Consumer Duty isn't a compliance exercise — it's a cultural shift. Under PRIN 2A, every FCA-regulated firm must act to deliver good outcomes for retail customers across all four outcomes. The FCA has been explicit that it expects firms to go beyond rule compliance and demonstrate, through evidence, that they are genuinely acting in customers' best interests at every stage of the product and service lifecycle. The FCA doesn't wait.

What's included:

Full regulatory framework: PRIN 2A, Principle 12, three cross-cutting rules, and integration with COBS, ICOBS, and BCOBS

Product governance and design: target market assessment, product approval procedures, pricing and fair value, and lifecycle management

Consumer communications and marketing: financial promotions framework, plain language standards, digital communications, and monitoring

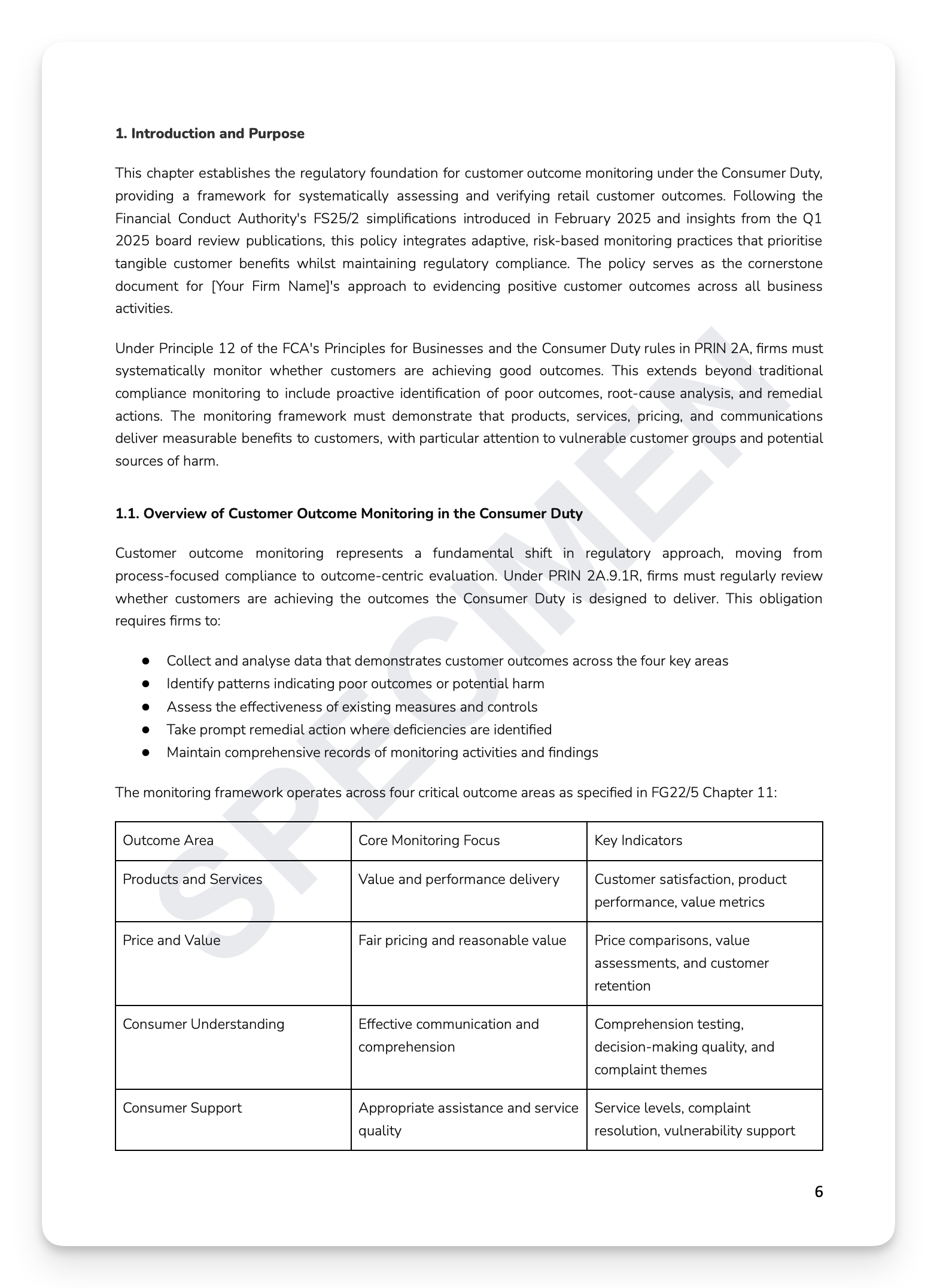

Four Consumer Duty outcomes: products and services, price and value, consumer understanding, and consumer support — each with KPIs and reporting

Governance and accountability: Board oversight, SMF accountability matrix, three-lines-of-defence, and Consumer Duty Champion Network

Training, culture, and awareness: role-specific training, cultural transformation framework, and effectiveness measurement

Remediation and complaints: detriment identification, remediation framework, and complaints handling under Consumer Duty

+ much more

Who is this for?

Compliance Officers, SMF holders, Consumer Duty leads, and Boards at FCA-regulated wealth management, investment, and retail financial services firms.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Consumer Duty isn't a compliance exercise — it's a cultural shift. Under PRIN 2A, every FCA-regulated firm must act to deliver good outcomes for retail customers across all four outcomes. The FCA has been explicit that it expects firms to go beyond rule compliance and demonstrate, through evidence, that they are genuinely acting in customers' best interests at every stage of the product and service lifecycle. The FCA doesn't wait.

What's included:

Full regulatory framework: PRIN 2A, Principle 12, three cross-cutting rules, and integration with COBS, ICOBS, and BCOBS

Product governance and design: target market assessment, product approval procedures, pricing and fair value, and lifecycle management

Consumer communications and marketing: financial promotions framework, plain language standards, digital communications, and monitoring

Four Consumer Duty outcomes: products and services, price and value, consumer understanding, and consumer support — each with KPIs and reporting

Governance and accountability: Board oversight, SMF accountability matrix, three-lines-of-defence, and Consumer Duty Champion Network

Training, culture, and awareness: role-specific training, cultural transformation framework, and effectiveness measurement

Remediation and complaints: detriment identification, remediation framework, and complaints handling under Consumer Duty

+ much more

Who is this for?

Compliance Officers, SMF holders, Consumer Duty leads, and Boards at FCA-regulated wealth management, investment, and retail financial services firms.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 8

Image 1 of 8

Image 2 of 8

Image 2 of 8

Image 3 of 8

Image 3 of 8

Image 4 of 8

Image 4 of 8

Image 5 of 8

Image 5 of 8

Image 6 of 8

Image 6 of 8

Image 7 of 8

Image 7 of 8

Image 8 of 8

Image 8 of 8