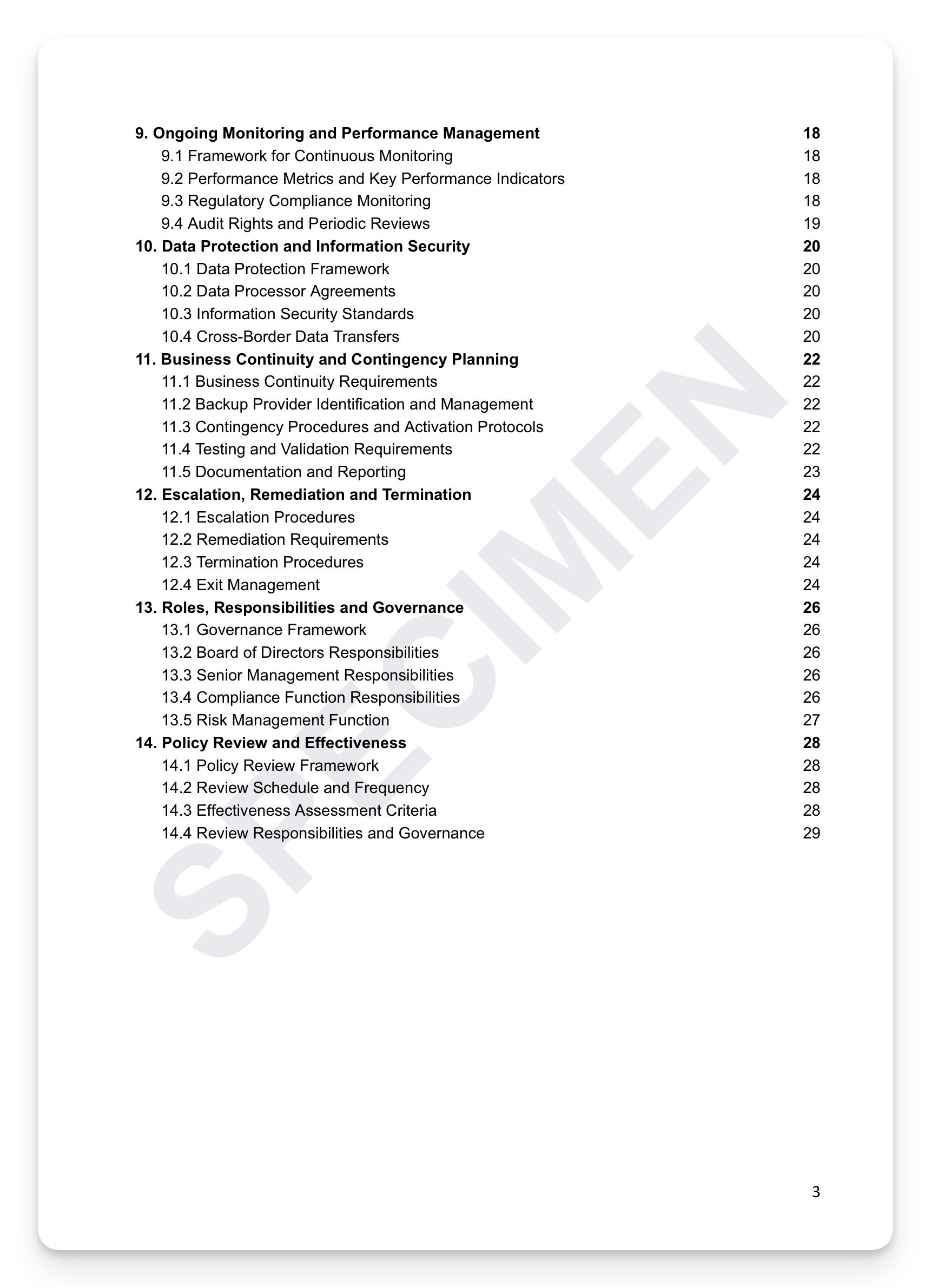

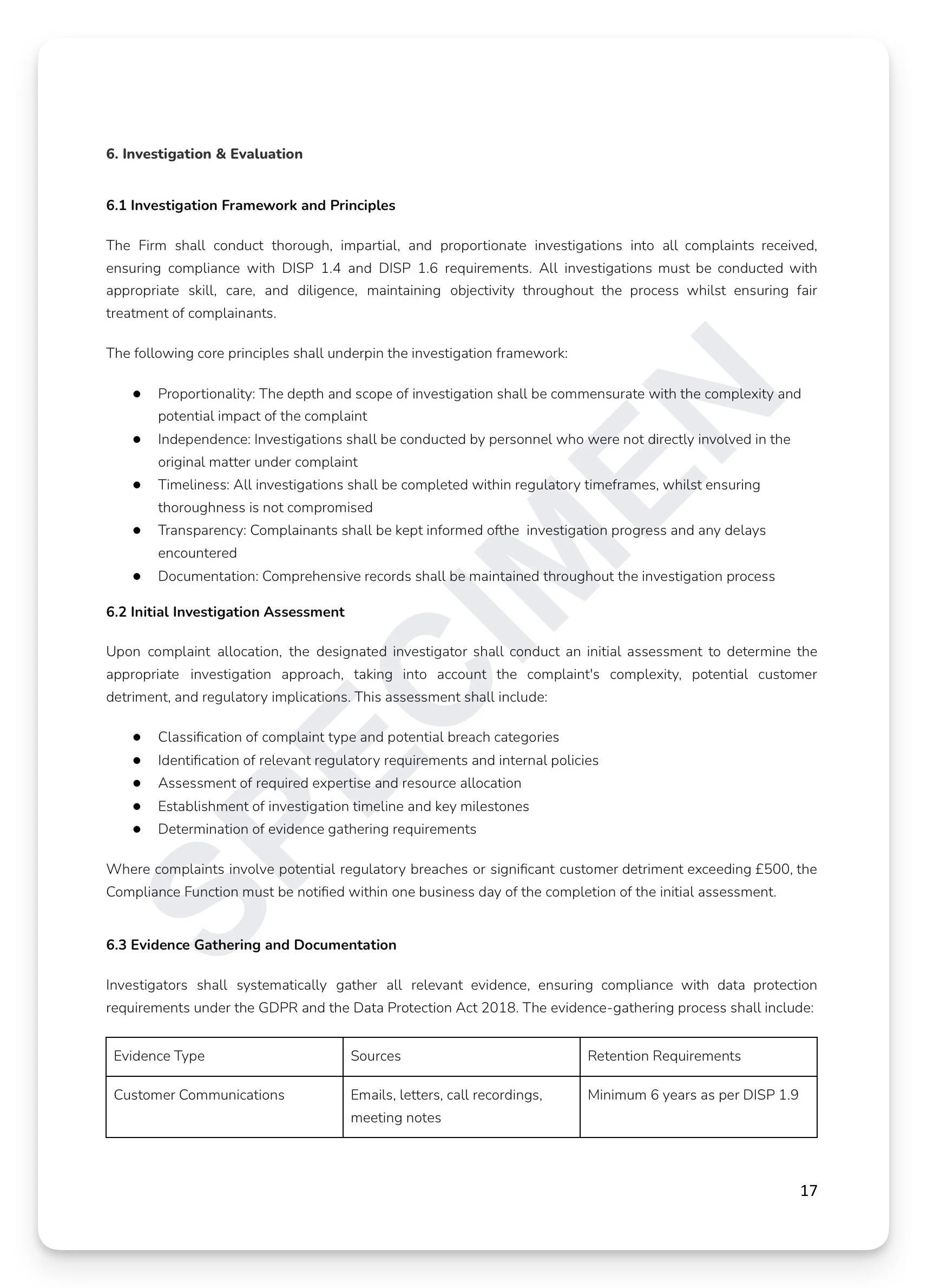

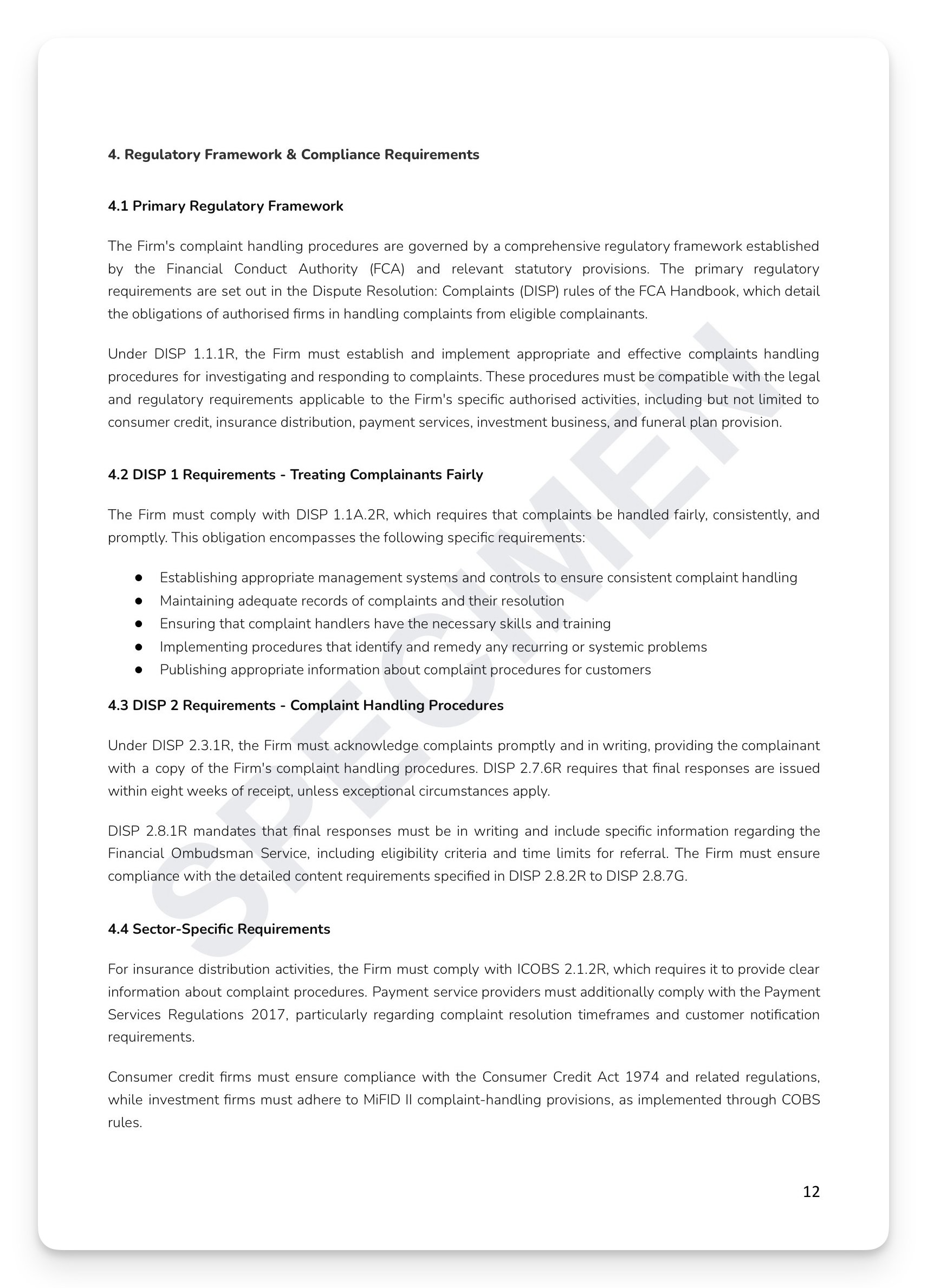

The FCA doesn't expect firms to be free of conflicts — in financial services, they're inevitable. What it expects is that firms have genuinely mapped them, that controls are proportionate to the risk, that disclosures are specific rather than generic boilerplate, and that there's a functioning register with evidence of quarterly oversight. Under PRIN 8 every FCA-authorised firm must manage conflicts fairly. Under SYSC 10, that obligation becomes structural — permanent, effective arrangements to identify, prevent, manage, and disclose. Most firms have a conflicts paragraph in their terms of business. Few have a framework that would survive supervisory scrutiny. Generic conflict disclosures don't satisfy COBS 2.3.1R. Specific ones do.

