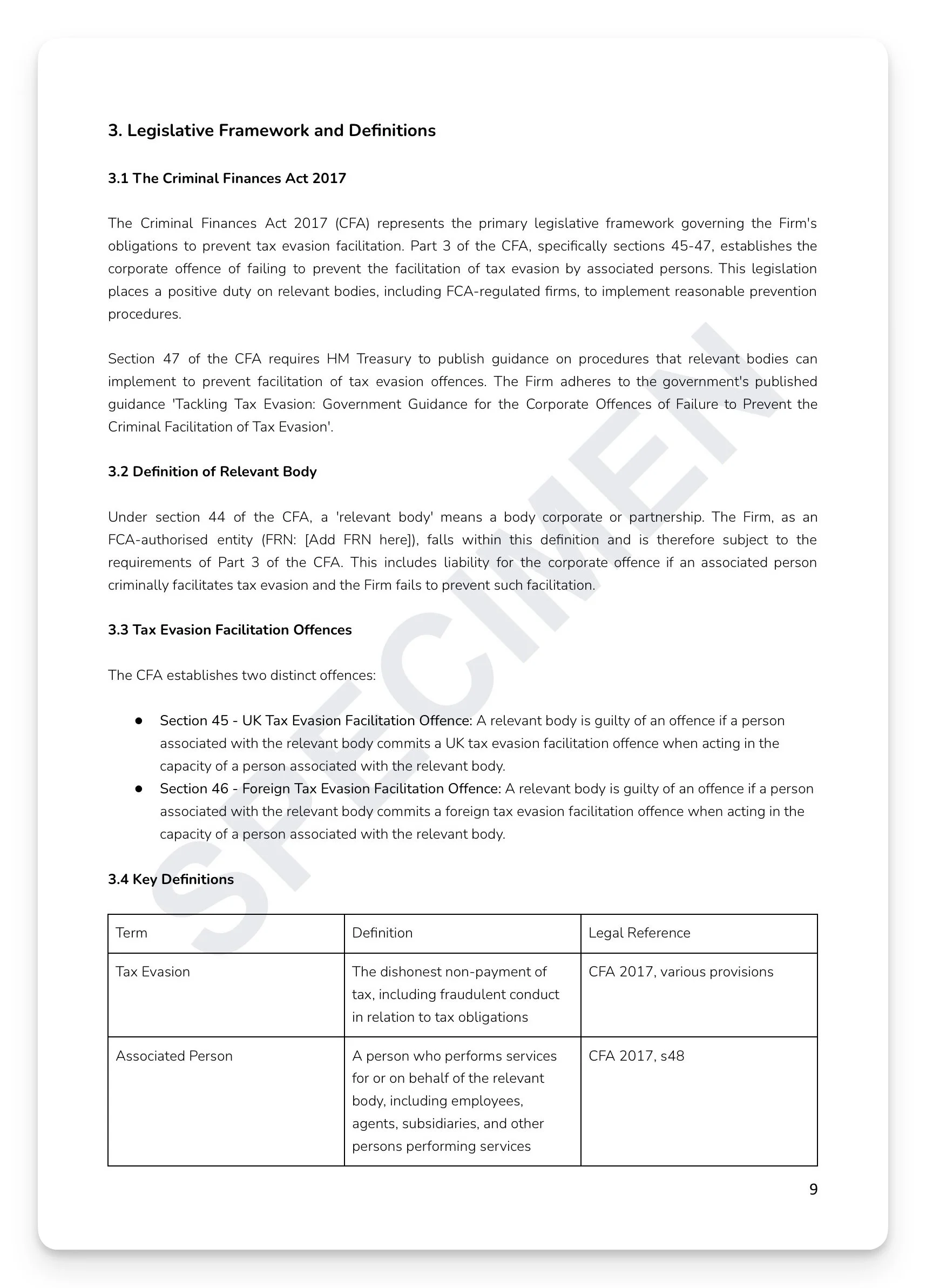

The Criminal Finances Act 2017 created two corporate criminal offences — failure to prevent the facilitation of UK and foreign tax evasion. There is no intent requirement. If anyone associated with your firm — an employee, agent, intermediary, or contractor — criminally facilitates tax evasion while acting on your behalf, your firm commits the offence. The only statutory defence is proving you had reasonable prevention procedures in place. The burden of proof is on your firm.

