Vulnerability isn't an edge case — the FCA estimates half of UK adults display one or more characteristics of vulnerability at any given time. Under FG21/1 and Consumer Duty's cross-cutting rules, firms must have a structured, evidenced framework for identifying vulnerable customers, adapting their treatment, and monitoring outcomes. The FCA expects vulnerability embedded in product design, customer interactions, complaints handling, and Board-level reporting. The FCA doesn't wait.

What's included:

Four vulnerability drivers: health, life events, resilience, and capability — each with detailed characteristics and implementation requirements

Identification and assessment: customer journey touchpoints, primary assessment methods, capacity assessment procedures, and ongoing reassessment

Communication and interaction standards: language and tone, format adjustments, verification of understanding, and digital standards

Product suitability: enhanced suitability assessment, fair value and pricing transparency, and ongoing suitability monitoring

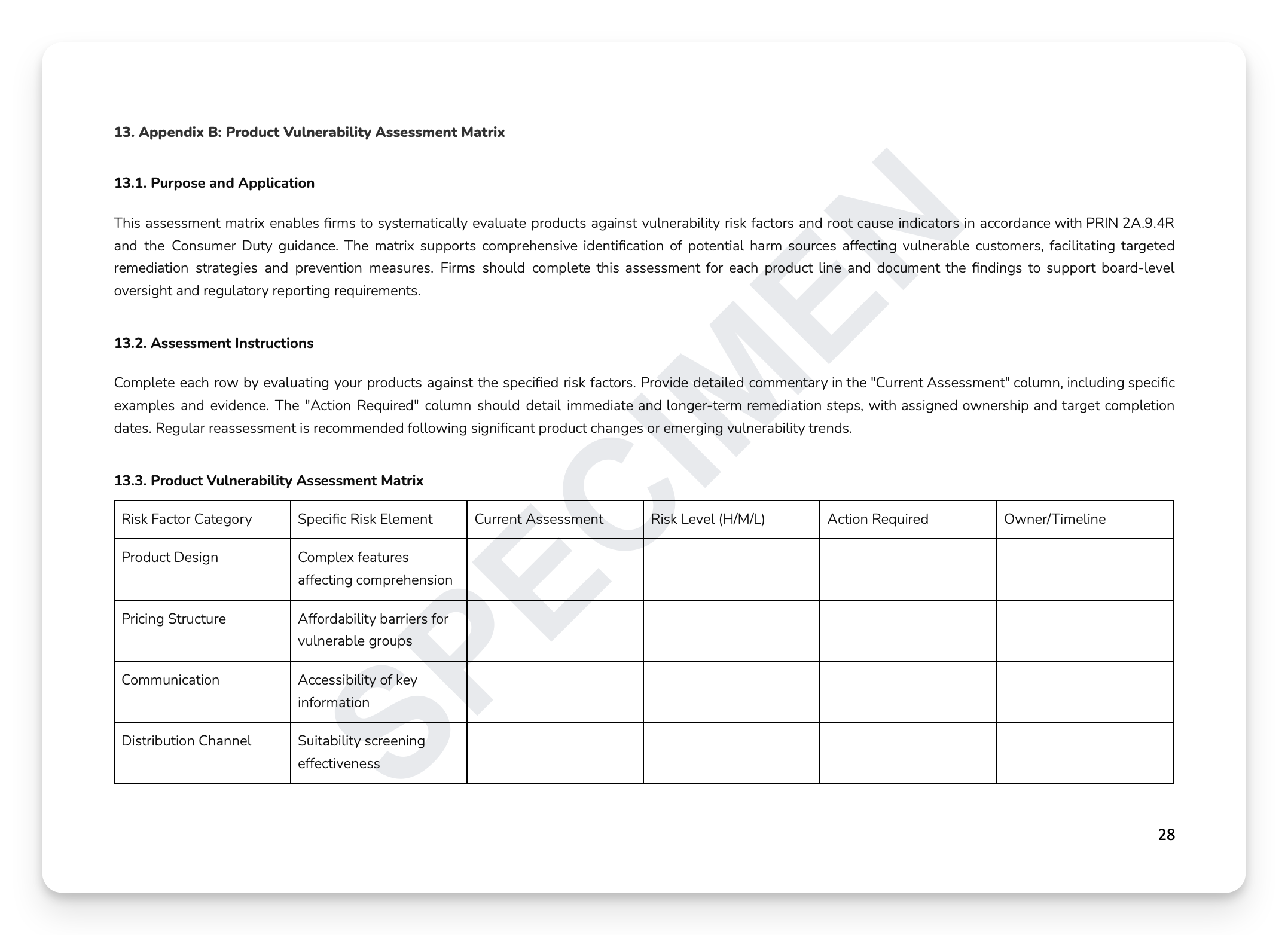

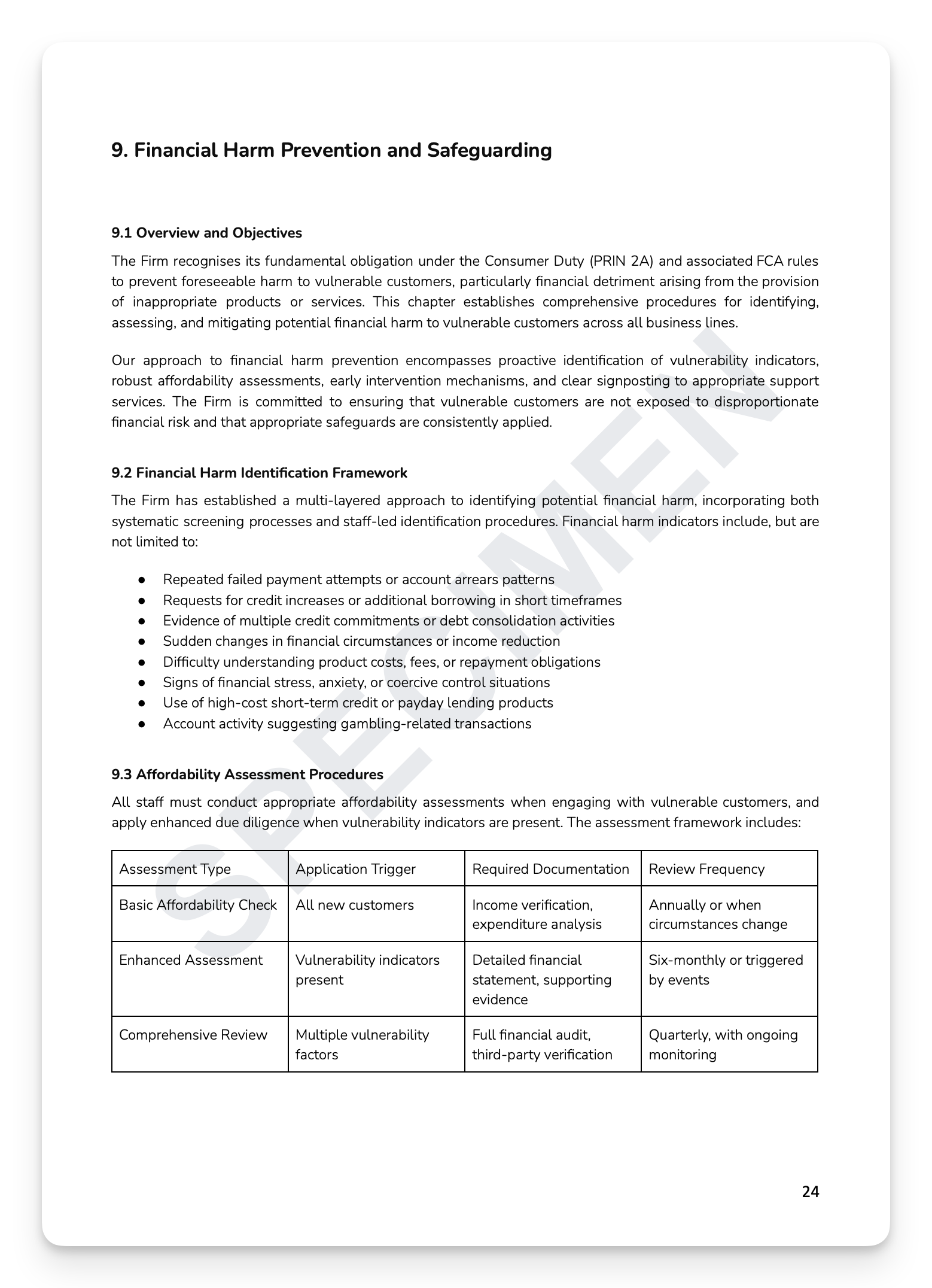

Financial harm prevention: harm identification, affordability assessment, safeguarding measures, and intervention protocols

Managing specific vulnerability types: mental capacity, language barriers, bereavement, elder abuse, and financial abuse

