The FCA's position on arrears management has hardened significantly since the introduction of Consumer Duty. It's no longer enough to have a collections process — firms must demonstrate that every stage of arrears management, from early warning identification through forbearance, enforcement, and default, genuinely supports customer outcomes and treats customers in financial difficulty with fairness and dignity. CONC 7 sets the floor. Consumer Duty raises it. And vulnerable customers — who are disproportionately represented in arrears portfolios — are subject to a higher standard still. Collections without a documented framework aren't just operationally risky. Under the current regulatory environment, it's an enforcement waiting to happen.

A properly structured Arrears Management framework from a consultant typically costs £8,000–£15,000. This template — built by compliance and regulatory experts with over 150 years of combined experience across some of the world's most reputable financial services firms — gives you the same rigour at a fraction of the cost, ready to implement today.

What's included:

Full regulatory mapping: CONC 7 arrears treatment requirements, CONC 7.3 contact standards, Consumer Credit Act 1974 compliance, Consumer Duty PRIN 2A, PRIN 6 Treating Customers Fairly, and UK GDPR/DPA 2018

Early identification framework: proactive monitoring procedures, early warning indicator library, risk-based account flagging, and intervention strategies — before accounts reach formal arrears status

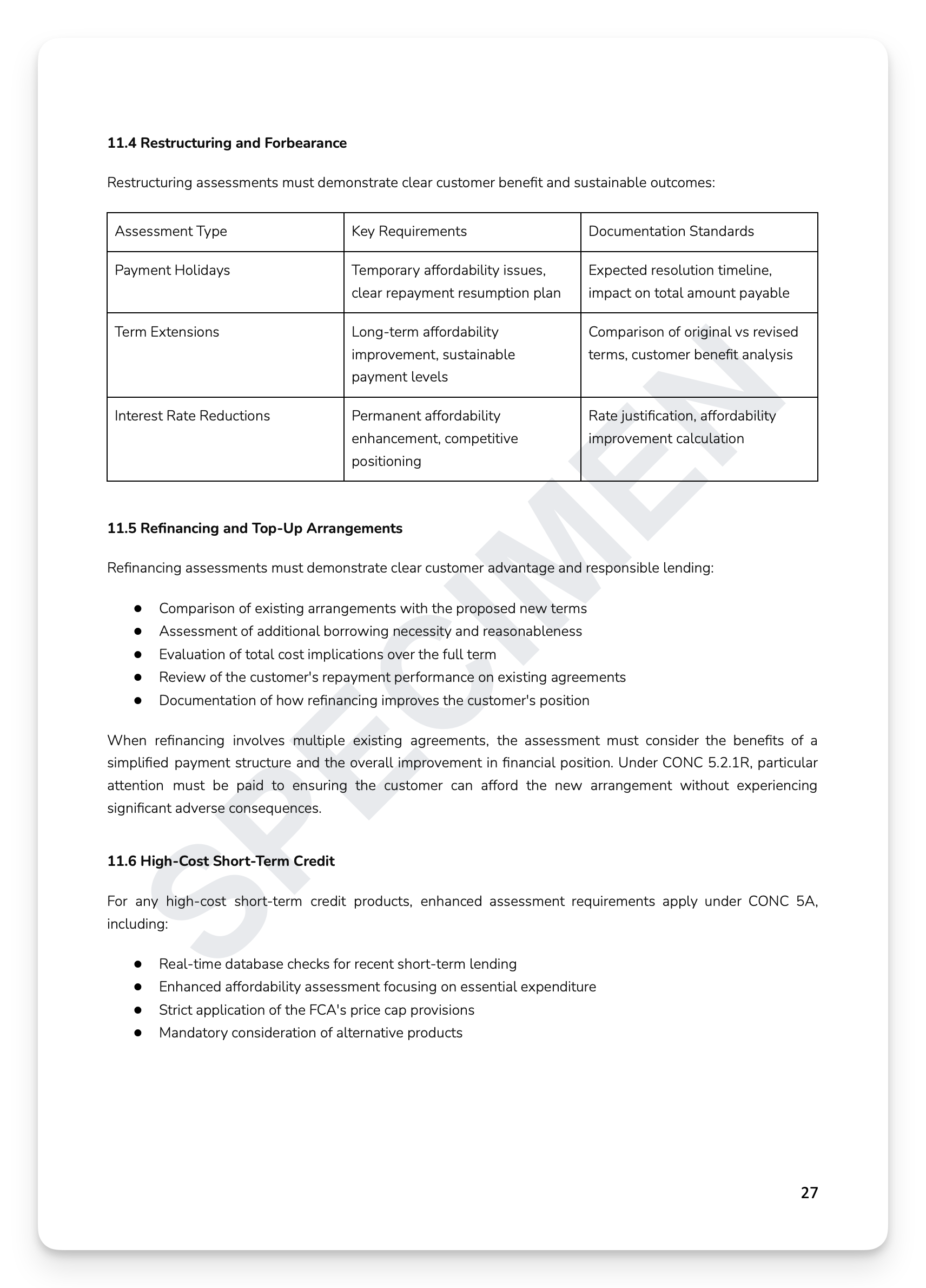

Arrears resolution and forbearance: payment deferrals, reduced payment arrangements, interest suspension, term extensions, and debt restructuring — with assessment, approval, implementation, and monitoring procedures for each

Vulnerability assessment framework: financial difficulty identification, four-driver vulnerability model, enhanced protections, tailored communication standards, and referral to specialist support

Collections, escalation, and enforcement: third-party collections governance, enforcement action criteria, legal proceedings standards, and Consumer Credit Act default notice requirements

Default and termination procedures: pre-default assessment, mandatory notice requirements, post-default customer rights, and Credit Reference Agency reporting obligations