What's included:

Full CFA 2017 legislative framework: Sections 45 (UK facilitation), 46 (foreign facilitation), 47 (HM Treasury guidance), and 48 (associated persons definition) — with statutory defence provisions and balance of probabilities burden

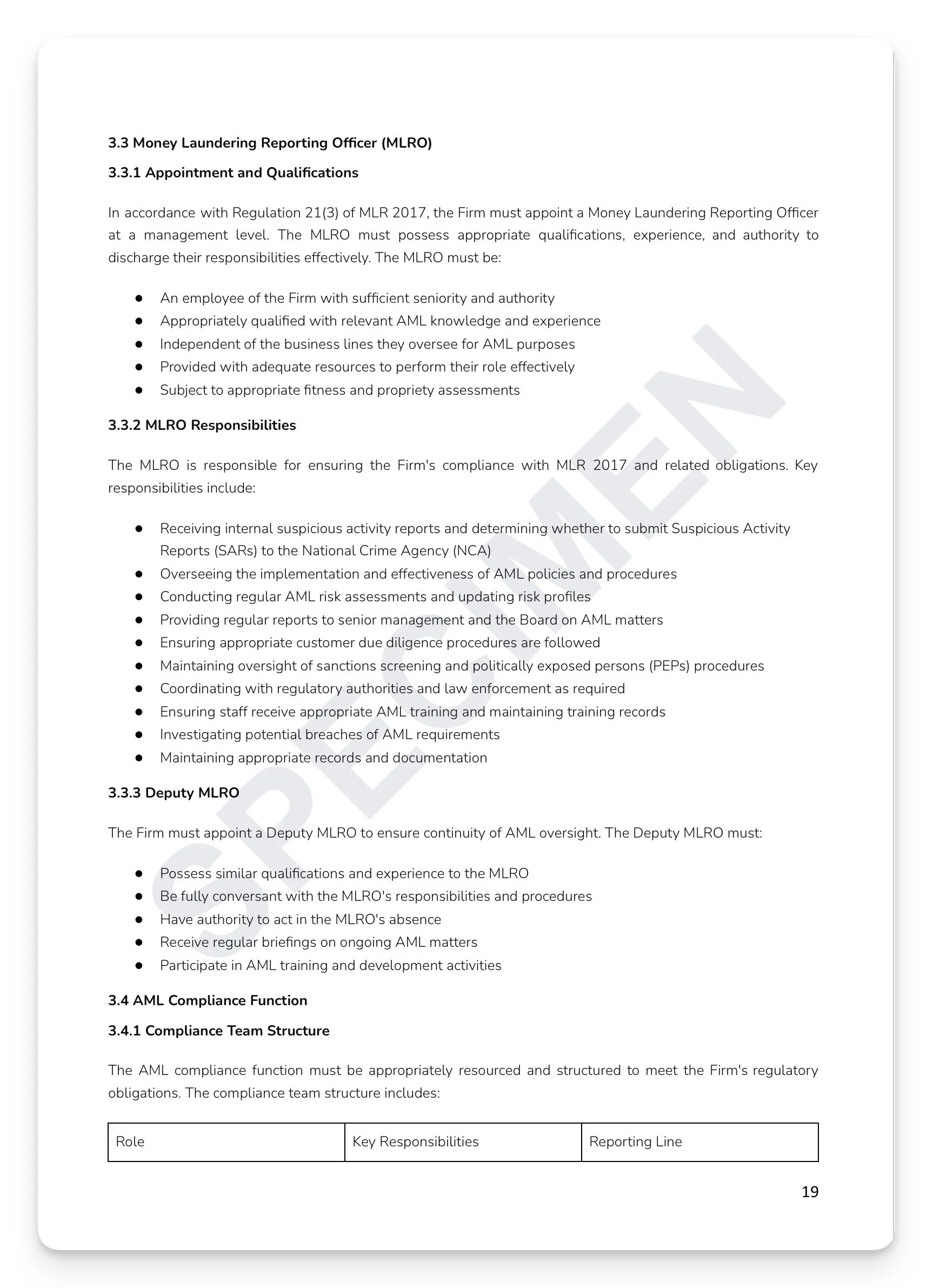

Six guiding principles framework mapped to HM Treasury guidance: risk assessment, proportionality, top-level commitment, due diligence, communication and training, and monitoring and review

