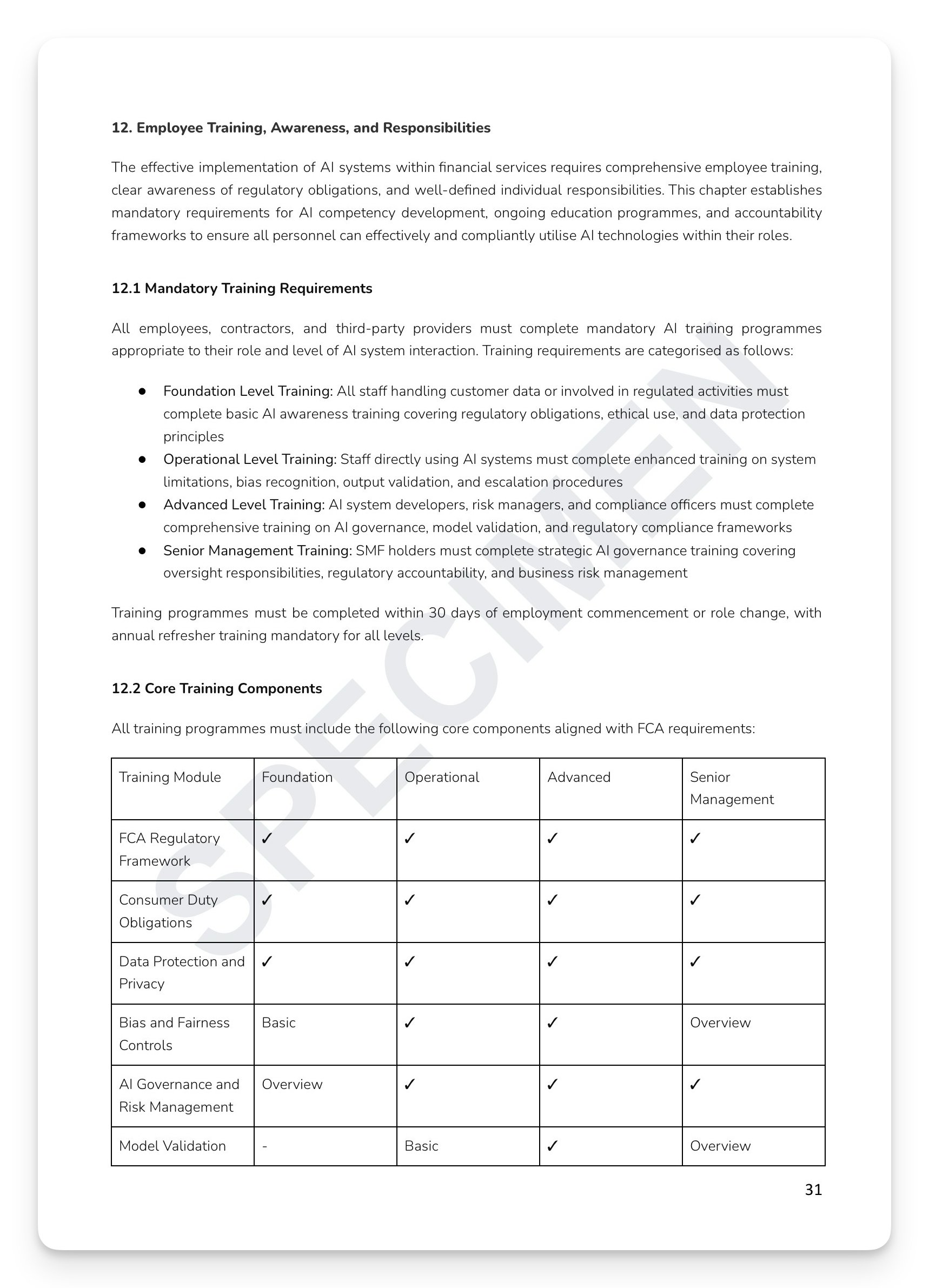

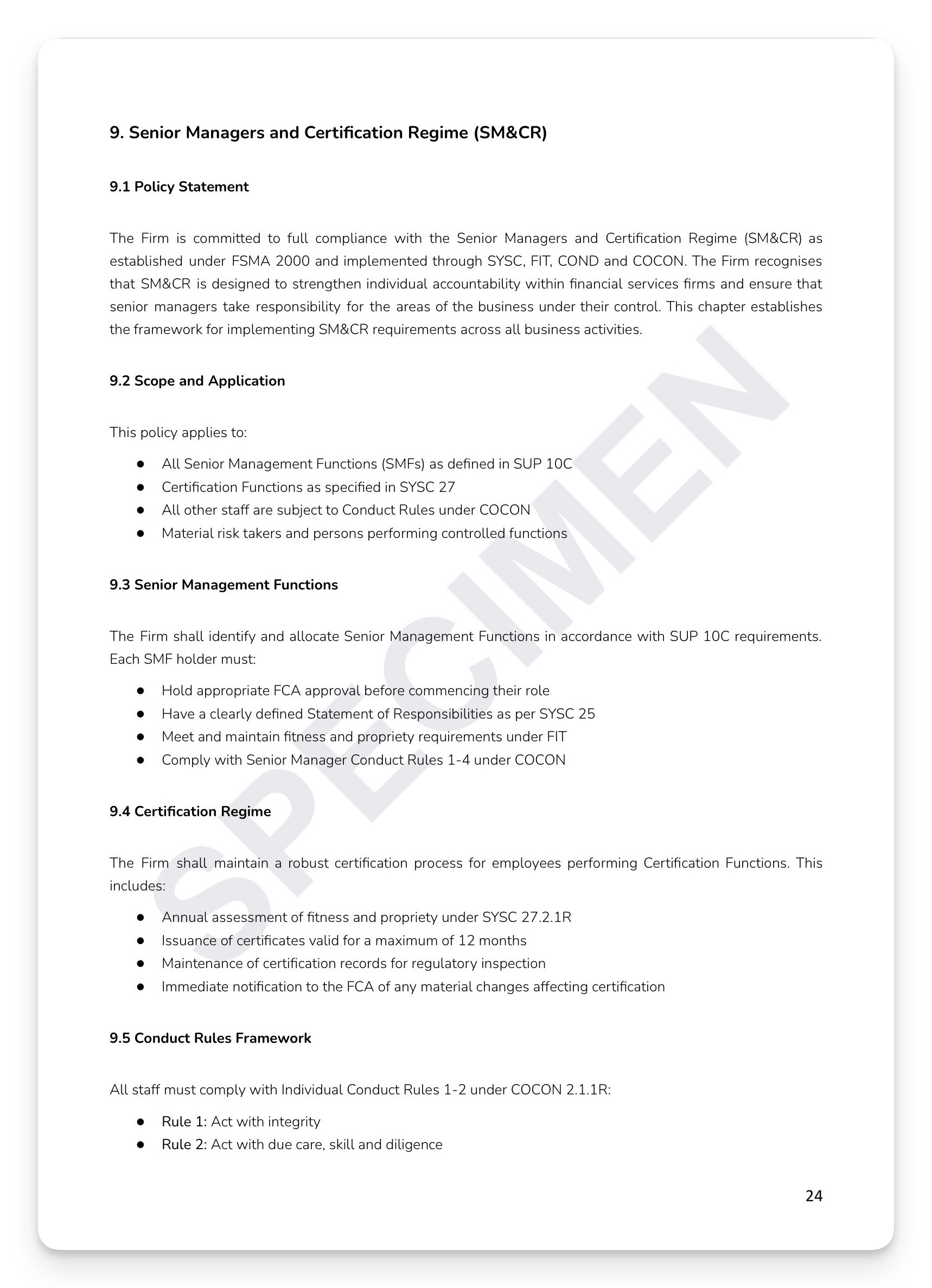

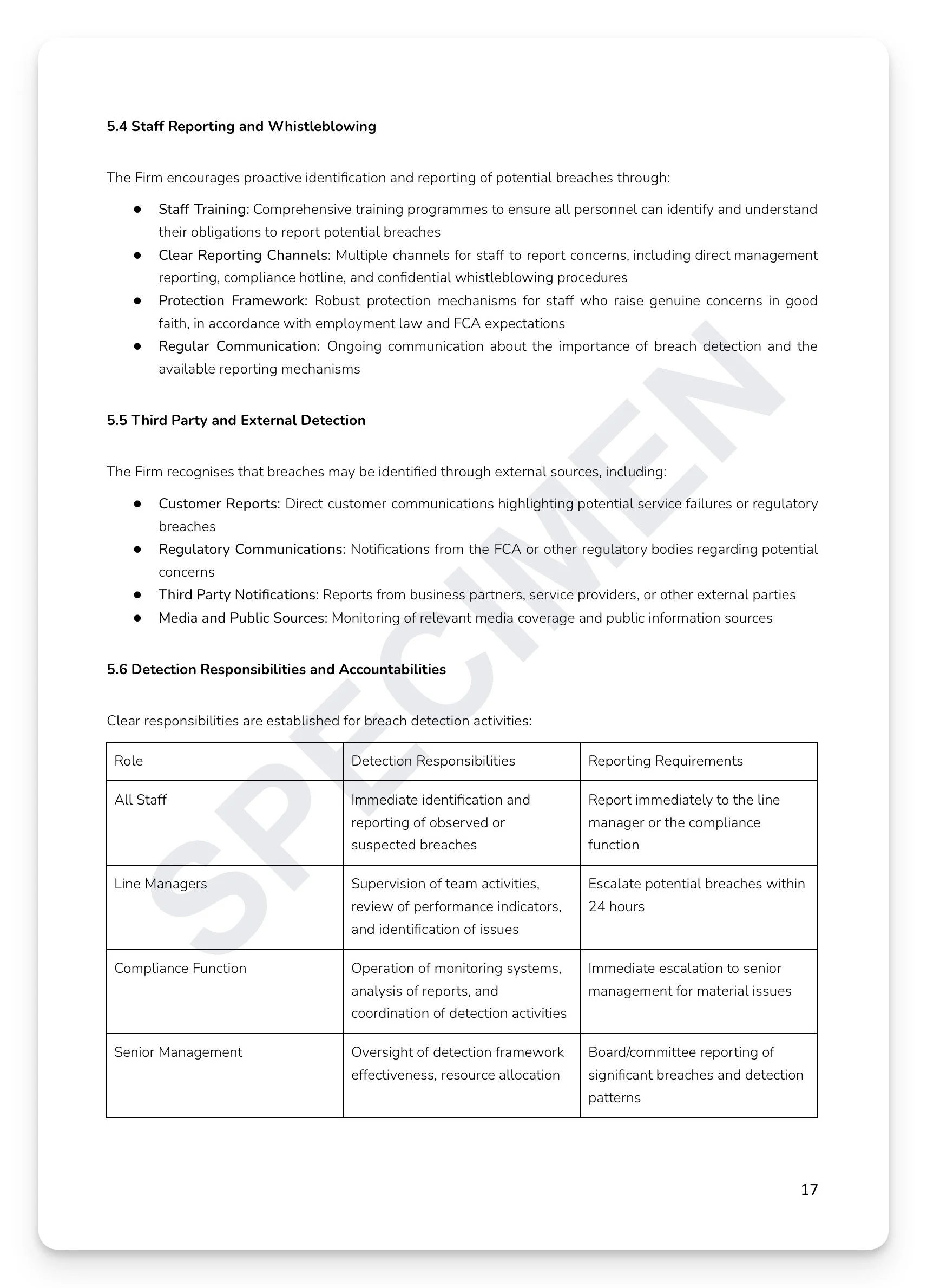

Every FCA-regulated firm has compliance breaches. The ones that face enforcement tend to be the ones that didn't have a framework for managing them. Under SYSC 6.1.1R, every FCA-authorised firm must maintain effective compliance arrangements to identify and manage regulatory failures. When something goes wrong, the question the regulator asks isn't just what happened — it's whether the firm detected it, reported it correctly, investigated it thoroughly, remediated it properly, and prevented it from recurring. The FCA doesn't punish firms for having breaches. It punishes firms for not knowing how to handle them.

