Artificial intelligence is transforming financial services — but the FCA is watching closely. Under PRIN, SYSC, Consumer Duty, and the UK GDPR, firms deploying AI face significant obligations: governance structures, bias controls, explainability requirements, vendor oversight, data protection impact assessments, and incident reporting. The regulator doesn't need to publish an AI-specific rulebook to act — the existing framework applies in full, and firms that can't demonstrate adequate oversight of their AI systems face the same enforcement consequences as any other systems and controls failure. Innovation without governance isn't a strategy — it's a risk.

What's included:

Full regulatory mapping: PRIN 1/2/6/7/8/11, SYSC 4.1.1R/6.1.1R/7.1.2R/9.1.1R/15A, Consumer Duty PRIN 2A, UK GDPR Articles 5/6/9/22/25/35, DPA 2018, Equality Act 2010, MAR, MiFID II, and COBS/CONC/ICOBS/PSRs

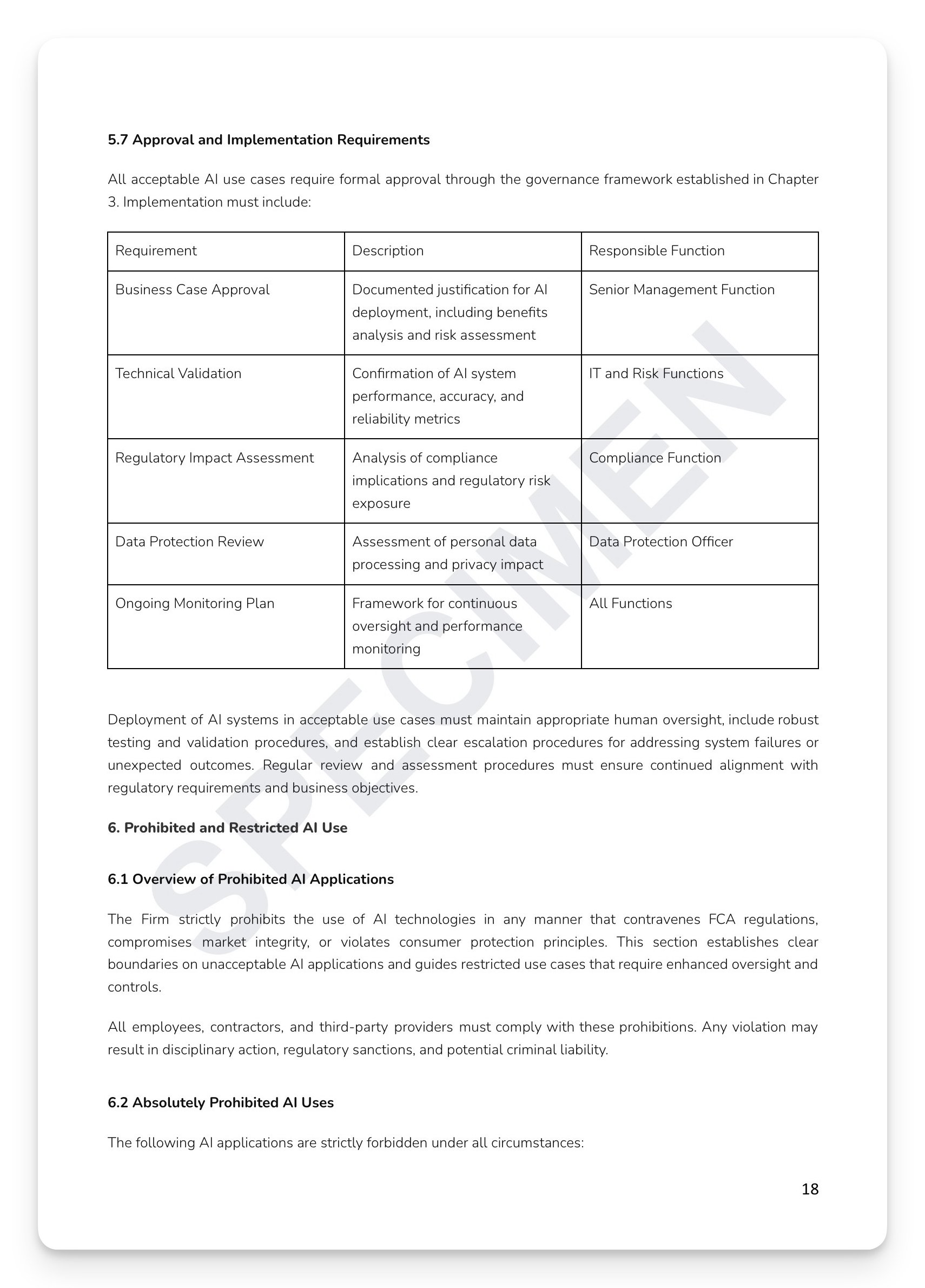

Four-level risk classification framework: Low, Medium, High, and Critical — with approval authorities from Department Manager through to the Board and absolutely prohibited applications explicitly defined

Bias identification framework: pre-deployment assessment, statistical parity testing, equal opportunity assessment, demographic parity analysis, and counterfactual fairness testing

Consumer Duty AI alignment: suitability testing, pricing fairness, communication clarity, and equitable support across all four PRIN 2A outcomes

Article 22 UK GDPR automated decision-making safeguards: human oversight requirements, data subject rights procedures, and DPIA requirements

Incident classification: Critical, High, Medium, and Low — with reporting timelines of 2/4/24 hours and FCA SUP 15.3 notification requirements (6-hour verbal, 72-hour written for critical incidents)