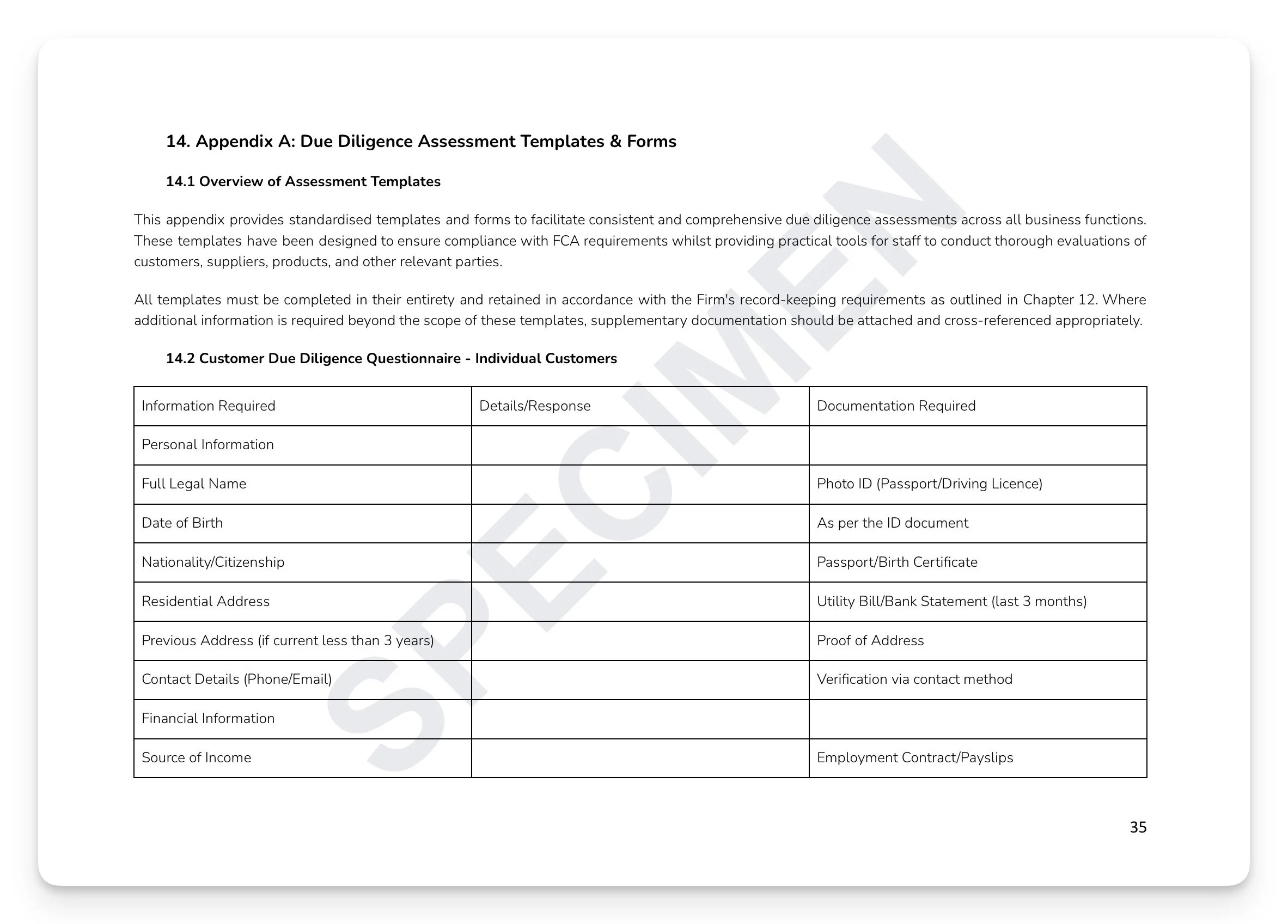

Customer CDD framework: tax residency status, tax identification numbers, source of funds, beneficial ownership thresholds by entity type — with EDD triggers for offshore structures, cash-intensive businesses, complex corporates, and PEPs