What's included:

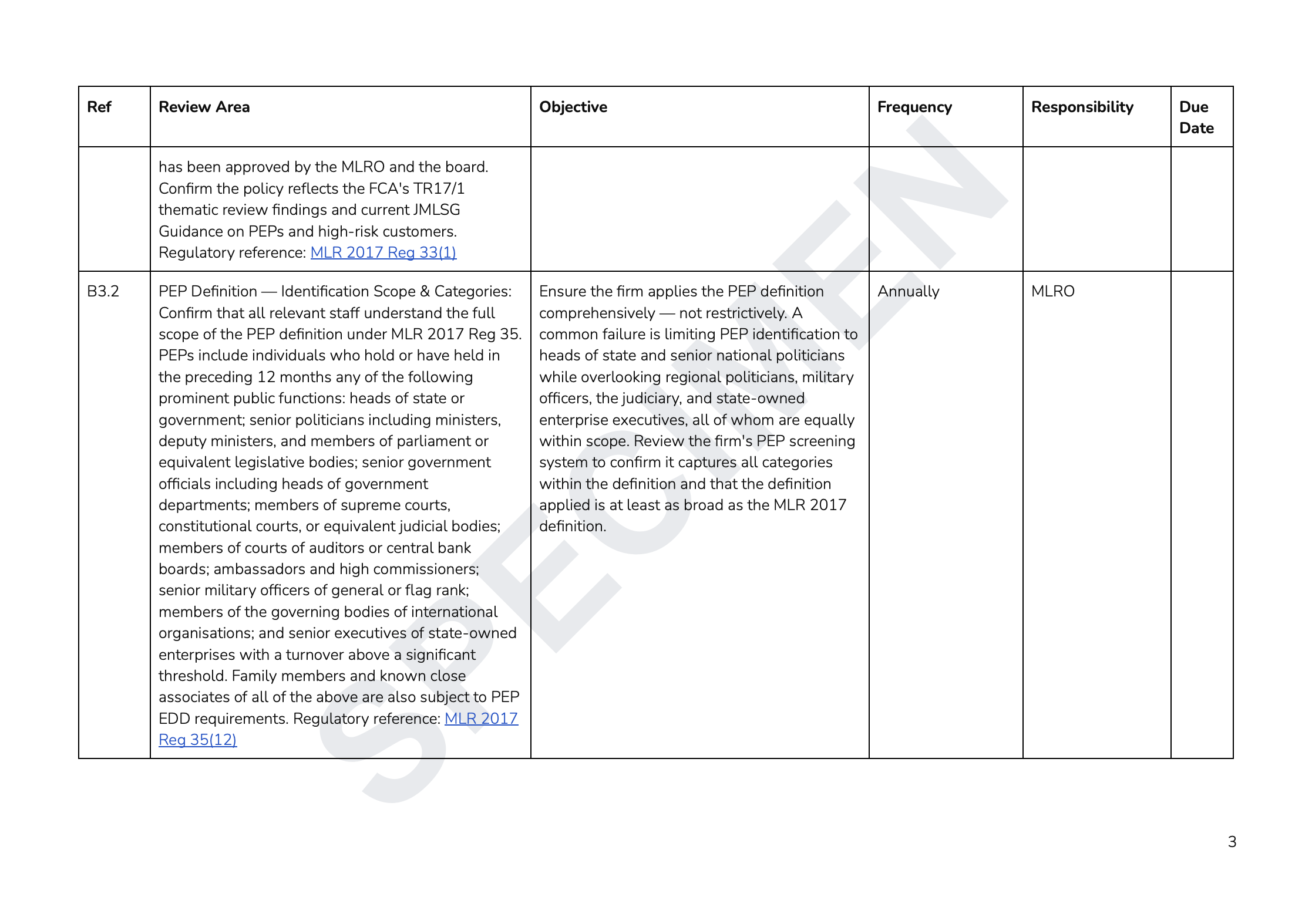

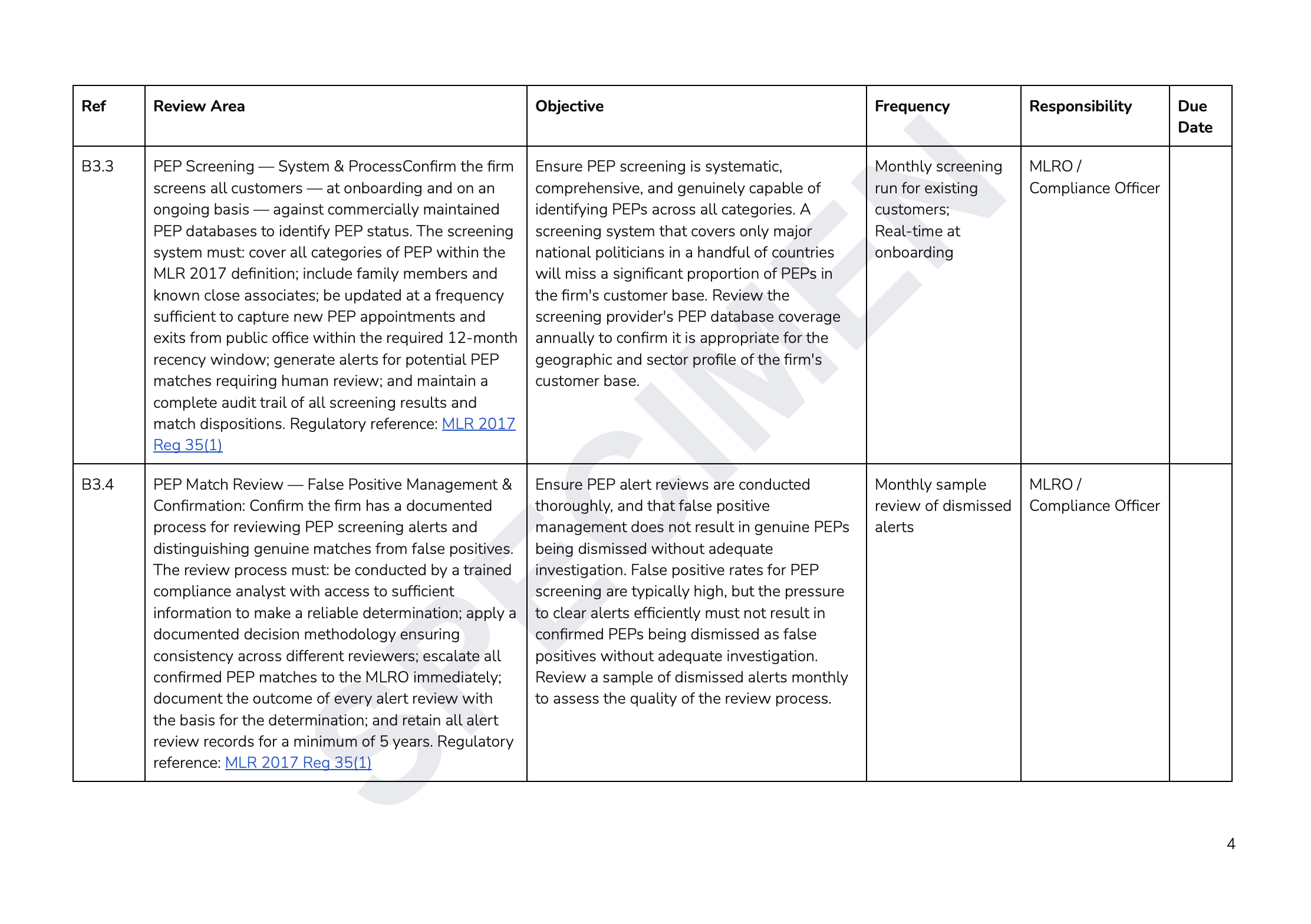

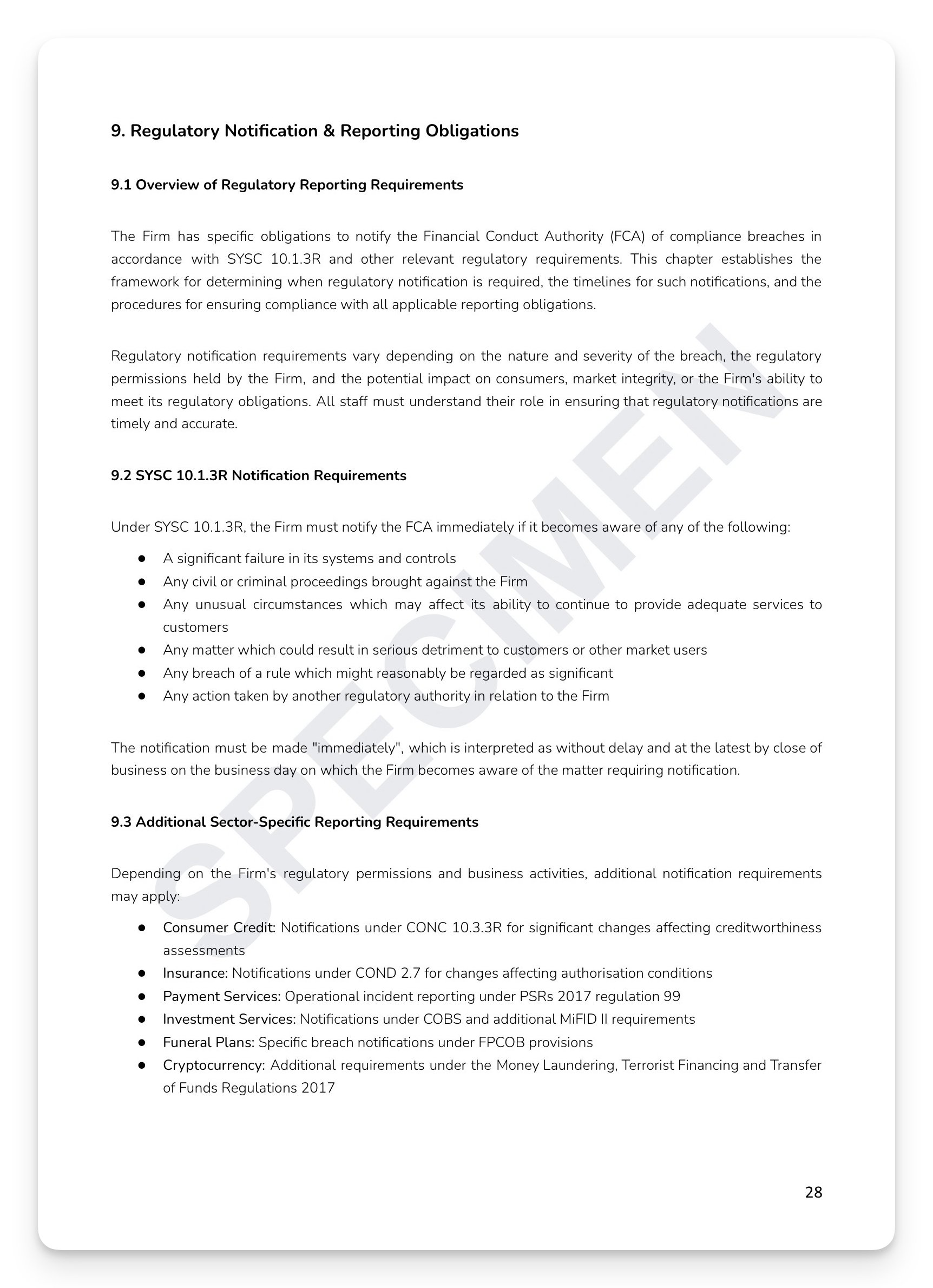

Full regulatory mapping: SYSC 3.1.1R/4.1.1R/6.1.1R/9.1.1R/10.1.3R, SUP 15.3.1R/15.3.8R/15.11, PRIN 