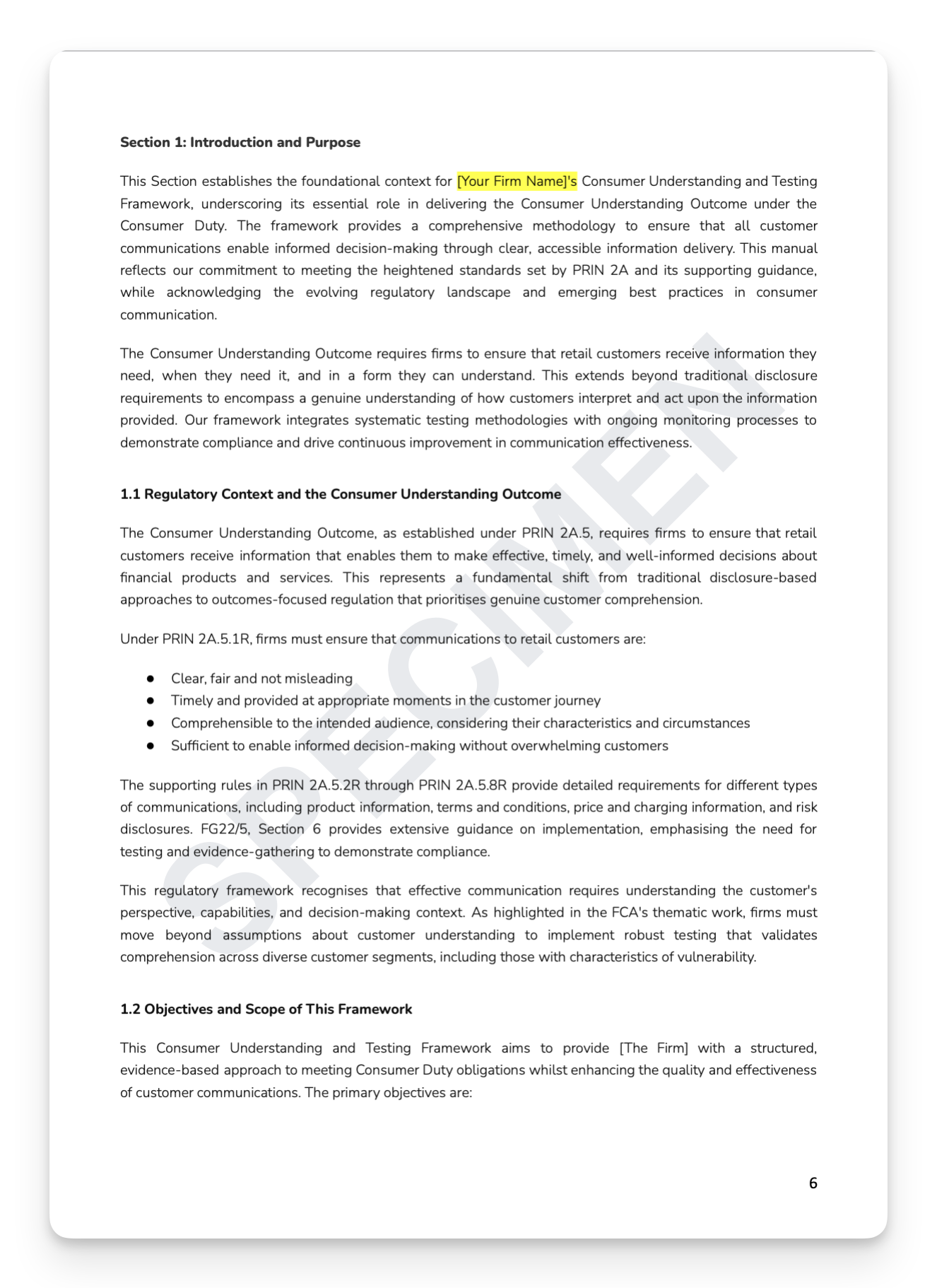

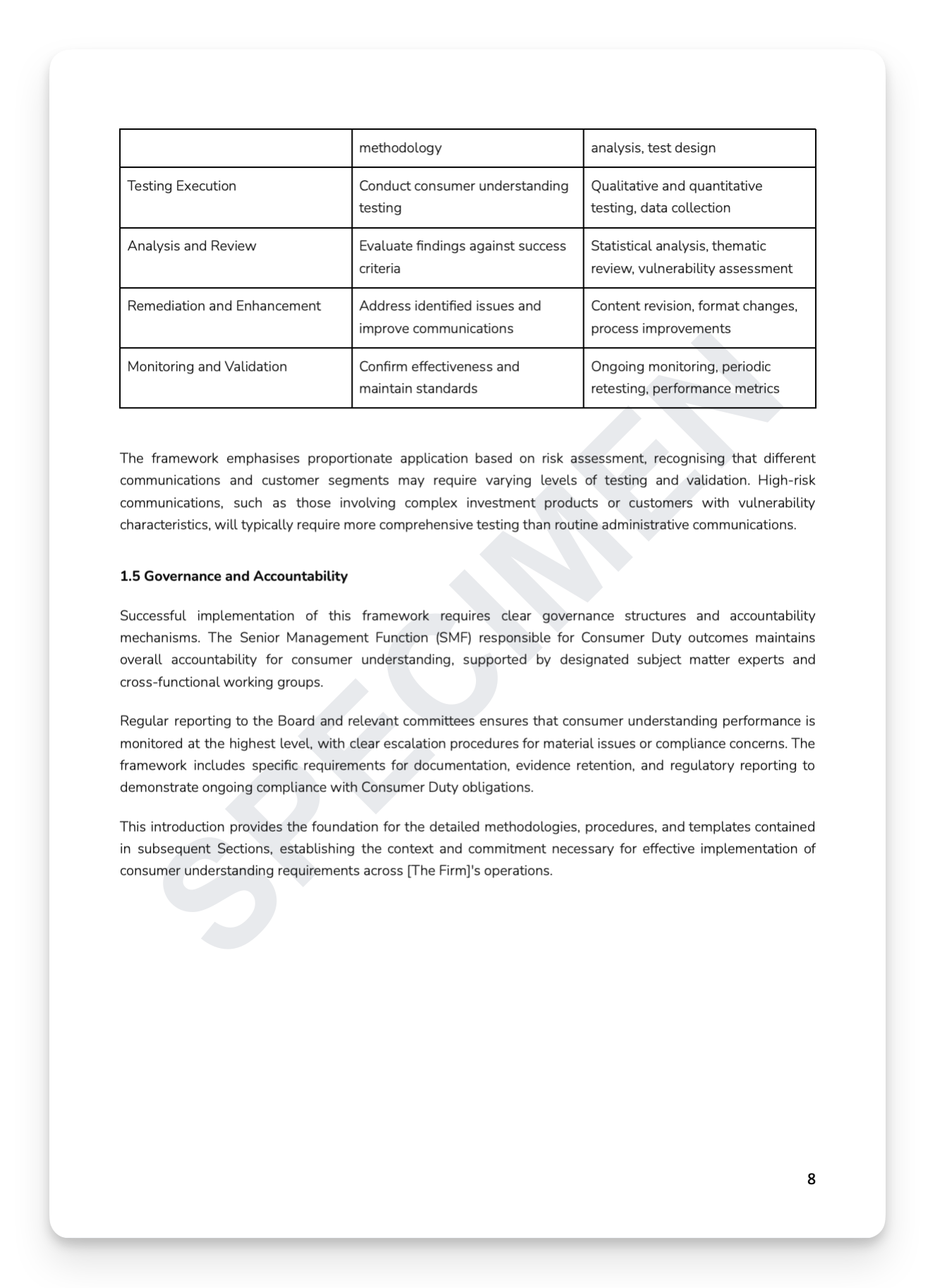

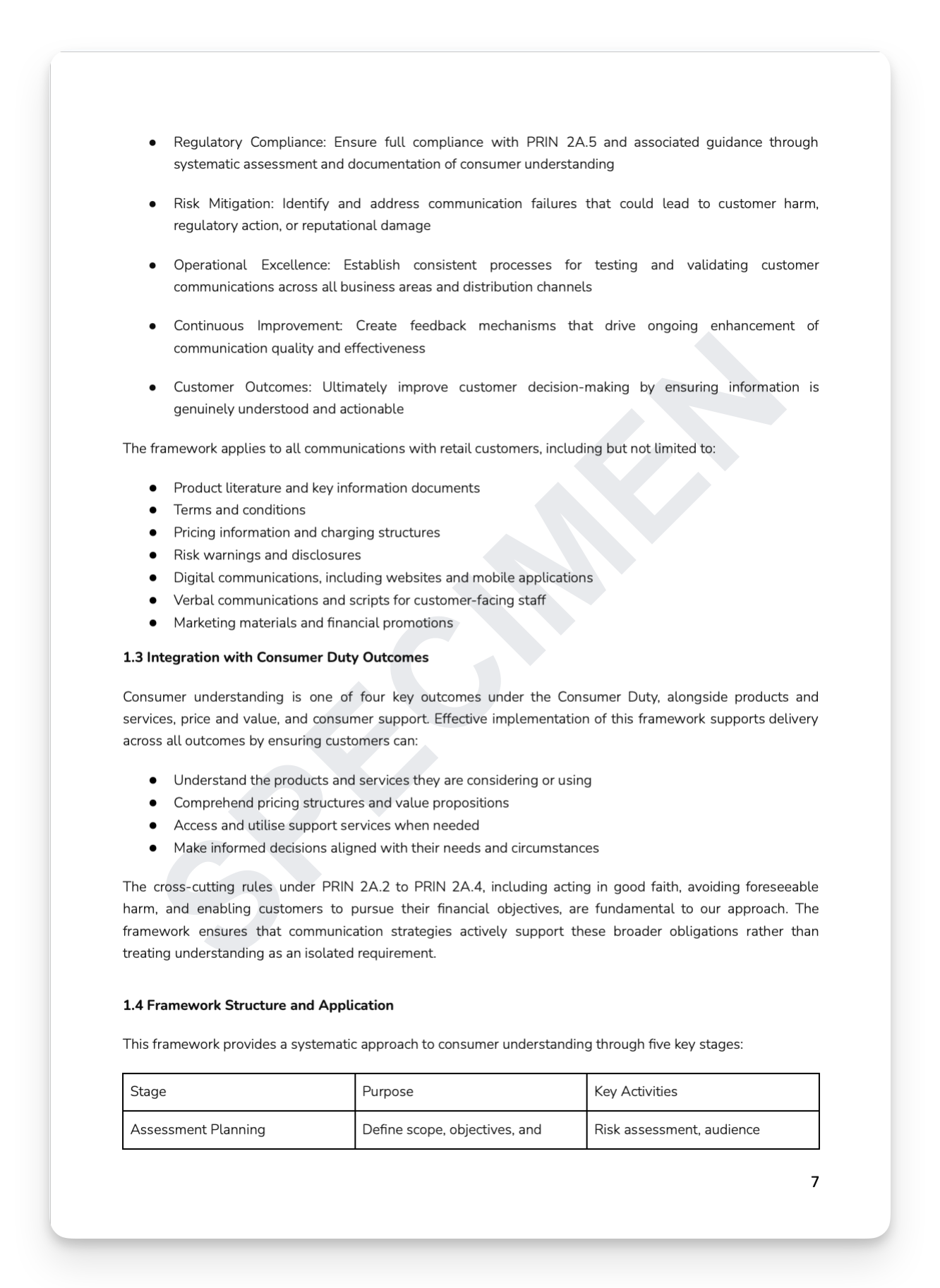

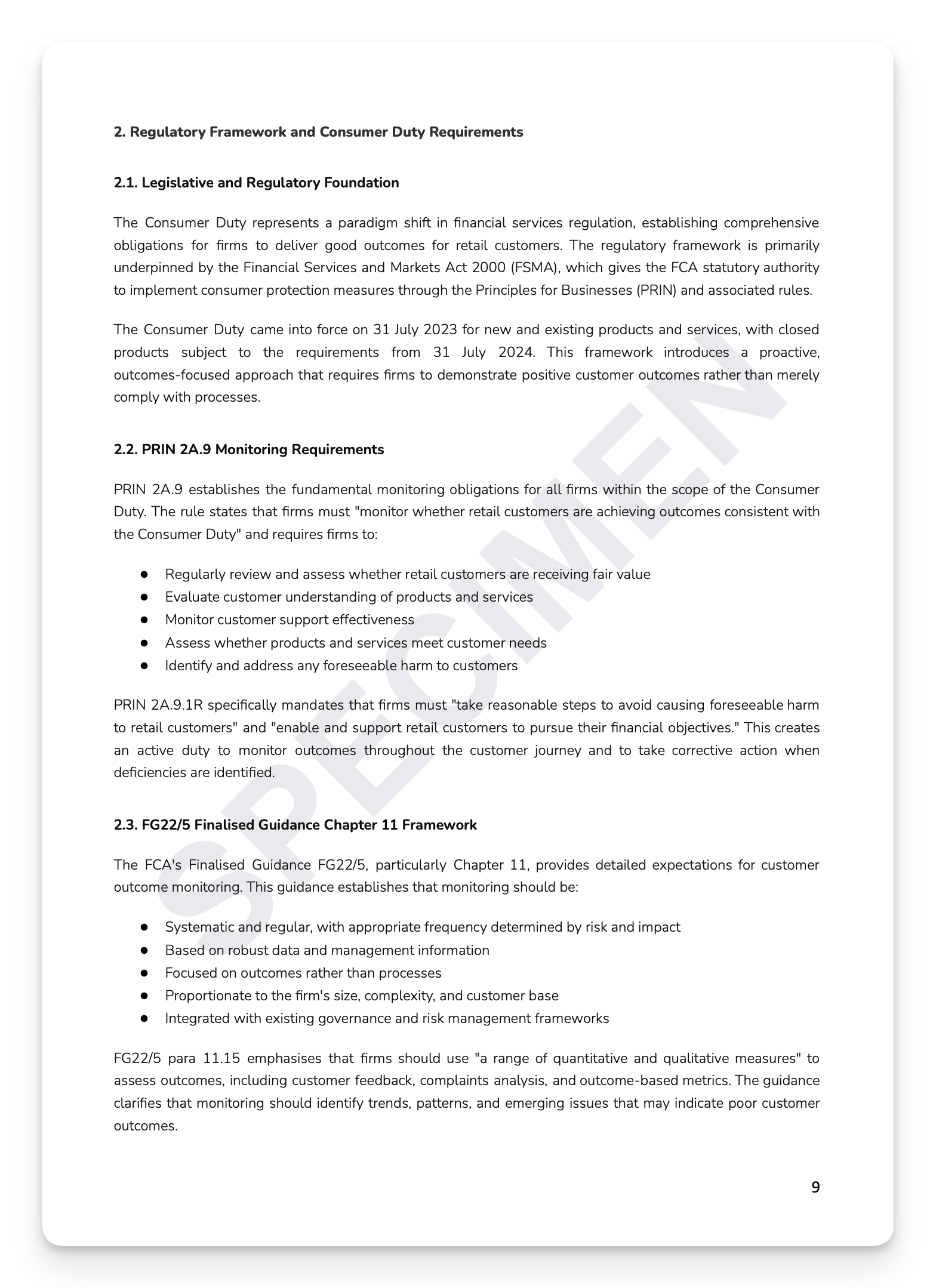

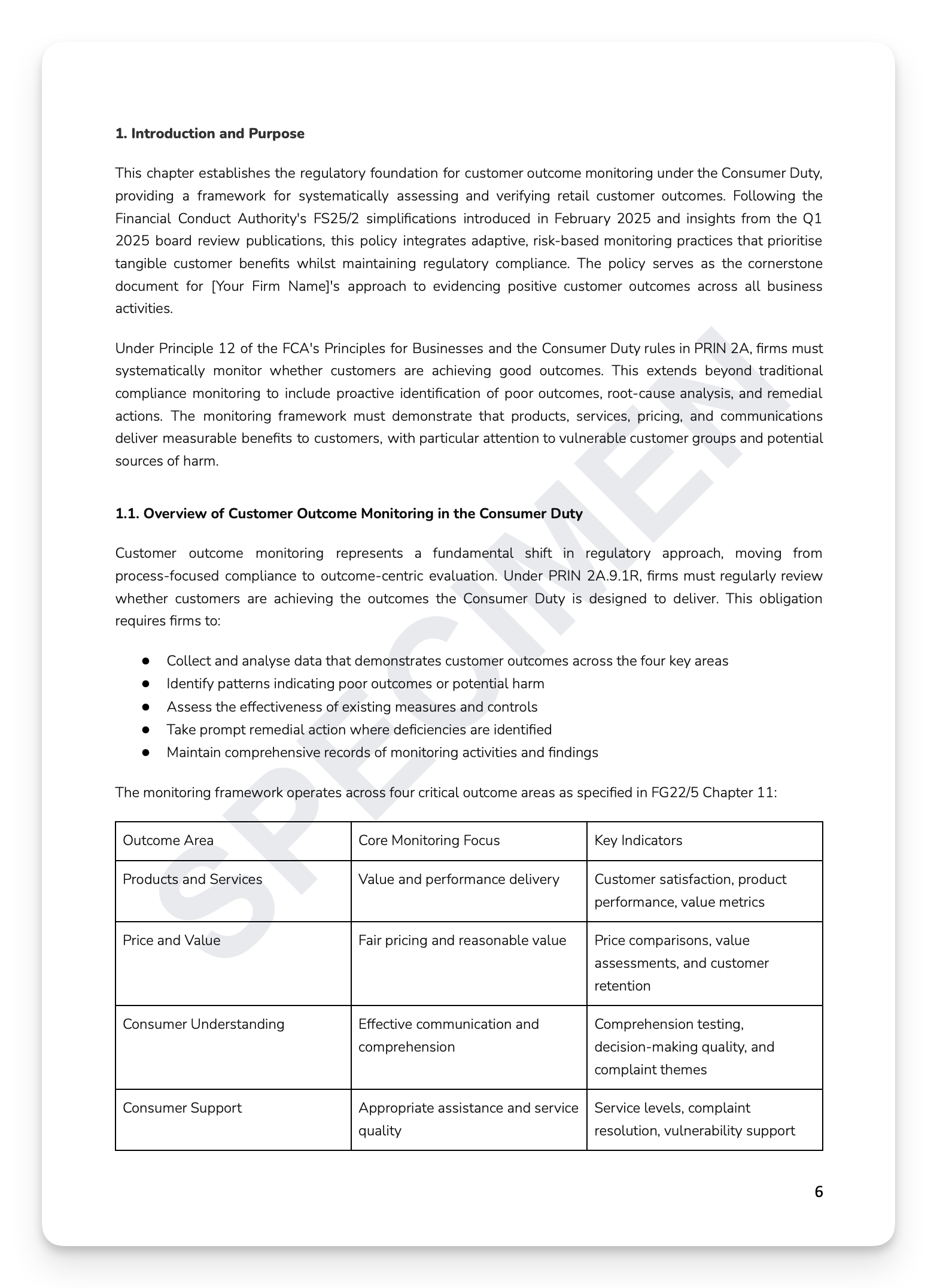

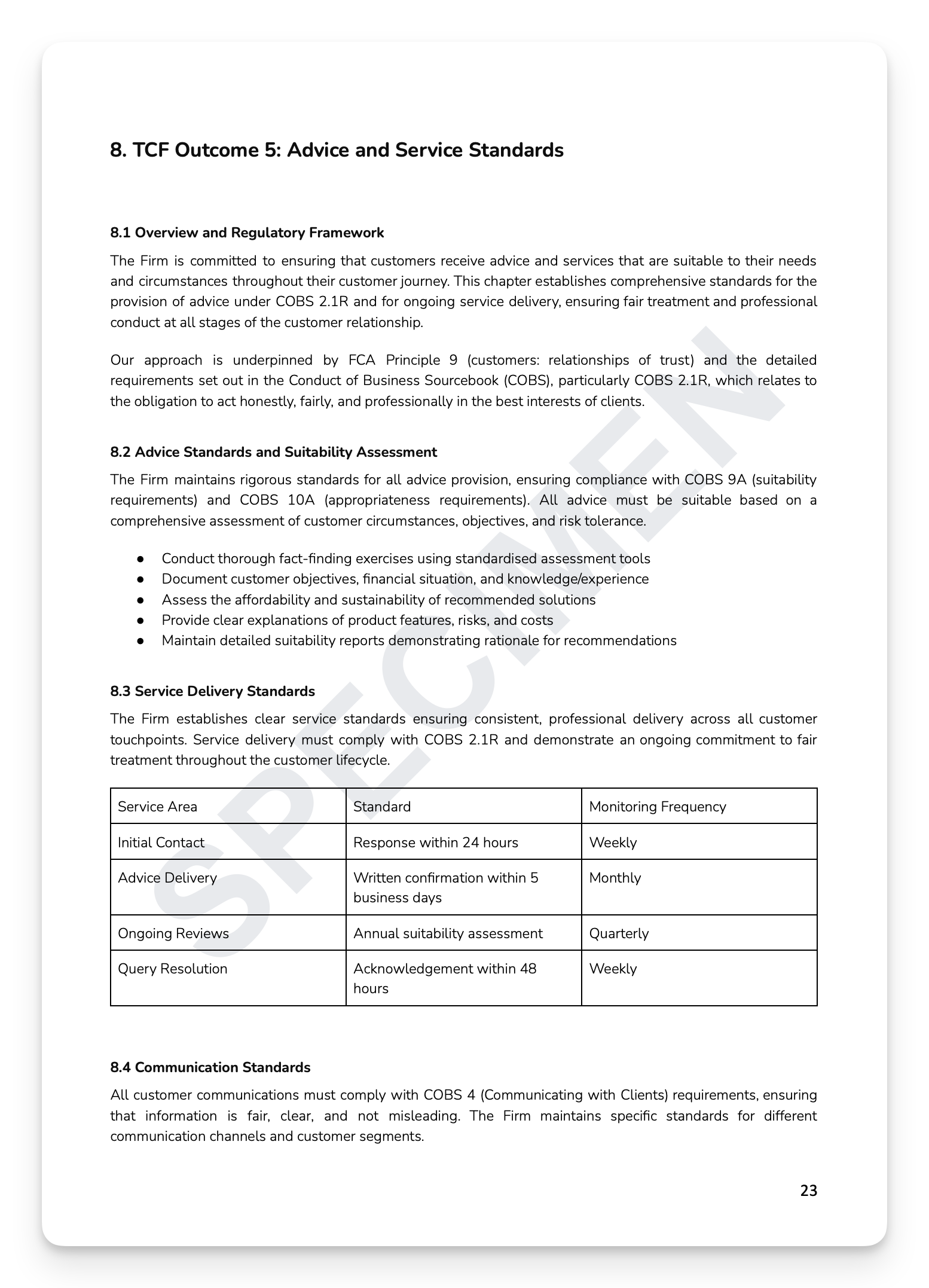

TCF's six outcomes remain live regulatory obligations — and Consumer Duty has raised the bar further. Firms must now demonstrate fair treatment through evidenced customer outcomes across every stage of the product and service lifecycle, with both frameworks operating in parallel. Firms that cannot evidence both simultaneously are exposed on two fronts. The FCA doesn't wait.

A consultant-built TCF Policy with Consumer Duty integration typically costs £6,000–£12,000. This template — built by compliance and regulatory experts with over 150 years of combined experience across some of the world's most reputable financial services firms — gives you the same rigour at a fraction of the cost, ready to implement today.

What's included:

Full regulatory framework: FCA Principles 2, 6, 7, and 12 — with RPPD and Consumer Duty cross-cutting rules integration

All six TCF outcomes: consumer promotion, product design and governance, product information and suitability, complaints handling, advice and service standards, and vulnerable customers and fair value

Consumer Duty implementation: cross-cutting rules, four outcomes, monitoring requirements, and governance and accountability

Governance and accountability: Board oversight, three-lines-of-defence model, TCF Committee structure, and performance management

Training and competence: role-specific training, competence assessment, and training records and documentation

Monitoring, audit, and assurance: first, second, and third line frameworks, KPIs, and management information and reporting