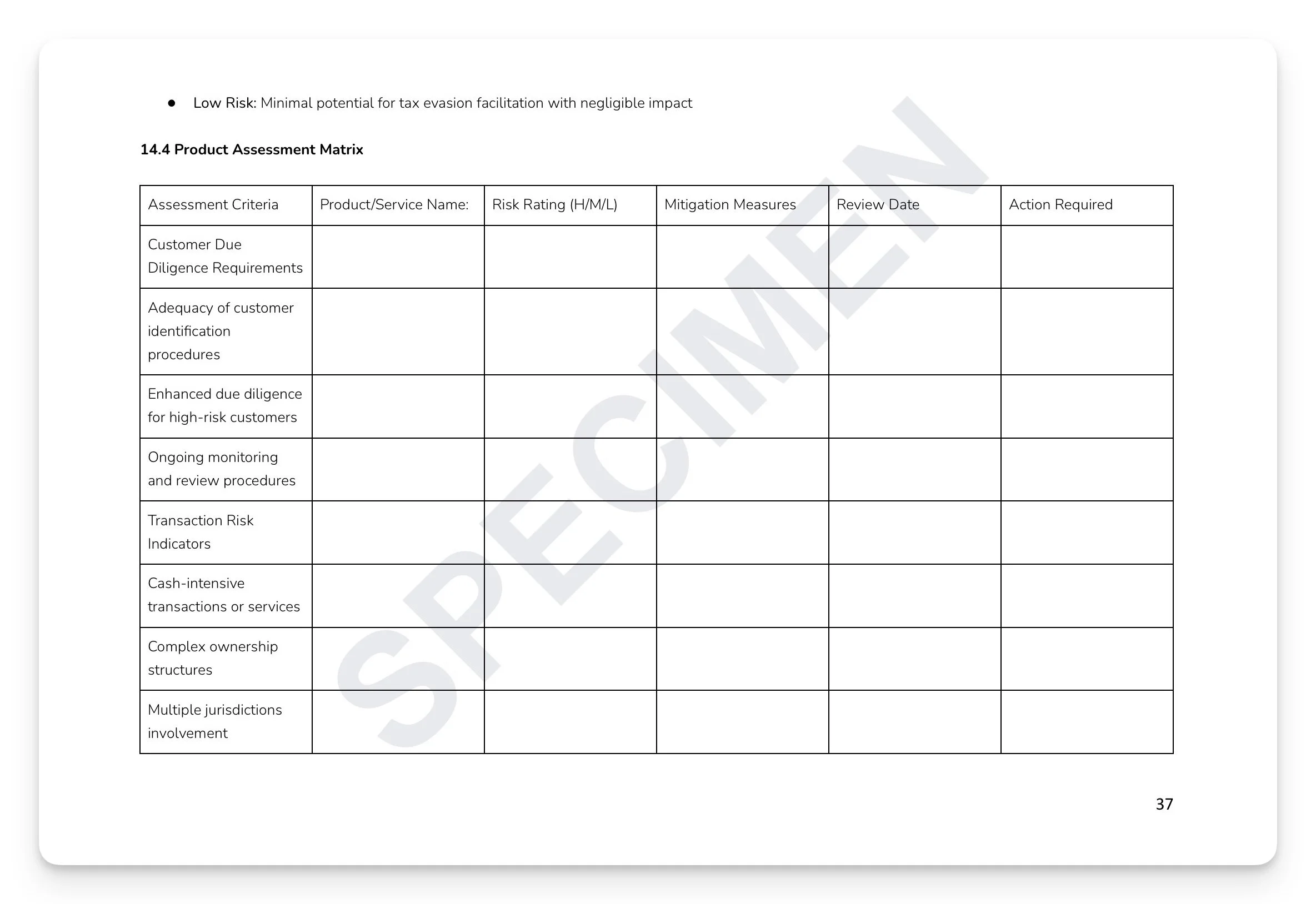

Product and service risk assessment: three-tier framework (High/Medium/Low) covering offshore jurisdictions, special purpose vehicles, anonymous transactions, and tax planning elements

