checklist. This is the framework behind the checklist.

What's included:

Full regulatory mapping: FSMA s.21, FPO 2005, PRIN 1/2A/3/6/7/8/9/11, Consumer Duty PS22/9, COBS 4, ICOBS 2.2/2.5, CONC 3, MCOB 3/3A, BCOBS 2, SYSC 3/4/6/9, and CCA 1974

Seven-sector promotion rules matrix: Investment, Insurance, Consumer Credit, Mortgages, Payment Services, Cryptoassets, and Funeral Plans — with sector-specific mandatory disclosures and risk warnings

Three-lines-of-defence approval governance: content creators, independent compliance review, and internal audit — with authority matrix covering standard, high-risk investment, consumer credit, and expedited approvals

Digital channel framework: website, email (PECR compliance), social media (FG15/4 compliance), chatbots (AI disclosure/boundary management), and paid digital (search/retargeting/Consumer Duty pressure assessment)

Vulnerable customer framework: four-driver model, WCAG 2.1 AA accessibility, reading age 11–13 standard, and monetary amounts over percentages

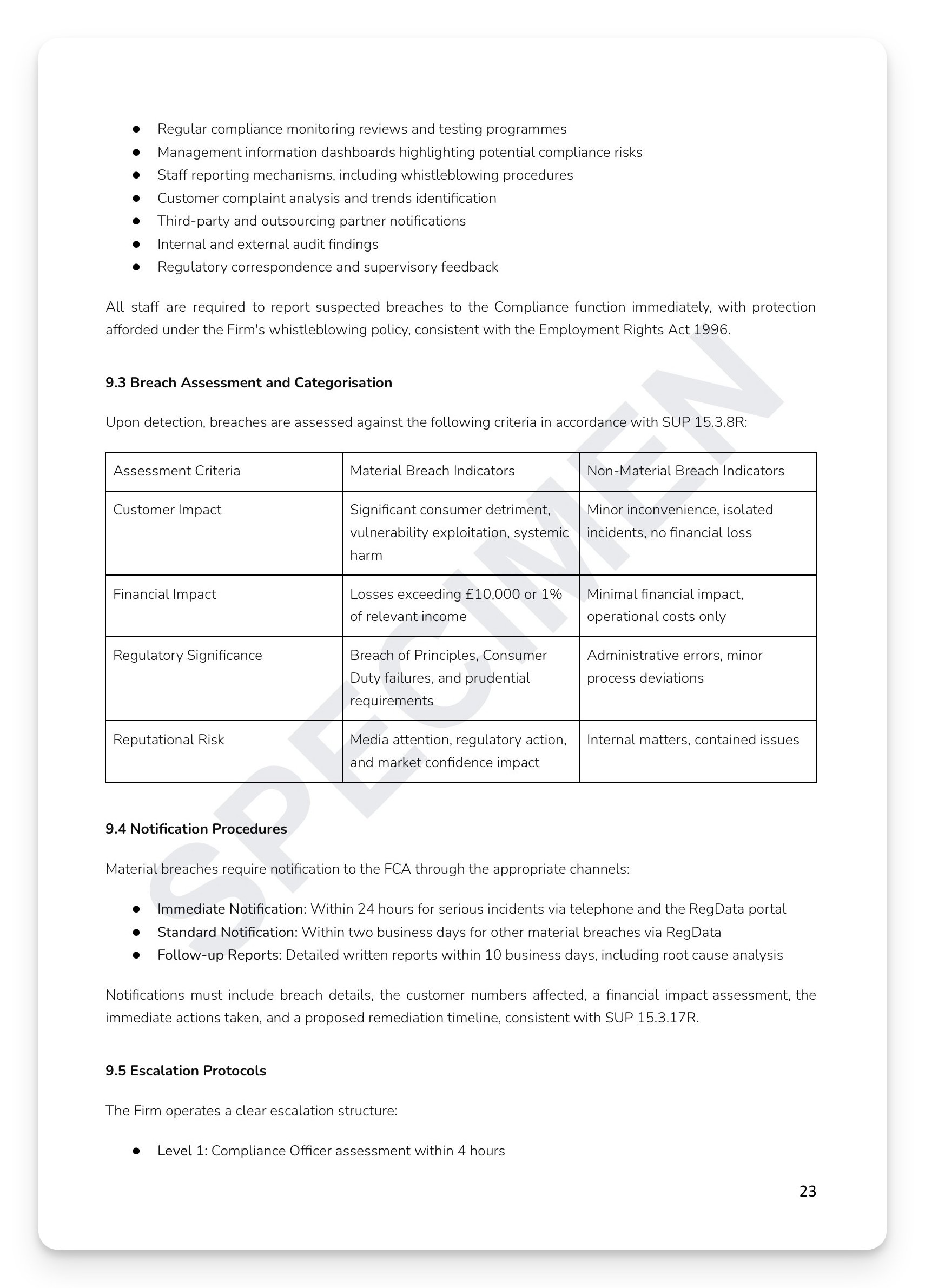

Breach classification: Category 1 (critical/4-hour notification/Board within 5 days), Category 2 (significant/48-hour senior management), and Category 3 (minor) — with SUP 15.3.17R FCA reporting triggers

Ready-to-use Promotion Assessment Form: 25 compliance criteria across core requirements, Consumer Duty, sector-specific rules, vulnerable customers, and digital channels — with sign-off matrix

+ much more

Who is this for?

Compliance Officers, Approved Persons, Marketing Directors, SMF holders, and Compliance Monitoring teams at FCA-regulated firms across any regulated sector who need a complete, board-approved Financial Promotions Manual governing every promotional touchpoint from approval through to breach remediation.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Every FCA-regulated firm knows financial promotions must be "clear, fair and not misleading." What few firms have is a complete, documented framework that operationalises that standard across every sector they operate in, every channel they use, every product they promote, and every customer segment they serve. FSMA Section 21 sets the floor. PRIN 7 raises it. Consumer Duty changes the entire assessment framework from "did we technically comply?" to "did we genuinely support customer understanding and avoid foreseeable harm?" Financial promotions aren't a marketing function — they're a compliance obligation with a three-tier approval structure, a six-year record retention requirement, and a 4-hour internal breach notification standard. Most firms have a checklist. This is the framework behind the checklist.

