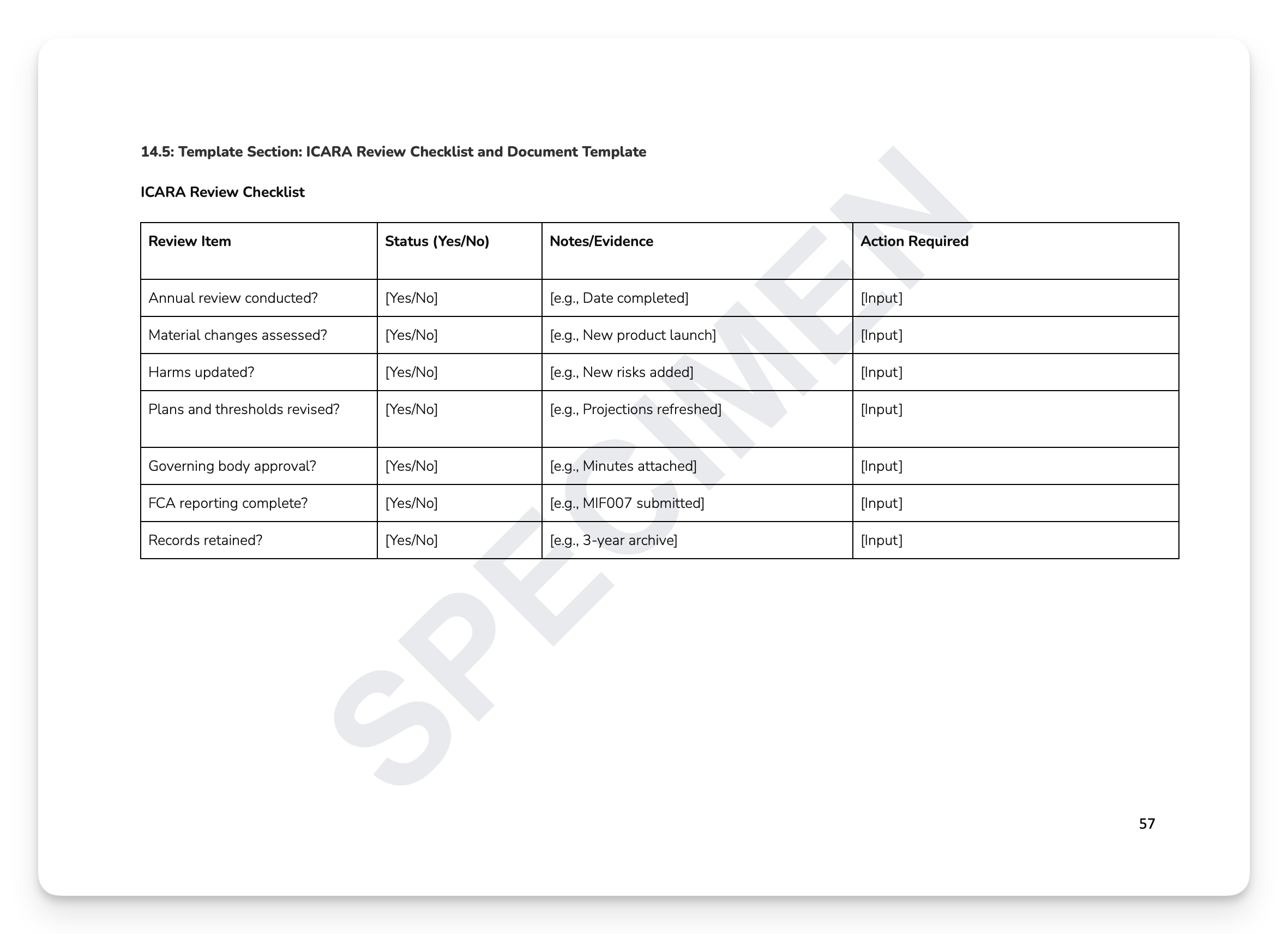

The Internal Capital and Risk Assessment process is the cornerstone of the MIFIDPRU prudential regime — replacing the old ICAAP/ILAAP framework and requiring firms to identify every potential harm to clients, markets, and themselves, then demonstrate they hold sufficient capital and liquid assets to cover it. Getting this wrong doesn't just mean a deficient document — it triggers FCA supervisory intervention, additional capital requirements, and personal accountability for senior managers. The FCA doesn't wait.

What's included:

Full regulatory mapping: MIFIDPRU 7.1–7.10, MIFIDPRU Annexes 1–7, and MIF007 submission requirements

Firm classification calculator: SNI vs non-SNI thresholds, K-factors, currency conversion guidance, and group vs individual application

Harm Register: structured matrix covering harms to clients, markets, and the firm — with likelihood, impact, and mitigation columns

