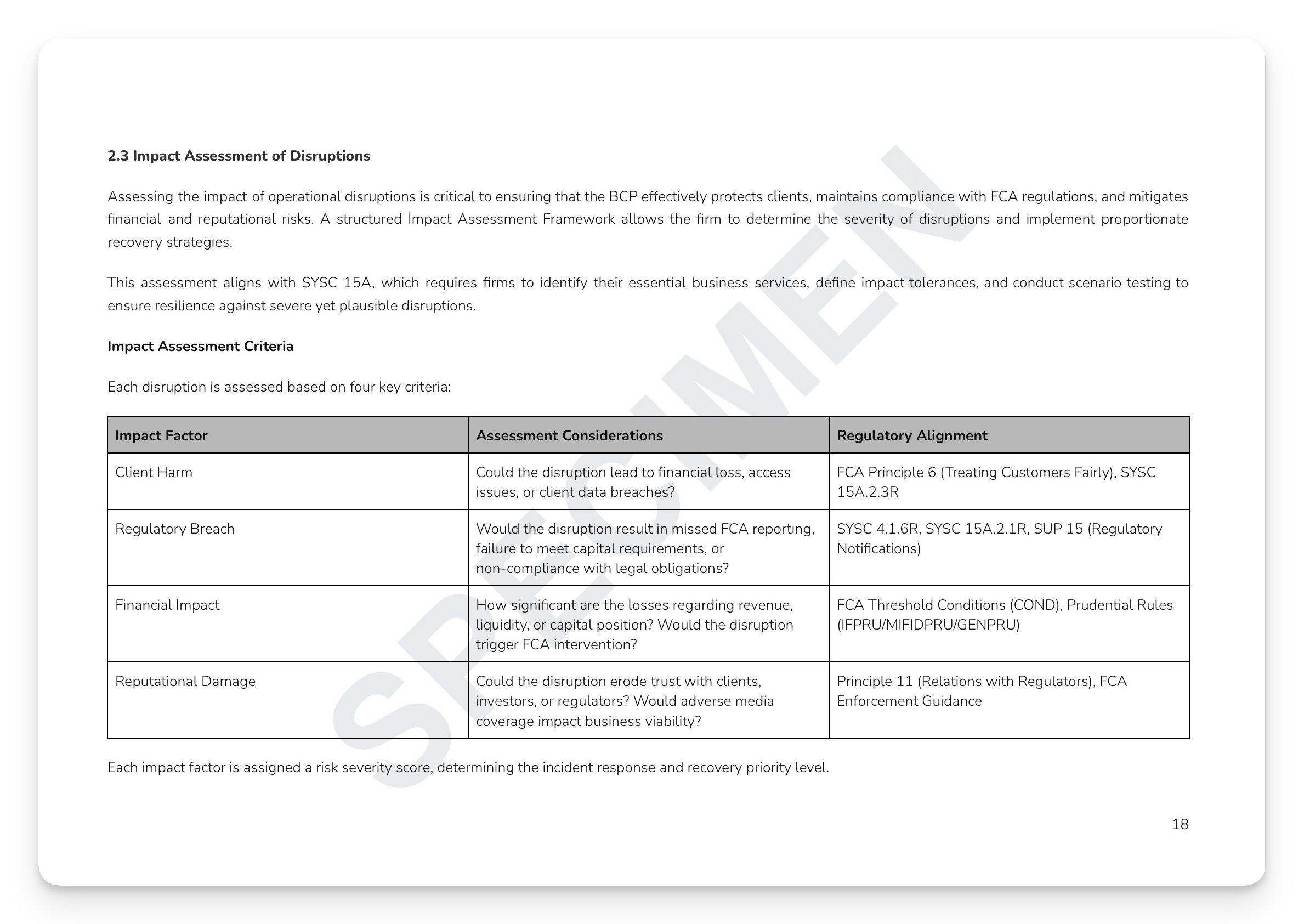

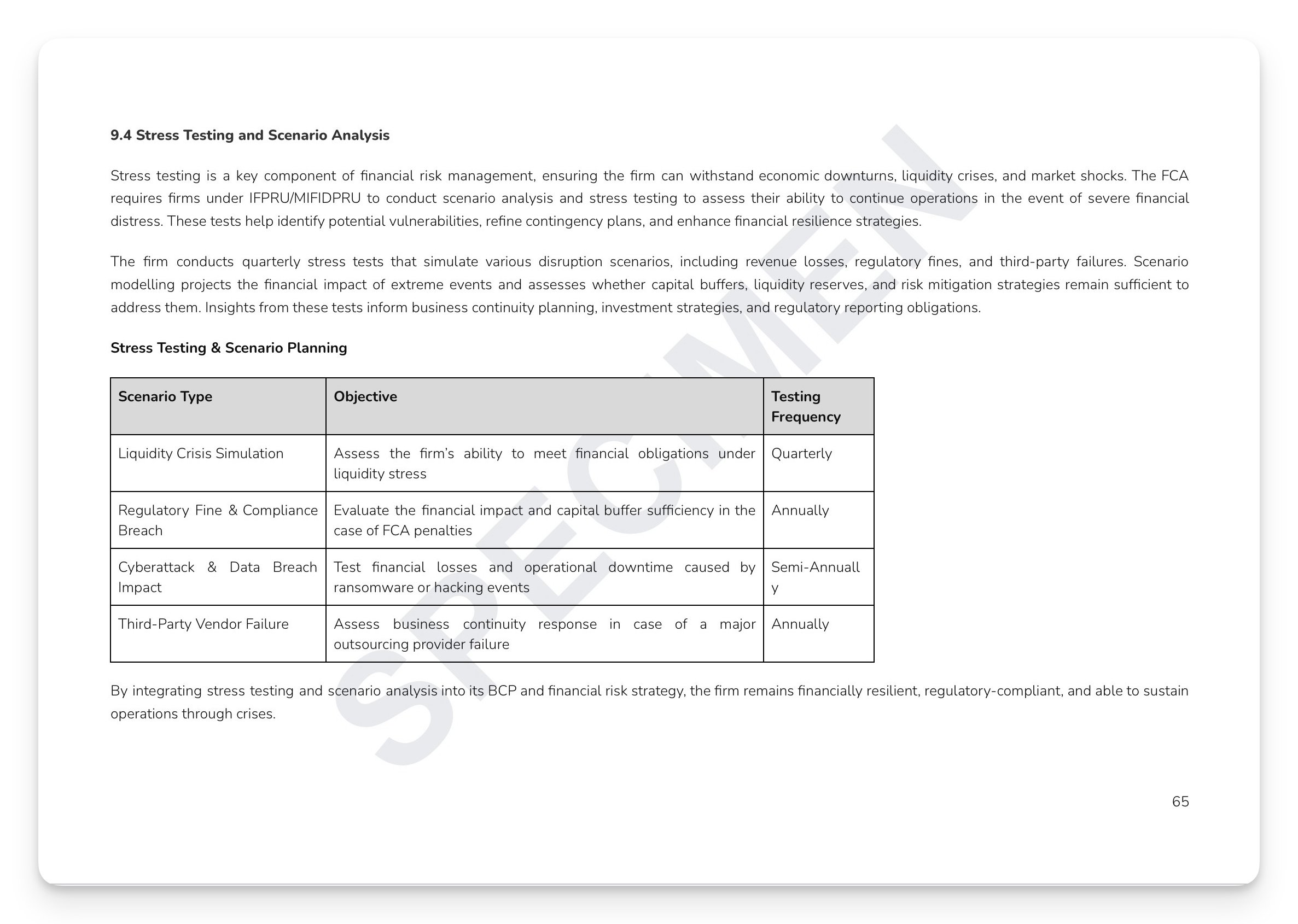

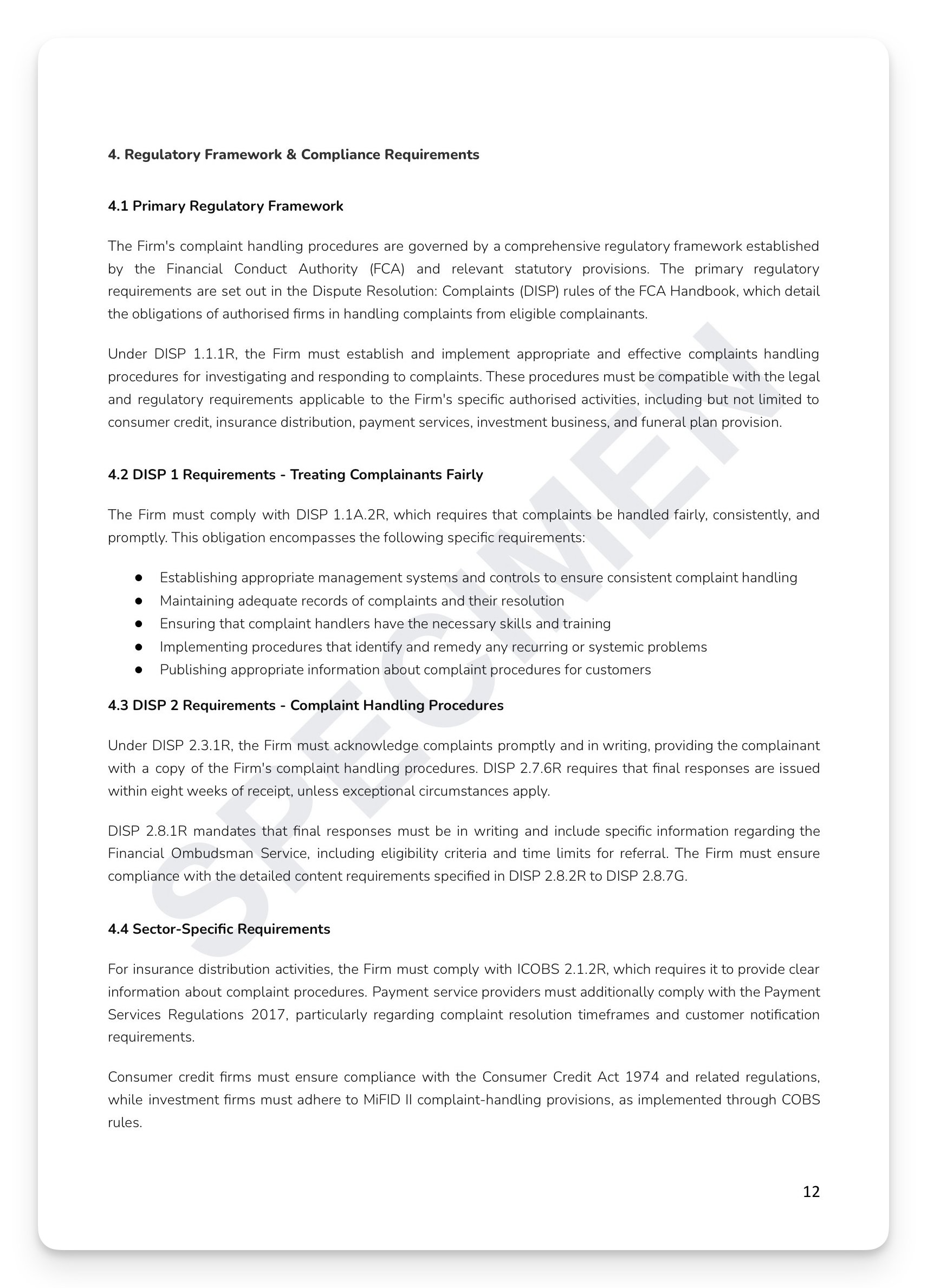

The FCA doesn't just regulate how you treat customers — it regulates what happens when you get it wrong. Under DISP 1.1.1R, every FCA-authorised firm must establish and maintain appropriate and effective procedures for investigating and responding to complaints. That obligation isn't satisfied by a generic process and a template letter. The FCA expects documented procedures, defined timeframes, consistent investigation methodology, Consumer Duty integration, and evidence that complaint data is actively used to identify and fix systemic failures. Most firms handle individual complaints reasonably well. Far fewer can demonstrate the full framework the FCA expects — and it's the framework regulators inspect, not the individual response. A complaint is not just a problem to resolve. It's evidence the FCA will use to assess your culture.