What's included:

Full regulatory mapping: FSMA s.21, FPO 2005, PRIN 1/2A/3/6/7/8/9/11, Consumer Duty PS22/9, COBS 4, ICOBS 2.2/2.5, CONC 3, MCOB 3/3A, BCOBS 2, SYSC 3/4/6/9, and CCA 1974

Seven-sector promotion rules matrix: Investment, Insurance, Consumer Credit, Mortgages, Payment Services, Cryptoassets, and Funeral Plans — with sector-specific mandatory disclosures and risk warnings

Three-lines-of-defence approval governance: content creators, independent compliance review, and internal audit — with authority matrix covering standard, high-risk investment, consumer credit, and expedited approvals

Digital channel framework: website, email (PECR compliance), social media (FG15/4 compliance), chatbots (AI disclosure/boundary management), and paid digital (search/retargeting/Consumer Duty pressure assessment)

Vulnerable customer framework: four-driver model, WCAG 2.1 AA accessibility, reading age 11–13 standard, and monetary amounts over percentages

Breach classification: Category 1 (critical/4-hour notification/Board within 5 days), Category 2 (significant/48-hour senior management), and Category 3 (minor) — with SUP 15.3.17R FCA reporting triggers

Ready-to-use Promotion Assessment Form: 25 compliance criteria across core requirements, Consumer Duty, sector-specific rules, vulnerable customers, and digital channels — with sign-off matrix

+ much more

Who is this for?

Compliance Officers, Approved Persons, Marketing Directors, SMF holders, and Compliance Monitoring teams at FCA-regulated firms across any regulated sector who need a complete, board-approved Financial Promotions Manual governing every promotional touchpoint from approval through to breach remediation.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 11

Image 1 of 11

Image 2 of 11

Image 2 of 11

Image 3 of 11

Image 3 of 11

Image 4 of 11

Image 4 of 11

Image 5 of 11

Image 5 of 11

Image 6 of 11

Image 6 of 11

Image 7 of 11

Image 7 of 11

Image 8 of 11

Image 8 of 11

Image 9 of 11

Image 9 of 11

Image 10 of 11

Image 10 of 11

Image 11 of 11

Image 11 of 11