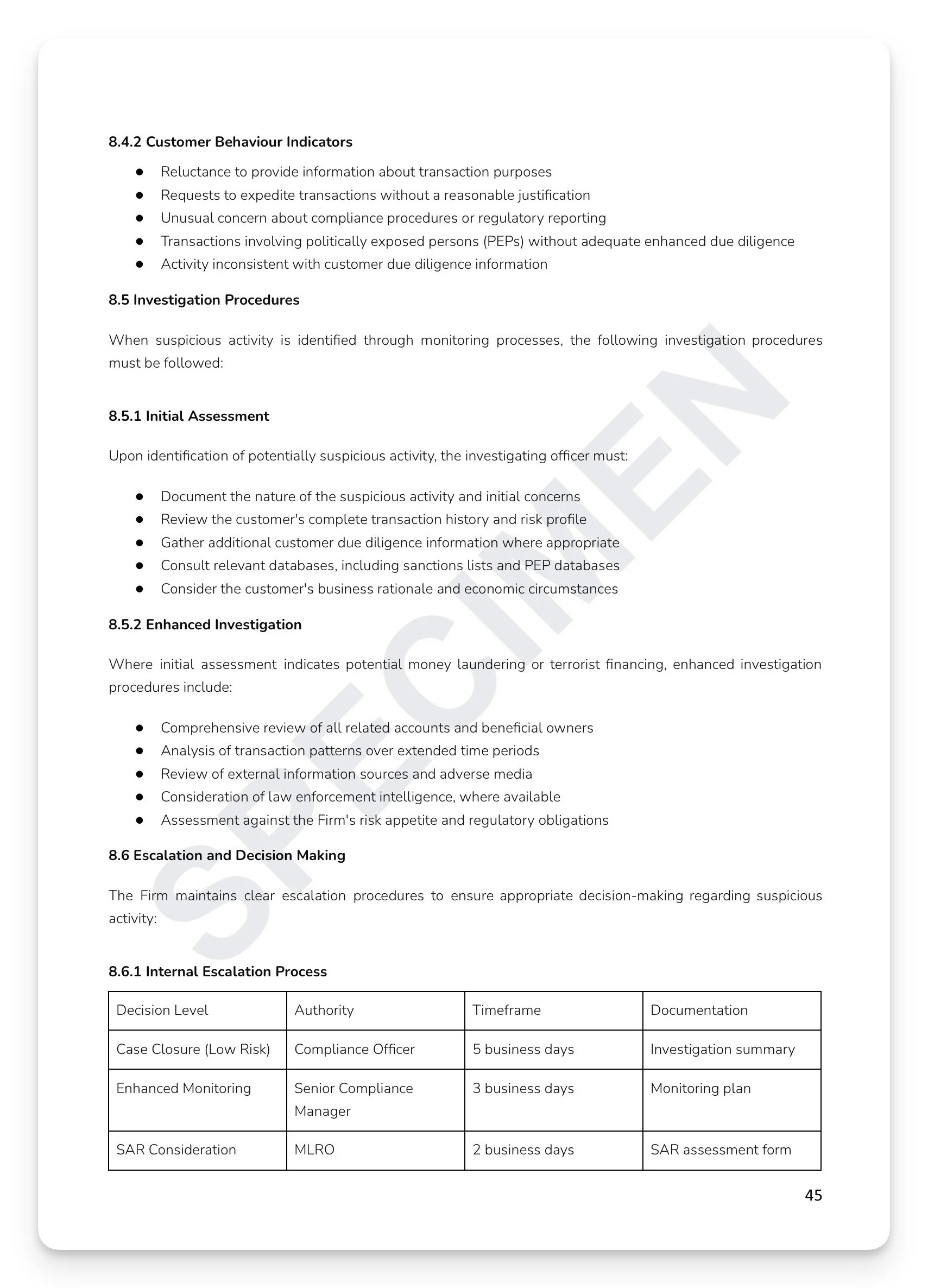

Four-category breach classification matrix: Minor, Moderate, Serious, and Critical — with escalation timeframes of 24 hours, 4 hours, 1 hour, and immediate