What's included:

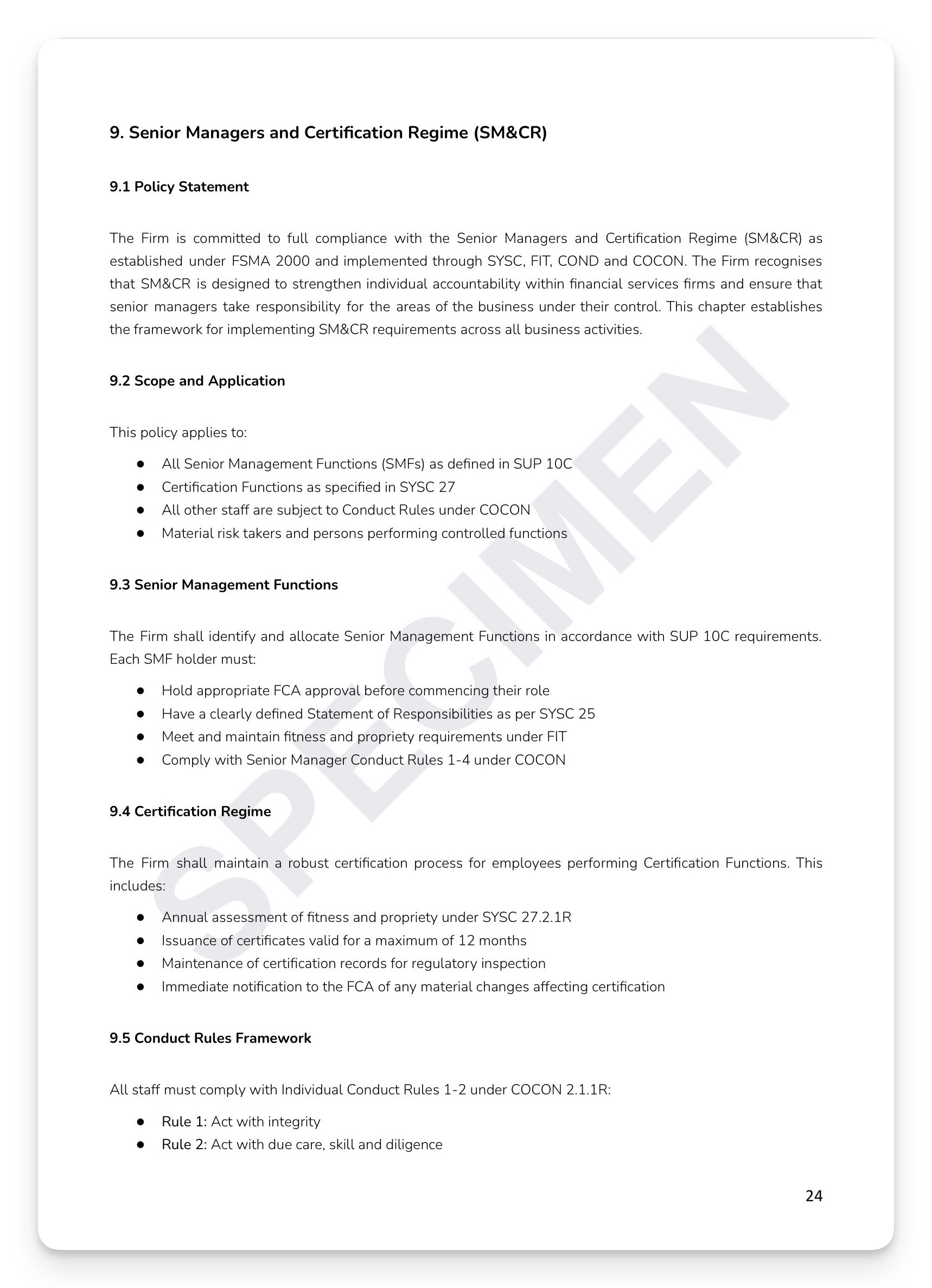

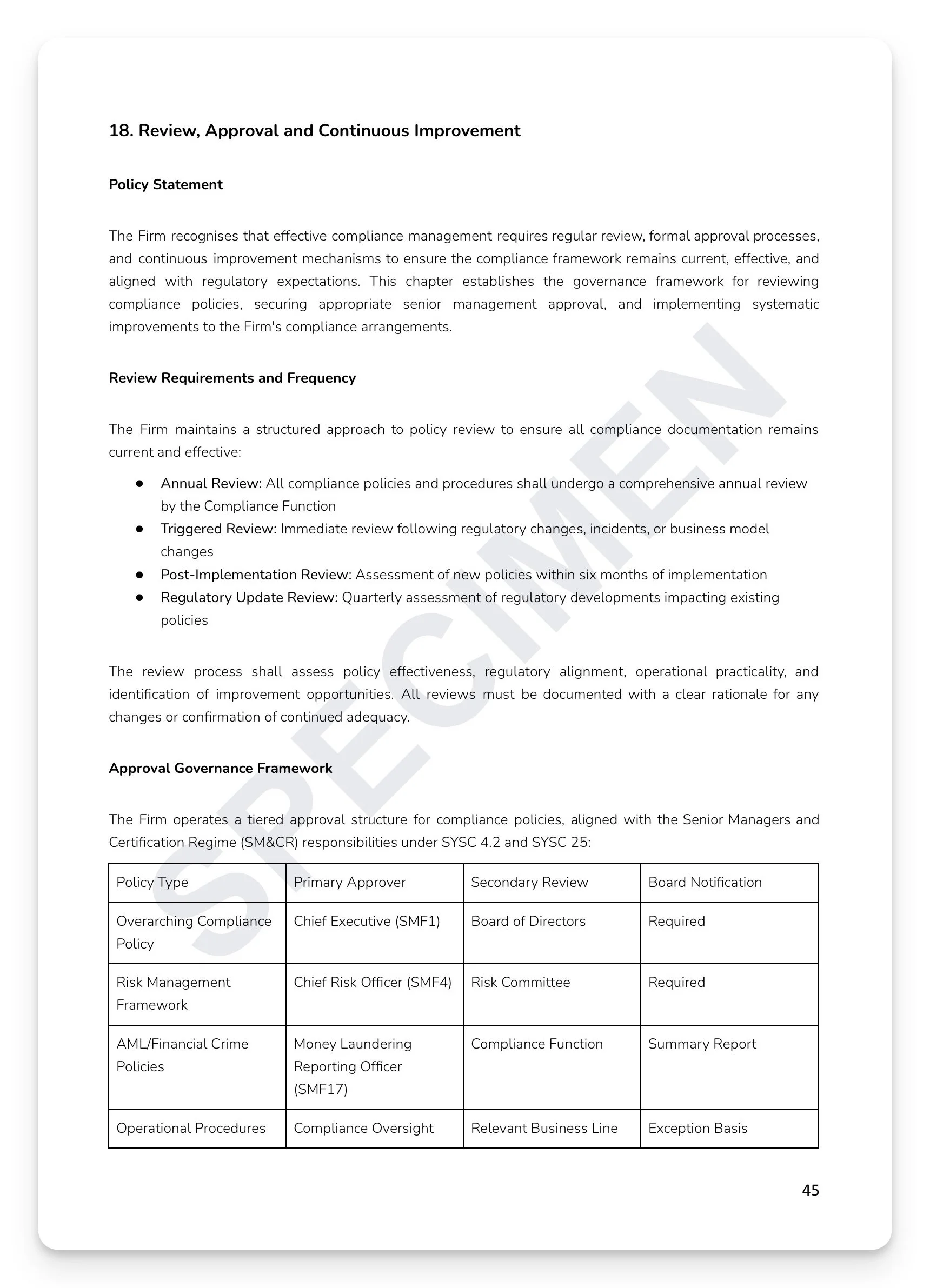