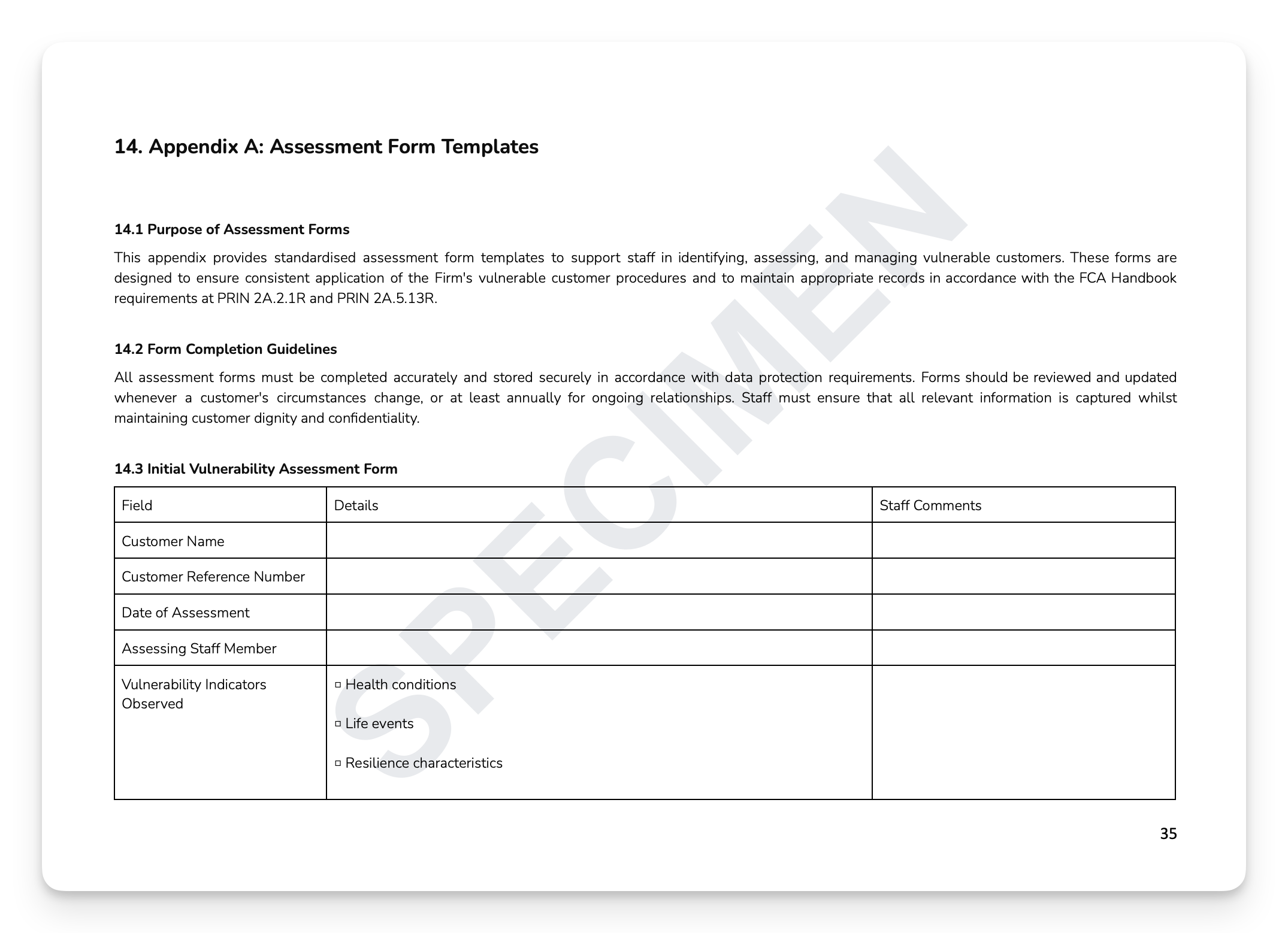

Ready-to-use appendices: Initial Vulnerability Assessment Form, Detailed Vulnerability Impact Assessment, and Ongoing Monitoring and Review Form

+ much more

Who is this for?

Compliance Officers, Consumer Duty leads, Customer Operations Directors, SMF holders, and Boards at FCA-regulated firms.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Vulnerability isn't an edge case — the FCA estimates half of UK adults display one or more characteristics of vulnerability at any given time. Under FG21/1 and Consumer Duty's cross-cutting rules, firms must have a structured, evidenced framework for identifying vulnerable customers, adapting their treatment, and monitoring outcomes. The FCA expects vulnerability embedded in product design, customer interactions, complaints handling, and Board-level reporting. The FCA doesn't wait.

What's included:

Four vulnerability drivers: health, life events, resilience, and capability — each with detailed characteristics and implementation requirements

Identification and assessment: customer journey touchpoints, primary assessment methods, capacity assessment procedures, and ongoing reassessment

Communication and interaction standards: language and tone, format adjustments, verification of understanding, and digital standards

Product suitability: enhanced suitability assessment, fair value and pricing transparency, and ongoing suitability monitoring

Financial harm prevention: harm identification, affordability assessment, safeguarding measures, and intervention protocols

Managing specific vulnerability types: mental capacity, language barriers, bereavement, elder abuse, and financial abuse

Ready-to-use appendices: Initial Vulnerability Assessment Form, Detailed Vulnerability Impact Assessment, and Ongoing Monitoring and Review Form

+ much more

Who is this for?

Compliance Officers, Consumer Duty leads, Customer Operations Directors, SMF holders, and Boards at FCA-regulated firms.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 9

Image 1 of 9

Image 2 of 9

Image 2 of 9

Image 3 of 9

Image 3 of 9

Image 4 of 9

Image 4 of 9

Image 5 of 9

Image 5 of 9

Image 6 of 9

Image 6 of 9

Image 7 of 9

Image 7 of 9

Image 8 of 9

Image 8 of 9

Image 9 of 9

Image 9 of 9