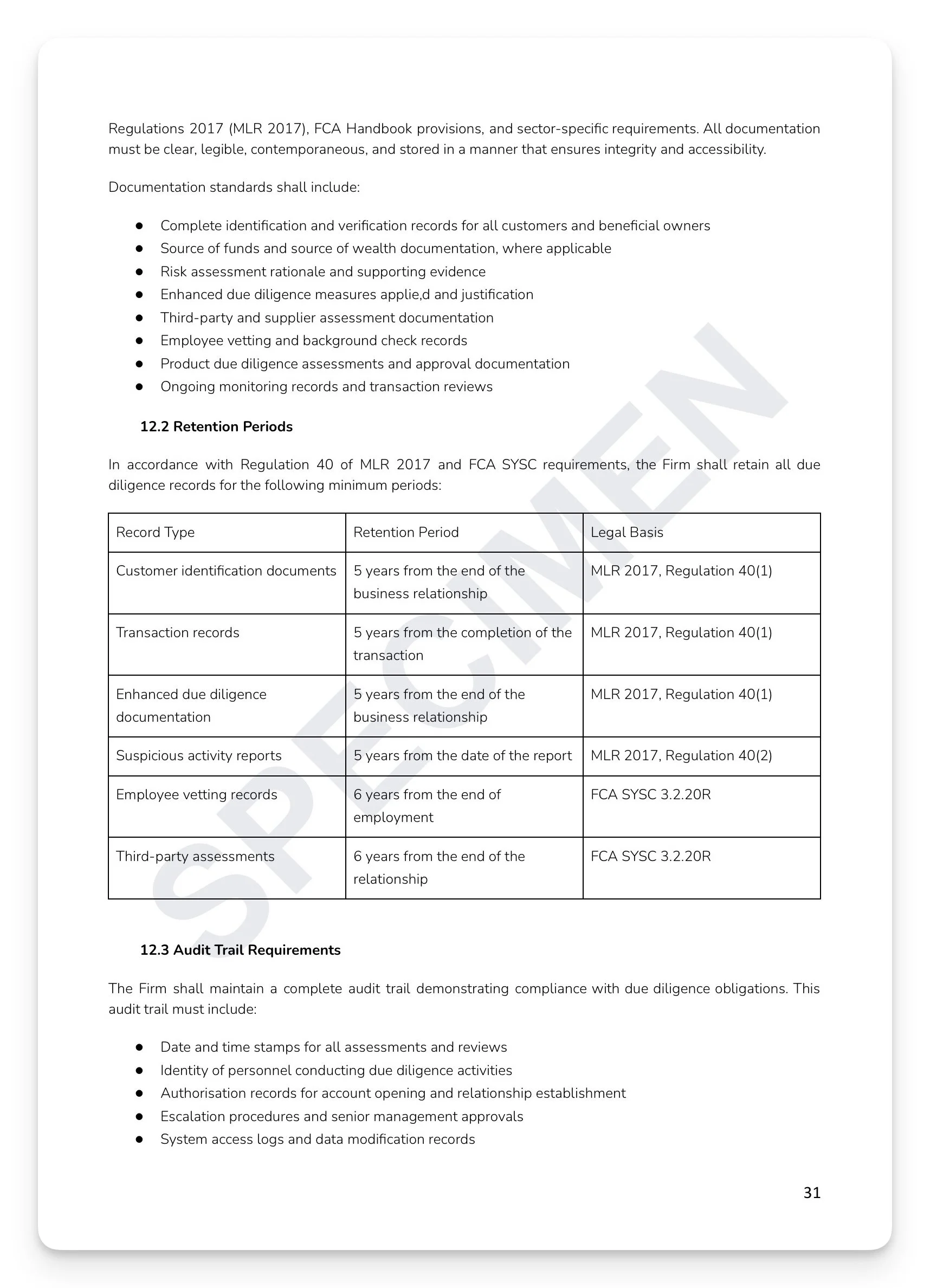

Regulatory reporting obligations: SARs to NCA, CRS reporting to HMRC by 31 May, FATCA reporting, and OFSI sanctions breach reports

Ready-to-use appendices: customer risk assessment, product and service risk assessment, third-party risk assessment, and product assessment matrix with RAG ratings across 20 risk criteria

+ much more

Who is this for?

Compliance Officers, MLROs, SMF holders, and risk functions at FCA-regulated firms who need a complete, board-approved CFA 2017-compliant Tax Evasion Prevention framework that satisfies the statutory defence requirements and withstands regulatory scrutiny.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

The Criminal Finances Act 2017 created two corporate criminal offences — failure to prevent the facilitation of UK and foreign tax evasion. There is no intent requirement. If anyone associated with your firm — an employee, agent, intermediary, or contractor — criminally facilitates tax evasion while acting on your behalf, your firm commits the offence. The only statutory defence is proving you had reasonable prevention procedures in place. The burden of proof is on your firm.

What's included:

Full CFA 2017 legislative framework: Sections 45 (UK facilitation), 46 (foreign facilitation), 47 (HM Treasury guidance), and 48 (associated persons definition) — with statutory defence provisions and balance of probabilities burden

Six guiding principles framework mapped to HM Treasury guidance: risk assessment, proportionality, top-level commitment, due diligence, communication and training, and monitoring and review