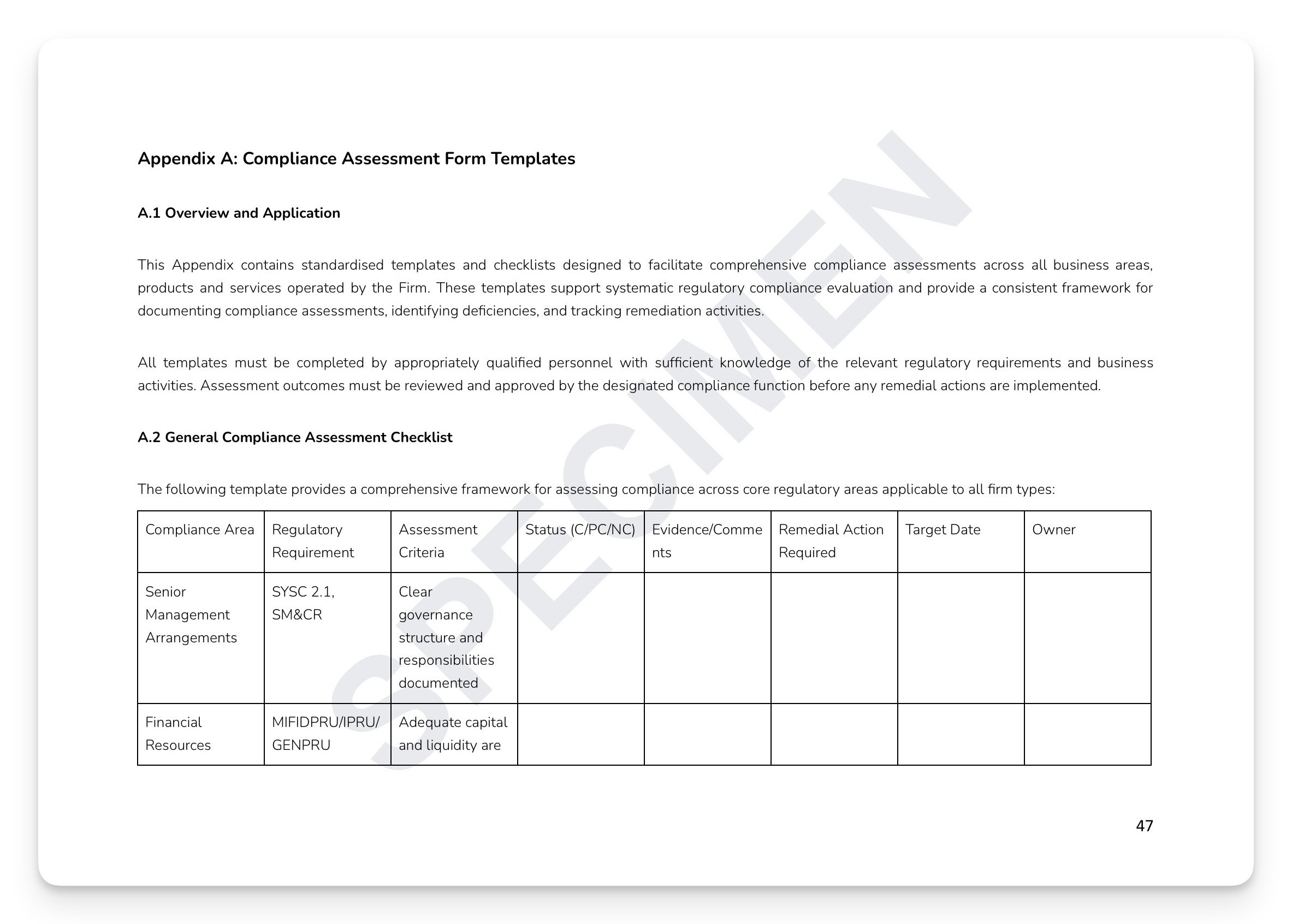

Full regulatory mapping: DISP 1.1.1R/1.1A.2R/1.4/1.6/1.9/1.10.2R/2.3.1R/2.7.6R/2.8/3, PRIN 6/7/12, Consumer Duty PRIN 2A, SUP 15.3/16, SYSC 3/9, FG22/5, PS22/9, FG21/1, and UK GDPR/DPA 2018