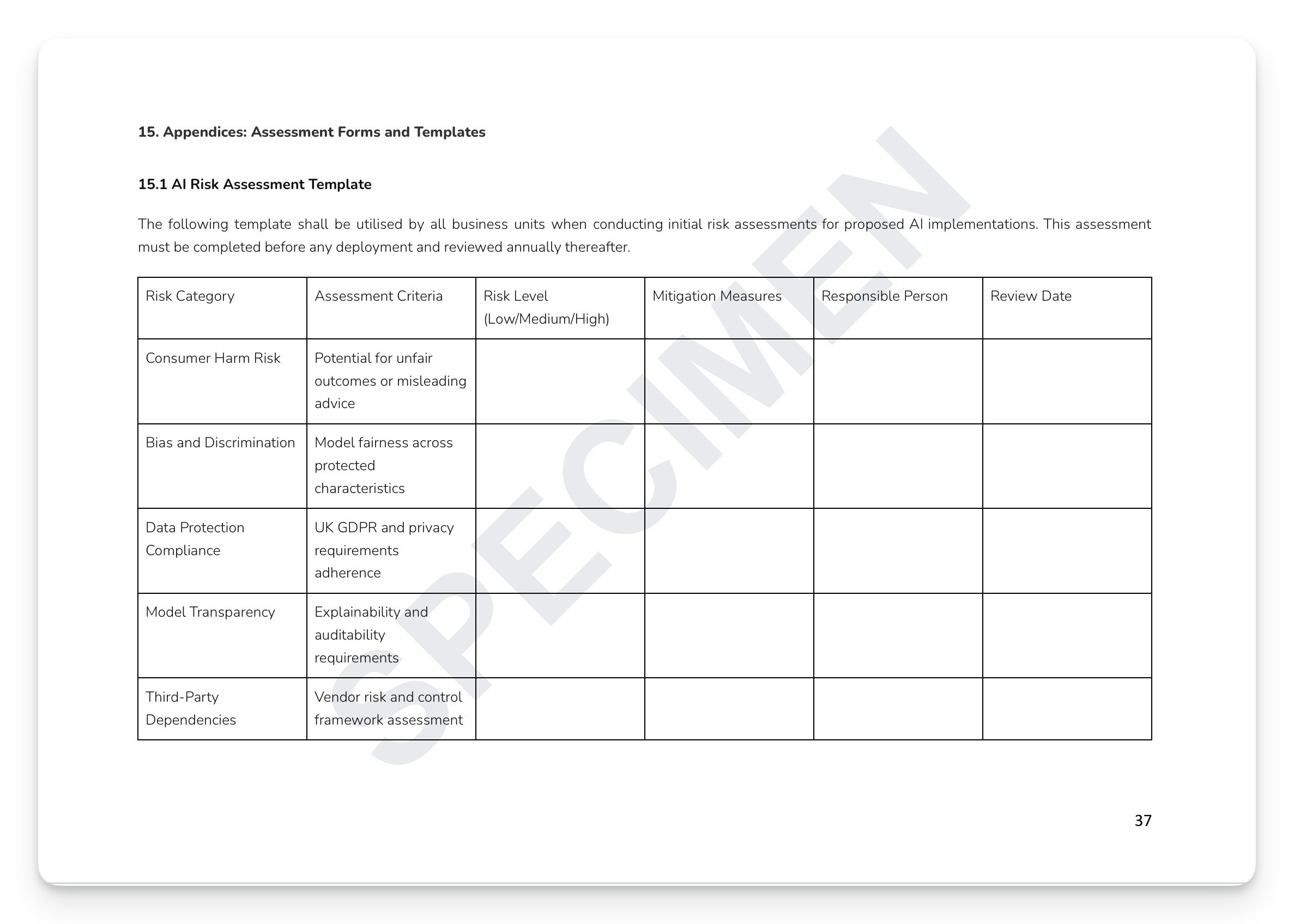

Ready-to-use appendices: AI risk assessment template, governance checklist (12-point), Consumer Duty AI assessment framework, third-party vendor due diligence template, and AI product assessment form across eight regulatory categories

+ much more

Who is this for?

Compliance Officers, Chief Risk Officers, Data Protection Officers, SMF holders, and technology teams at FCA-regulated firms deploying AI who need a complete, board-approved governance framework that demonstrates adequate systems and controls over artificial intelligence.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Artificial intelligence is transforming financial services — but the FCA is watching closely. Under PRIN, SYSC, Consumer Duty, and the UK GDPR, firms deploying AI face significant obligations: governance structures, bias controls, explainability requirements, vendor oversight, data protection impact assessments, and incident reporting. The regulator doesn't need to publish an AI-specific rulebook to act — the existing framework applies in full, and firms that can't demonstrate adequate oversight of their AI systems face the same enforcement consequences as any other systems and controls failure. Innovation without governance isn't a strategy — it's a risk.

What's included:

Full regulatory mapping: PRIN 1/2/6/7/8/11, SYSC 4.1.1R/6.1.1R/7.1.2R/9.1.1R/15A, Consumer Duty PRIN 2A, UK GDPR Articles 5/6/9/22/25/35, DPA 2018, Equality Act 2010, MAR, MiFID II, and COBS/CONC/ICOBS/PSRs

