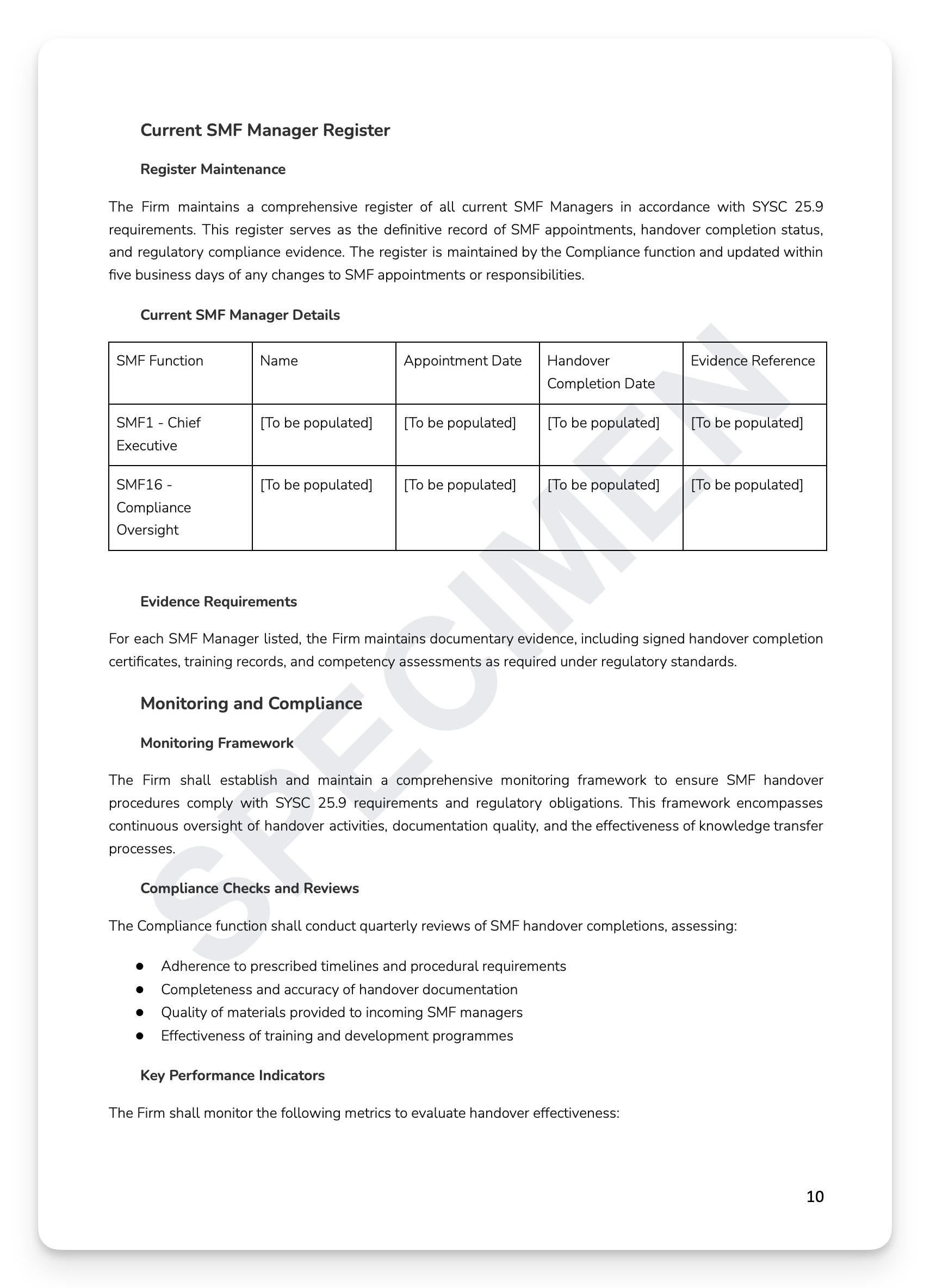

The FCA's Conduct Rules aren't aspirational guidelines — they're enforceable personal standards that apply to virtually every employee in a regulated firm, with the FCA empowered to investigate, sanction, and prohibit individuals who fall short. A two-tier framework places Individual Conduct Rules on all staff and additional Senior Manager Rules on SMF holders, creating layered personal accountability that most firms underestimate until it's tested. The FCA doesn't wait.

What's included:

Full two-tier Conduct Rules framework: Individual Rules 1–6 (all staff) and Senior Manager Rules SC1–SC4 (SMF holders) — with plain-English explanations, compliance examples, and real-world breach scenarios

Role classification framework: Senior Managers, client-facing roles, and support functions — with specific obligations for each

Induction training requirements: timelines, CPD obligations, and ongoing competency standards

Monitoring framework: day-to-day oversight, escalation triggers, and investigation procedures