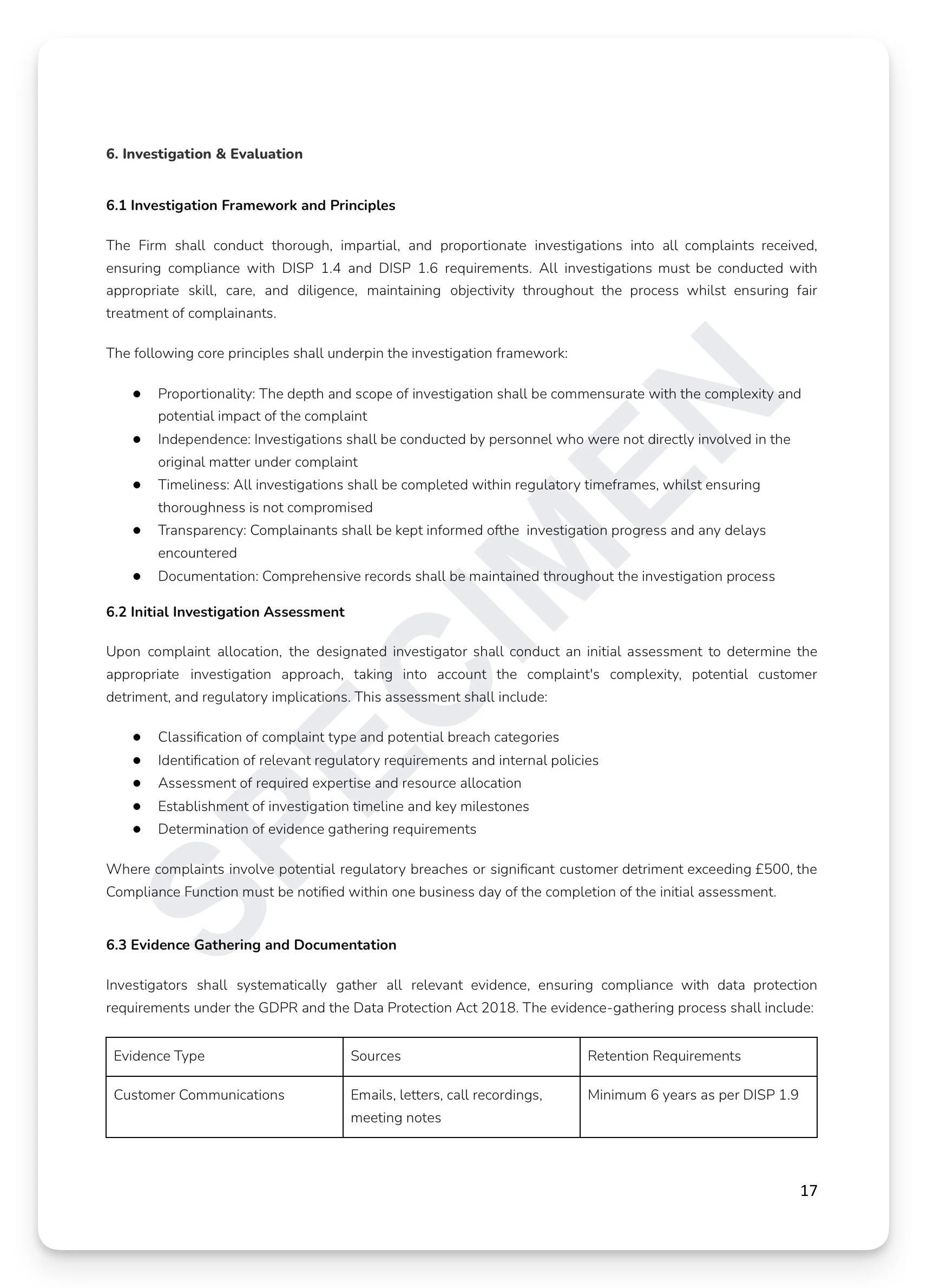

Five-stage investigation framework: initial assessment, evidence gathering, customer claim evaluation, liability determination, and remediation calculation — with direct financial loss, consequential losses, compensatory interest, and distress and inconvenience payments

Statutory response timeframes: 8 weeks standard, 15 business days payment services, and 35 business days complex payment cases — with final response mandatory content requirements under DISP 1.6.2R

Four-level escalation matrix: Team Leader (2 days) through Executive Team (immediate) — with defined criteria and authority limits at each level

Consumer Duty four-outcome integration: mapped to complaint handling at every stage of the process

Vulnerable customer procedures aligned to FG21/1: vulnerability indicator training, flexible communication methods, and outcome recording

Ready-to-use appendices: Complaint Assessment Form, Investigation Checklist (10-point), Response Template Framework, and FCA regulatory contact details

+ much more

Who is this for?

Compliance Officers, Customer Service Directors, Operations Managers, and SMF holders at FCA-regulated firms who need a complete, board-approved Complaints Handling Policy that satisfies FCA supervisory expectations, embeds Consumer Duty throughout, and turns complaint data into a genuine improvement mechanism.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

The FCA doesn't just regulate how you treat customers — it regulates what happens when you get it wrong. Under DISP 1.1.1R, every FCA-authorised firm must establish and maintain appropriate and effective procedures for investigating and responding to complaints. That obligation isn't satisfied by a generic process and a template letter. The FCA expects documented procedures, defined timeframes, consistent investigation methodology, Consumer Duty integration, and evidence that complaint data is actively