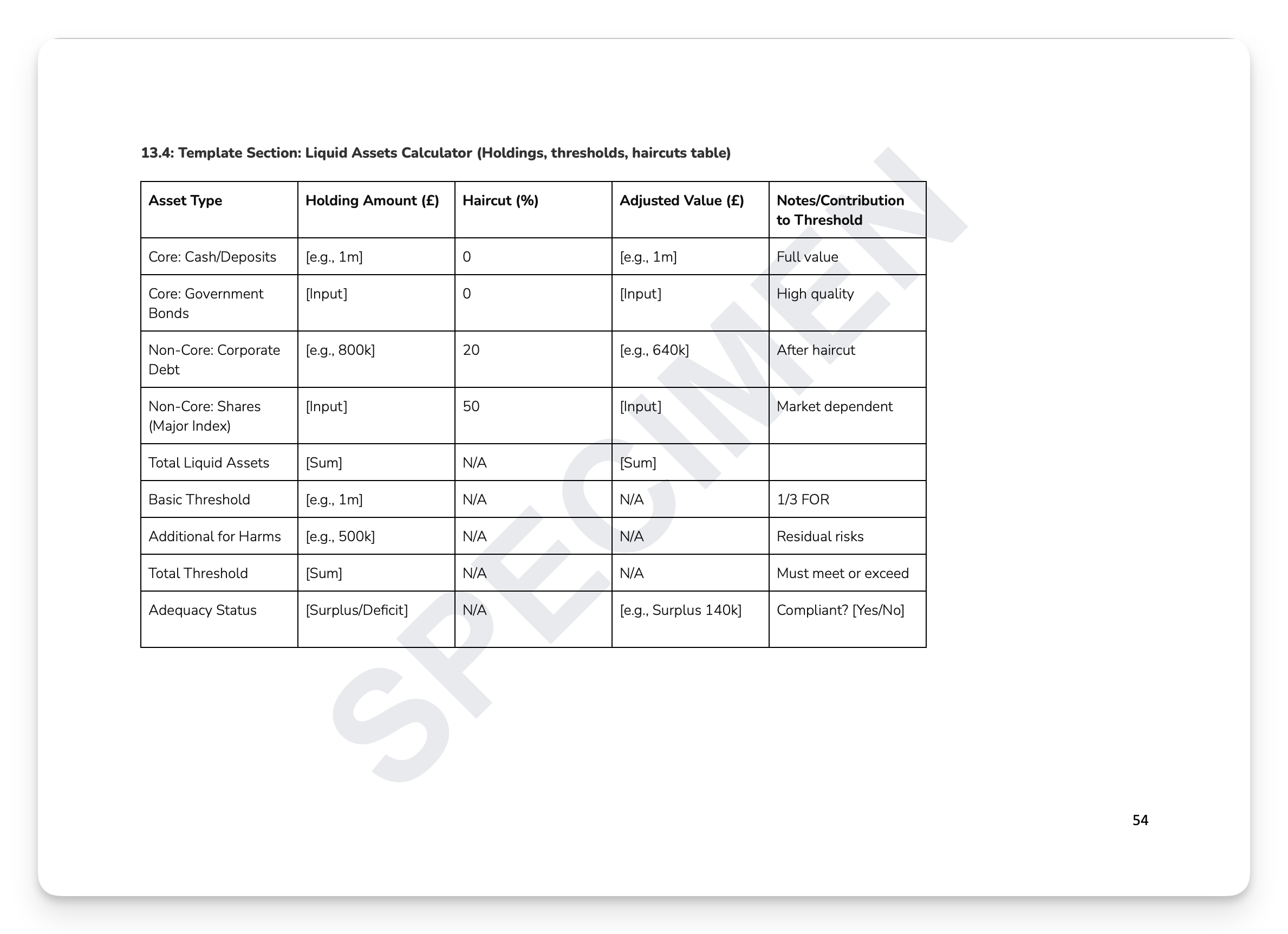

Capital and liquidity planning templates: 3-year financial projections, own funds calculator, and liquid assets calculator with haircuts table

Stress testing workbook: forward-looking scenarios, reverse stress testing, and economic and operational failure scenarios

Wind-down plan template: triggers, timelines, resource requirements, and consistency checks against ICARA thresholds

SREP readiness checklist: what the FCA reviews, common intervention triggers, and documentation tips

+ much more

Who is this for?

CFOs, Risk Directors, Compliance Officers, and Governing Bodies at FCA-regulated investment firms — SNI and non-SNI — who need a complete, board-approved ICARA that satisfies MIFIDPRU 7 requirements and can withstand supervisory scrutiny.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

The Internal Capital and Risk Assessment process is the cornerstone of the MIFIDPRU prudential regime — replacing the old ICAAP/ILAAP framework and requiring firms to identify every potential harm to clients, markets, and themselves, then demonstrate they hold sufficient capital and liquid assets to cover it. Getting this wrong doesn't just mean a deficient document — it triggers FCA supervisory intervention, additional capital requirements, and personal accountability for senior managers. The FCA doesn't wait.

What's included:

Full regulatory mapping: MIFIDPRU 7.1–7.10, MIFIDPRU Annexes 1–7, and MIF007 submission requirements

Firm classification calculator: SNI vs non-SNI thresholds, K-factors, currency conversion guidance, and group vs individual application

Harm Register: structured matrix covering harms to clients, markets, and the firm — with likelihood, impact, and mitigation columns

Capital and liquidity planning templates: 3-year financial projections, own funds calculator, and liquid assets calculator with haircuts table

Stress testing workbook: forward-looking scenarios, reverse stress testing, and economic and operational failure scenarios

Wind-down plan template: triggers, timelines, resource requirements, and consistency checks against ICARA thresholds

SREP readiness checklist: what the FCA reviews, common intervention triggers, and documentation tips

+ much more

Who is this for?

CFOs, Risk Directors, Compliance Officers, and Governing Bodies at FCA-regulated investment firms — SNI and non-SNI — who need a complete, board-approved ICARA that satisfies MIFIDPRU 7 requirements and can withstand supervisory scrutiny.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 11

Image 1 of 11

Image 2 of 11

Image 2 of 11

Image 3 of 11

Image 3 of 11

Image 4 of 11

Image 4 of 11

Image 5 of 11

Image 5 of 11

Image 6 of 11

Image 6 of 11

Image 7 of 11

Image 7 of 11

Image 8 of 11

Image 8 of 11

Image 9 of 11

Image 9 of 11

Image 10 of 11

Image 10 of 11

Image 11 of 11

Image 11 of 11