What's included:

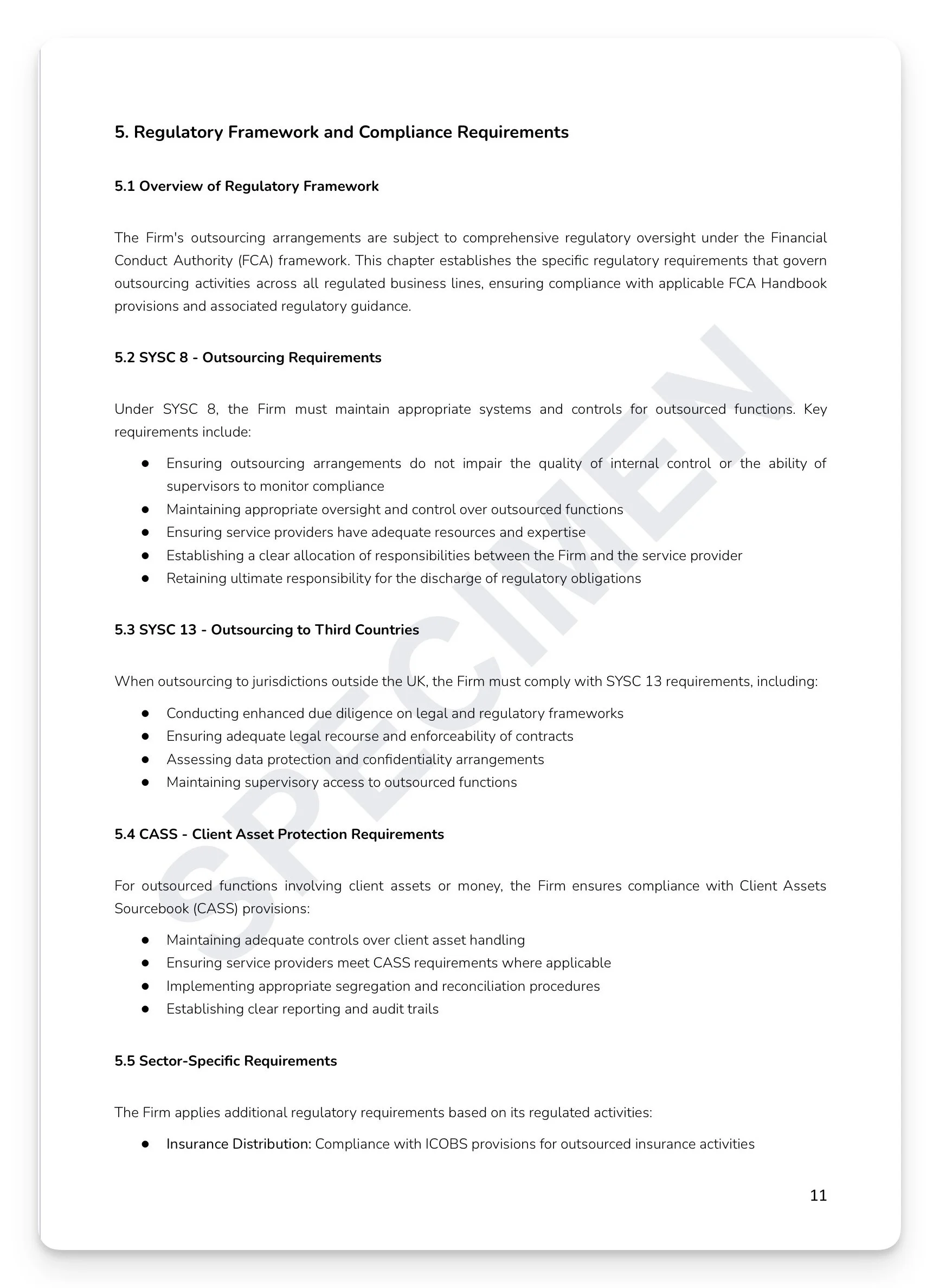

Full regulatory mapping: SYSC 10.1.3R/10.1.5R/10.1.7R, SYSC 6.1/4.1/8.1/9.1, PRIN 1/6/7/8, COBS 2.1R/2.3.1R/3, CONC 2.5/3.3, ICOBS 2.5/4.3.1R, MIFIDPRU 7, and COND 2.5

Six conflict categories: Financial, Personal, Competitive, Information, Structural, and Third-Party — each with three-stage assessment methodology and H/M/L risk rating

Conflict management hierarchy: structural separation first, Chinese walls, remuneration controls, and operational restrictions — with disclosure only as last resort

Three-tier client disclosure standard: Retail (enhanced/plain English/prominent), Professional (standard), and Eligible Counterparties (basic notification) — per COBS 3

Sector-specific conflict mapping: Consumer Credit, Insurance, Investment, Payment Services, Cryptoassets, Debt Management, and Funeral Plans

Quarterly conflicts register review with governing body reporting and annual comprehensive review