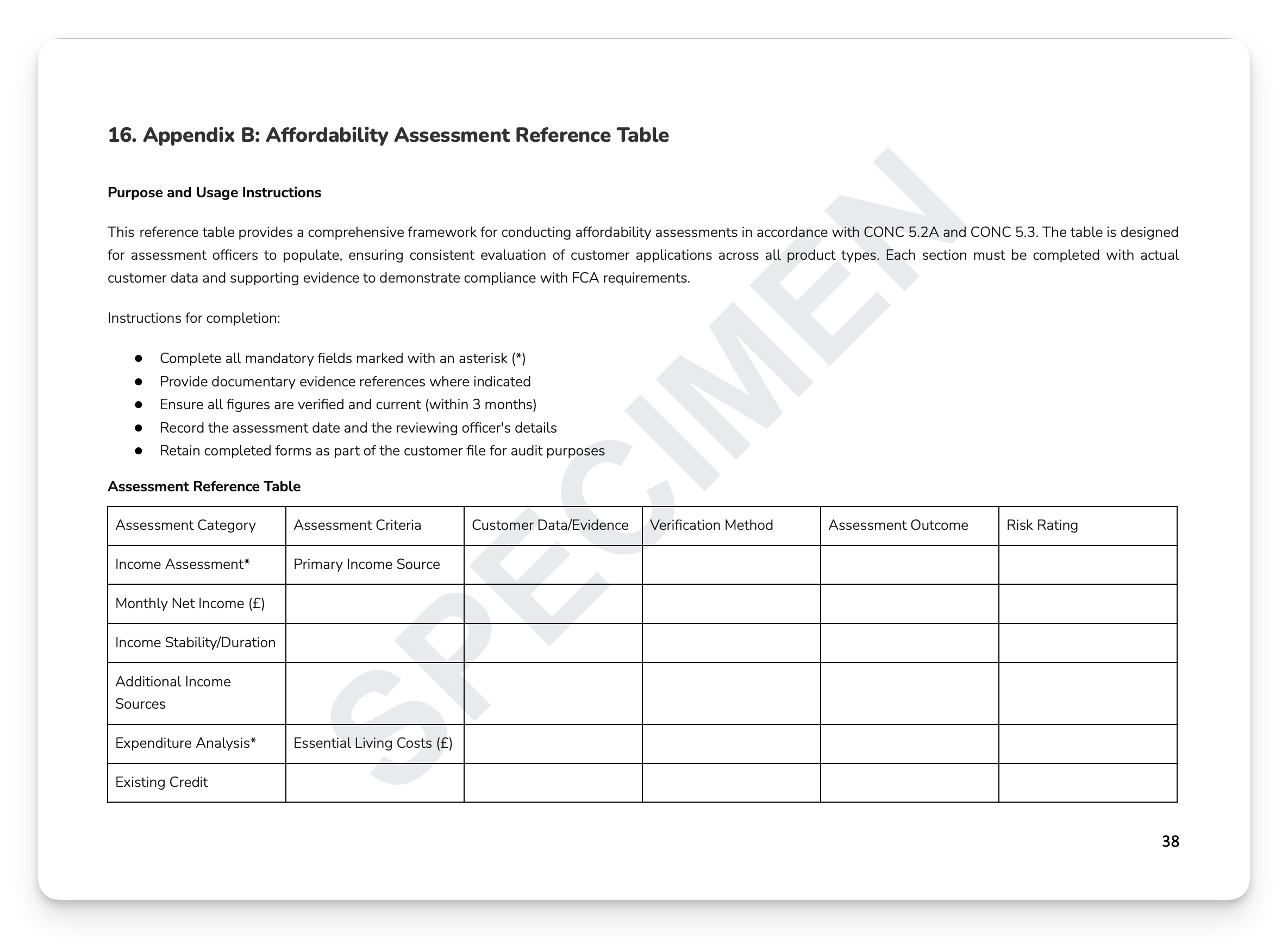

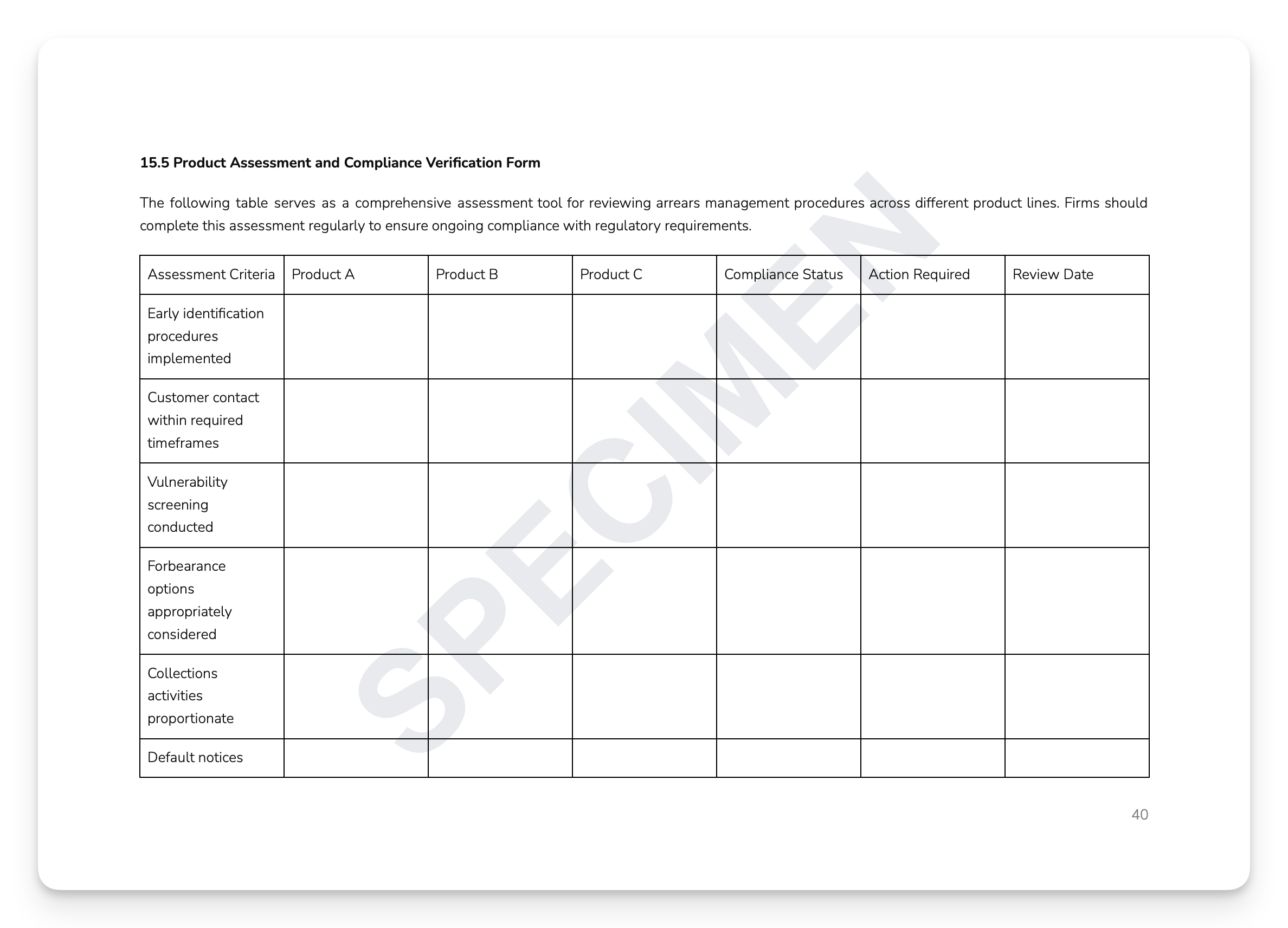

Ready-to-use appendices: Financial Difficulty Assessment Checklist, Vulnerability Assessment Matrix, Forbearance Options Template, and Product Assessment and Compliance Verification Form + much more

Who is this for?

Compliance Officers, Collections Managers, SMF holders, and operational teams at FCA-regulated consumer credit firms who need a complete, board-approved Arrears Management Policy that satisfies CONC 7, Consumer Duty, and FCA supervisory expectations — from first missed payment through to default.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

The FCA's position on arrears management has hardened significantly since the introduction of Consumer Duty. It's no longer enough to have a collections process — firms must demonstrate that every stage of arrears management, from early warning identification through forbearance, enforcement, and default, genuinely supports customer outcomes and treats customers in financial difficulty with fairness and dignity. CONC 7 sets the floor. Consumer Duty raises it. And vulnerable customers — who are disproportionately represented in arrears portfolios — are subject to a higher standard still. Collections without a documented framework aren't just operationally risky. Under the current regulatory environment, it's an enforcement waiting to happen.