Customer CDD framework: tax residency status, tax identification numbers, source of funds, beneficial ownership thresholds by entity type — with EDD triggers for offshore structures, cash-intensive businesses, complex corporates, and PEPs

Product and service risk assessment: three-tier framework (High/Medium/Low) covering offshore jurisdictions, special purpose vehicles, anonymous transactions, and tax planning elements

Four-category breach classification matrix: Minor, Moderate, Serious, and Critical — with escalation timeframes of 24 hours, 4 hours, 1 hour, and immediate

Regulatory reporting obligations: SARs to NCA, CRS reporting to HMRC by 31 May, FATCA reporting, and OFSI sanctions breach reports

Ready-to-use appendices: customer risk assessment, product and service risk assessment, third-party risk assessment, and product assessment matrix with RAG ratings across 20 risk criteria

+ much more

Who is this for?

Compliance Officers, MLROs, SMF holders, and risk functions at FCA-regulated firms who need a complete, board-approved CFA 2017-compliant Tax Evasion Prevention framework that satisfies the statutory defence requirements and withstands regulatory scrutiny.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 15

Image 1 of 15

Image 2 of 15

Image 2 of 15

Image 3 of 15

Image 3 of 15

Image 4 of 15

Image 4 of 15

Image 5 of 15

Image 5 of 15

Image 6 of 15

Image 6 of 15

Image 7 of 15

Image 7 of 15

Image 8 of 15

Image 8 of 15