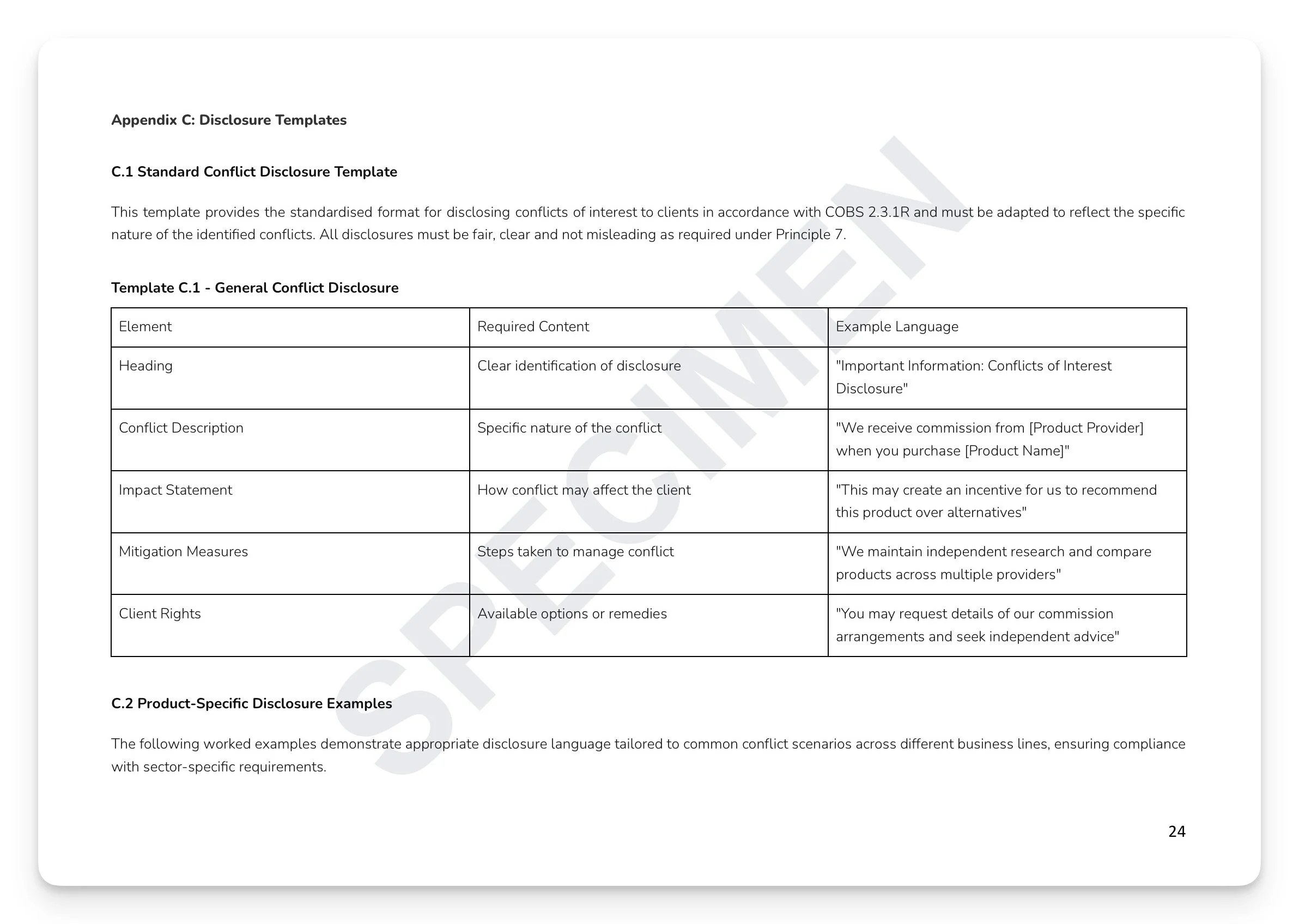

Ready-to-use appendices: Initial Conflicts Assessment Form, Master Conflicts Register Template, Standard Conflict Disclosure Template with worked examples, Disclosure Timing Matrix, and Product-Specific Conflicts Assessment Matrix across seven business types

+ much more

Who is this for?

Compliance Officers, SMF16 holders, and Boards at FCA-regulated firms — particularly investment, insurance, consumer credit, and multi-activity firms — who need a complete, board-approved Conflicts of Interest Policy that operates as a functioning management framework and gives the FCA documented evidence of genuine conflict governance.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

The FCA doesn't expect firms to be free of conflicts — in financial services, they're inevitable. What it expects is that firms have genuinely mapped them, that controls are proportionate to the risk, that disclosures are specific rather than generic boilerplate, and that there's a functioning register with evidence of quarterly oversight. Under PRIN 8 every FCA-authorised firm must manage conflicts fairly. Under SYSC 10, that obligation becomes structural — permanent, effective arrangements to identify, prevent, manage, and disclose. Most firms have a conflicts paragraph in their terms of business. Few have a framework that would survive supervisory scrutiny. Generic conflict disclosures don't satisfy COBS 2.3.1R. Specific ones do.

What's included:

Full regulatory mapping: SYSC 10.1.3R/10.1.5R/10.1.7R, SYSC 6.1/4.1/8.1/9.1, PRIN 1/6/7/8, COBS 2.1R/2.3.1R/3, CONC 2.5/3.3, ICOBS 2.5/4.3.1R, MIFIDPRU 7, and COND 2.5

Six conflict categories: Financial, Personal, Competitive, Information, Structural, and Third-Party — each with three-stage assessment methodology and H/M/L risk rating

Conflict management hierarchy: structural separation first, Chinese walls, remuneration controls, and operational restrictions — with disclosure only as last resort

Three-tier client disclosure standard: Retail (enhanced/plain English/prominent), Professional (standard), and Eligible Counterparties (basic notification) — per COBS 3

Sector-specific conflict mapping: Consumer Credit, Insurance, Investment, Payment Services, Cryptoassets, Debt Management, and Funeral Plans

Quarterly conflicts register review with governing body reporting and annual comprehensive review

Ready-to-use appendices: Initial Conflicts Assessment Form, Master Conflicts Register Template, Standard Conflict Disclosure Template with worked examples, Disclosure Timing Matrix, and Product-Specific Conflicts Assessment Matrix across seven business types

+ much more

Who is this for?

Compliance Officers, SMF16 holders, and Boards at FCA-regulated firms — particularly investment, insurance, consumer credit, and multi-activity firms — who need a complete, board-approved Conflicts of Interest Policy that operates as a functioning management framework and gives the FCA documented evidence of genuine conflict governance.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7