A properly structured Arrears Management framework from a consultant typically costs £8,000–£15,000. This template — built by compliance and regulatory experts with over 150 years of combined experience across some of the world's most reputable financial services firms — gives you the same rigour at a fraction of the cost, ready to implement today.

What's included:

Full regulatory mapping: CONC 7 arrears treatment requirements, CONC 7.3 contact standards, Consumer Credit Act 1974 compliance, Consumer Duty PRIN 2A, PRIN 6 Treating Customers Fairly, and UK GDPR/DPA 2018

Early identification framework: proactive monitoring procedures, early warning indicator library, risk-based account flagging, and intervention strategies — before accounts reach formal arrears status

Arrears resolution and forbearance: payment deferrals, reduced payment arrangements, interest suspension, term extensions, and debt restructuring — with assessment, approval, implementation, and monitoring procedures for each

Vulnerability assessment framework: financial difficulty identification, four-driver vulnerability model, enhanced protections, tailored communication standards, and referral to specialist support

Collections, escalation, and enforcement: third-party collections governance, enforcement action criteria, legal proceedings standards, and Consumer Credit Act default notice requirements

Default and termination procedures: pre-default assessment, mandatory notice requirements, post-default customer rights, and Credit Reference Agency reporting obligations

Ready-to-use appendices: Financial Difficulty Assessment Checklist, Vulnerability Assessment Matrix, Forbearance Options Template, and Product Assessment and Compliance Verification Form + much more

Who is this for?

Compliance Officers, Collections Managers, SMF holders, and operational teams at FCA-regulated consumer credit firms who need a complete, board-approved Arrears Management Policy that satisfies CONC 7, Consumer Duty, and FCA supervisory expectations — from first missed payment through to default.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 10

Image 1 of 10

Image 2 of 10

Image 2 of 10

Image 3 of 10

Image 3 of 10

Image 4 of 10

Image 4 of 10

Image 5 of 10

Image 5 of 10

Image 6 of 10

Image 6 of 10

Image 7 of 10

Image 7 of 10

Image 8 of 10

Image 8 of 10

Image 9 of 10

Image 9 of 10

Image 10 of 10

Image 10 of 10