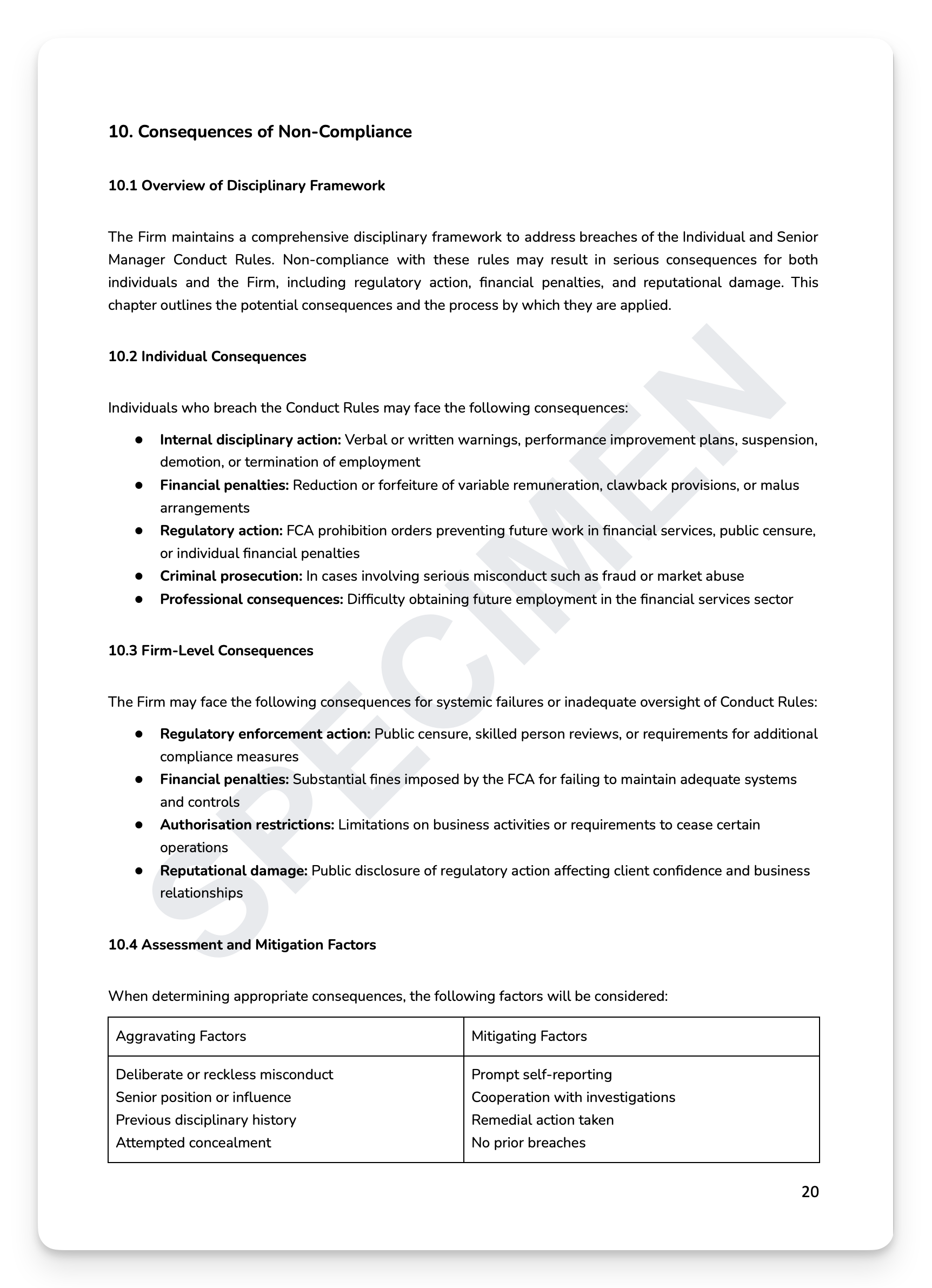

Breach reporting and escalation: FCA notification obligations and consequences framework — individual sanctions, firm-level consequences, and mitigation factors

Recruitment and fitness assessment: FIT criteria, pre-employment screening, and ongoing reassessment

Record-keeping requirements: training records, competency assessments, and breach investigation files

+ much more

Who is this for?

SMF16 holders, Compliance Officers, HR Directors, and Line Managers at FCA-regulated firms who need a documented, board-approved Conduct Rules Policy that protects individuals and the firm alike.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

The FCA's Conduct Rules aren't aspirational guidelines — they're enforceable personal standards that apply to virtually every employee in a regulated firm, with the FCA empowered to investigate, sanction, and prohibit individuals who fall short. A two-tier framework places Individual Conduct Rules on all staff and additional Senior Manager Rules on SMF holders, creating layered personal accountability that most firms underestimate until it's tested. The FCA doesn't wait.

What's included:

Full two-tier Conduct Rules framework: Individual Rules 1–6 (all staff) and Senior Manager Rules SC1–SC4 (SMF holders) — with plain-English explanations, compliance examples, and real-world breach scenarios

Role classification framework: Senior Managers, client-facing roles, and support functions — with specific obligations for each

Induction training requirements: timelines, CPD obligations, and ongoing competency standards

Monitoring framework: day-to-day oversight, escalation triggers, and investigation procedures

Breach reporting and escalation: FCA notification obligations and consequences framework — individual sanctions, firm-level consequences, and mitigation factors

Recruitment and fitness assessment: FIT criteria, pre-employment screening, and ongoing reassessment

Record-keeping requirements: training records, competency assessments, and breach investigation files

+ much more

Who is this for?

SMF16 holders, Compliance Officers, HR Directors, and Line Managers at FCA-regulated firms who need a documented, board-approved Conduct Rules Policy that protects individuals and the firm alike.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7