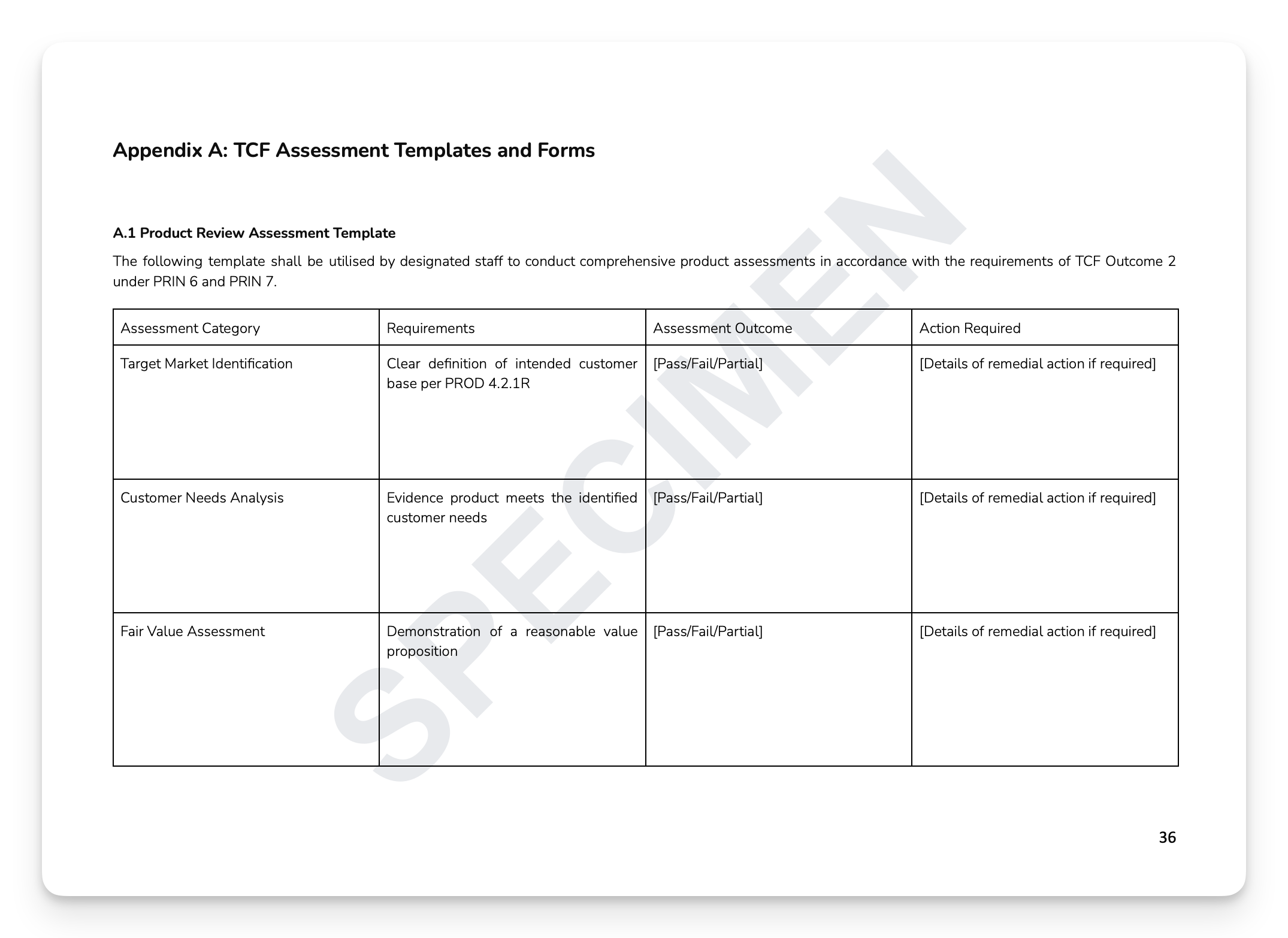

Ready-to-use appendices: Product Review Assessment Template and Customer Vulnerability Assessment Form

+ much more

Who is this for?

Compliance Officers, Consumer Duty leads, SMF holders, and Boards at FCA-regulated firms who need a complete policy satisfying both legacy TCF obligations and current Consumer Duty expectations.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

TCF's six outcomes remain live regulatory obligations — and Consumer Duty has raised the bar further. Firms must now demonstrate fair treatment through evidenced customer outcomes across every stage of the product and service lifecycle, with both frameworks operating in parallel. Firms that cannot evidence both simultaneously are exposed on two fronts. The FCA doesn't wait.

A consultant-built TCF Policy with Consumer Duty integration typically costs £6,000–£12,000. This template — built by compliance and regulatory experts with over 150 years of combined experience across some of the world's most reputable financial services firms — gives you the same rigour at a fraction of the cost, ready to implement today.

What's included:

Full regulatory framework: FCA Principles 2, 6, 7, and 12 — with RPPD and Consumer Duty cross-cutting rules integration

All six TCF outcomes: consumer promotion, product design and governance, product information and suitability, complaints handling, advice and service standards, and vulnerable customers and fair value

Consumer Duty implementation: cross-cutting rules, four outcomes, monitoring requirements, and governance and accountability

Governance and accountability: Board oversight, three-lines-of-defence model, TCF Committee structure, and performance management

Training and competence: role-specific training, competence assessment, and training records and documentation

Monitoring, audit, and assurance: first, second, and third line frameworks, KPIs, and management information and reporting

Ready-to-use appendices: Product Review Assessment Template and Customer Vulnerability Assessment Form

+ much more

Who is this for?

Compliance Officers, Consumer Duty leads, SMF holders, and Boards at FCA-regulated firms who need a complete policy satisfying both legacy TCF obligations and current Consumer Duty expectations.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 8

Image 1 of 8

Image 2 of 8

Image 2 of 8

Image 3 of 8

Image 3 of 8

Image 4 of 8

Image 4 of 8

Image 5 of 8

Image 5 of 8

Image 6 of 8

Image 6 of 8

Image 7 of 8

Image 7 of 8

Image 8 of 8

Image 8 of 8