Four-level risk classification framework: Low, Medium, High, and Critical — with approval authorities from Department Manager through to the Board and absolutely prohibited applications explicitly defined

Bias identification framework: pre-deployment assessment, statistical parity testing, equal opportunity assessment, demographic parity analysis, and counterfactual fairness testing

Consumer Duty AI alignment: suitability testing, pricing fairness, communication clarity, and equitable support across all four PRIN 2A outcomes

Article 22 UK GDPR automated decision-making safeguards: human oversight requirements, data subject rights procedures, and DPIA requirements

Incident classification: Critical, High, Medium, and Low — with reporting timelines of 2/4/24 hours and FCA SUP 15.3 notification requirements (6-hour verbal, 72-hour written for critical incidents)

Ready-to-use appendices: AI risk assessment template, governance checklist (12-point), Consumer Duty AI assessment framework, third-party vendor due diligence template, and AI product assessment form across eight regulatory categories

+ much more

Who is this for?

Compliance Officers, Chief Risk Officers, Data Protection Officers, SMF holders, and technology teams at FCA-regulated firms deploying AI who need a complete, board-approved governance framework that demonstrates adequate systems and controls over artificial intelligence.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 9

Image 1 of 9

Image 2 of 9

Image 2 of 9

Image 3 of 9

Image 3 of 9

Image 4 of 9

Image 4 of 9

Image 5 of 9

Image 5 of 9

Image 6 of 9

Image 6 of 9

Image 7 of 9

Image 7 of 9

Image 8 of 9

Image 8 of 9

Image 9 of 9

Image 9 of 9