used to identify and fix systemic failures. Most firms handle individual complaints reasonably well. Far fewer can demonstrate the full framework the FCA expects — and it's the framework regulators inspect, not the individual response. A complaint is not just a problem to resolve. It's evidence the FCA will use to assess your culture.

What's included:

Full regulatory mapping: DISP 1.1.1R/1.1A.2R/1.4/1.6/1.9/1.10.2R/2.3.1R/2.7.6R/2.8/3, PRIN 6/7/12, Consumer Duty PRIN 2A, SUP 15.3/16, SYSC 3/9, FG22/5, PS22/9, FG21/1, and UK GDPR/DPA 2018

Five-stage investigation framework: initial assessment, evidence gathering, customer claim evaluation, liability determination, and remediation calculation — with direct financial loss, consequential losses, compensatory interest, and distress and inconvenience payments

Statutory response timeframes: 8 weeks standard, 15 business days payment services, and 35 business days complex payment cases — with final response mandatory content requirements under DISP 1.6.2R

Four-level escalation matrix: Team Leader (2 days) through Executive Team (immediate) — with defined criteria and authority limits at each level

Consumer Duty four-outcome integration: mapped to complaint handling at every stage of the process

Vulnerable customer procedures aligned to FG21/1: vulnerability indicator training, flexible communication methods, and outcome recording

Ready-to-use appendices: Complaint Assessment Form, Investigation Checklist (10-point), Response Template Framework, and FCA regulatory contact details

+ much more

Who is this for?

Compliance Officers, Customer Service Directors, Operations Managers, and SMF holders at FCA-regulated firms who need a complete, board-approved Complaints Handling Policy that satisfies FCA supervisory expectations, embeds Consumer Duty throughout, and turns complaint data into a genuine improvement mechanism.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7