3/6/11, SM&CR SYSC 24/26/27, COCON 2.1.1R, UK GDPR/DPA 2018, and the ICO 72-hour obligation

Five breach categories: Conduct/Customer Treatment, Financial Crime/AML, Prudential/Capital, Governance/Systems, and Market Conduct/Integrity — with sector-specific examples across Consumer Credit, Insurance, Investment, Payment Services, and Cryptoassets

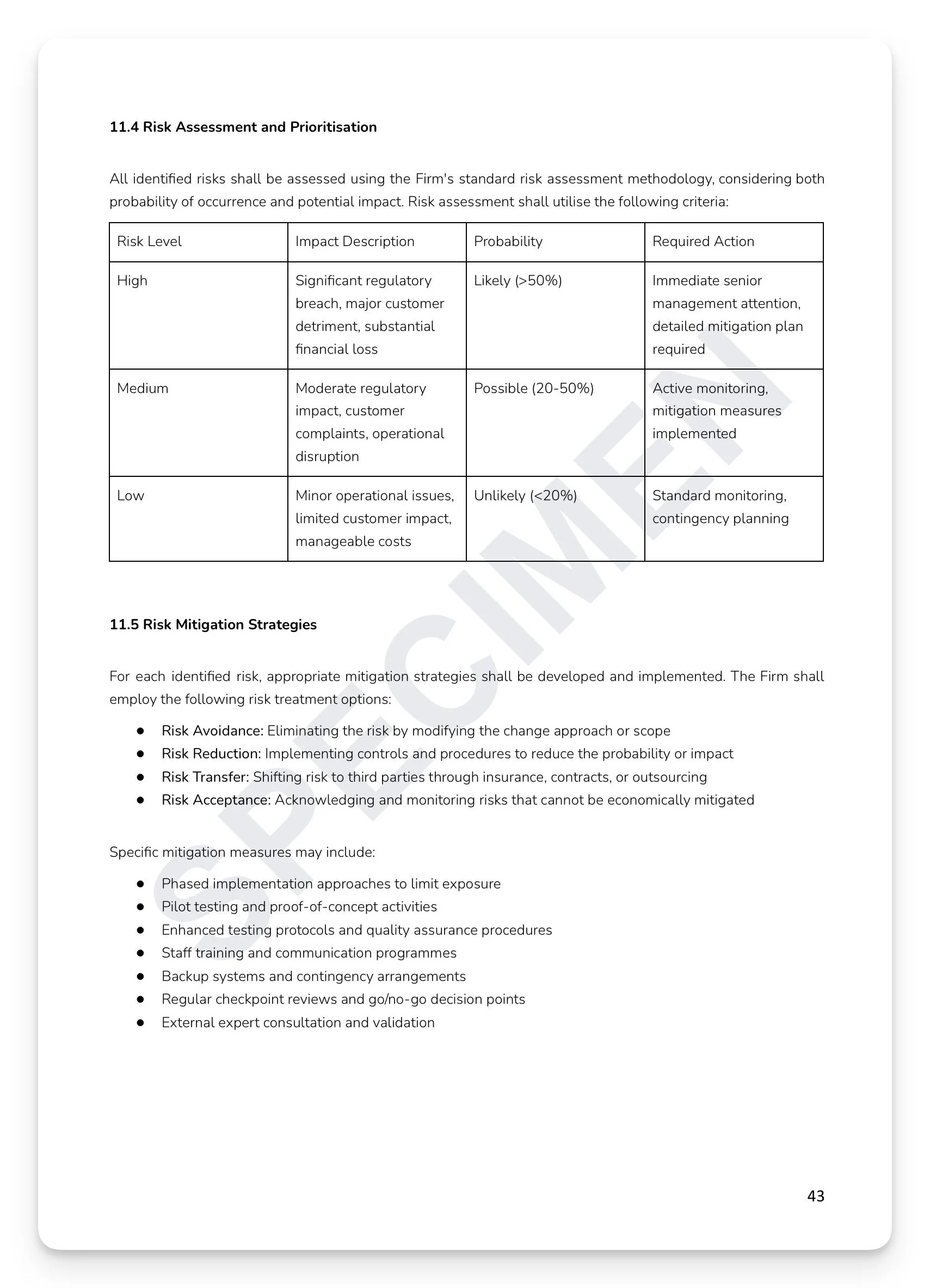

Four-tier severity classification: Critical (>£50,000 customer detriment), High (£10,000–£50,000), Medium (<£10,000), and Low (administrative) — with five-factor assessment matrix

Mandatory 2-hour verbal notification and 24-hour written report standard — with four-level escalation matrix from Line Manager through to Board Emergency Meeting

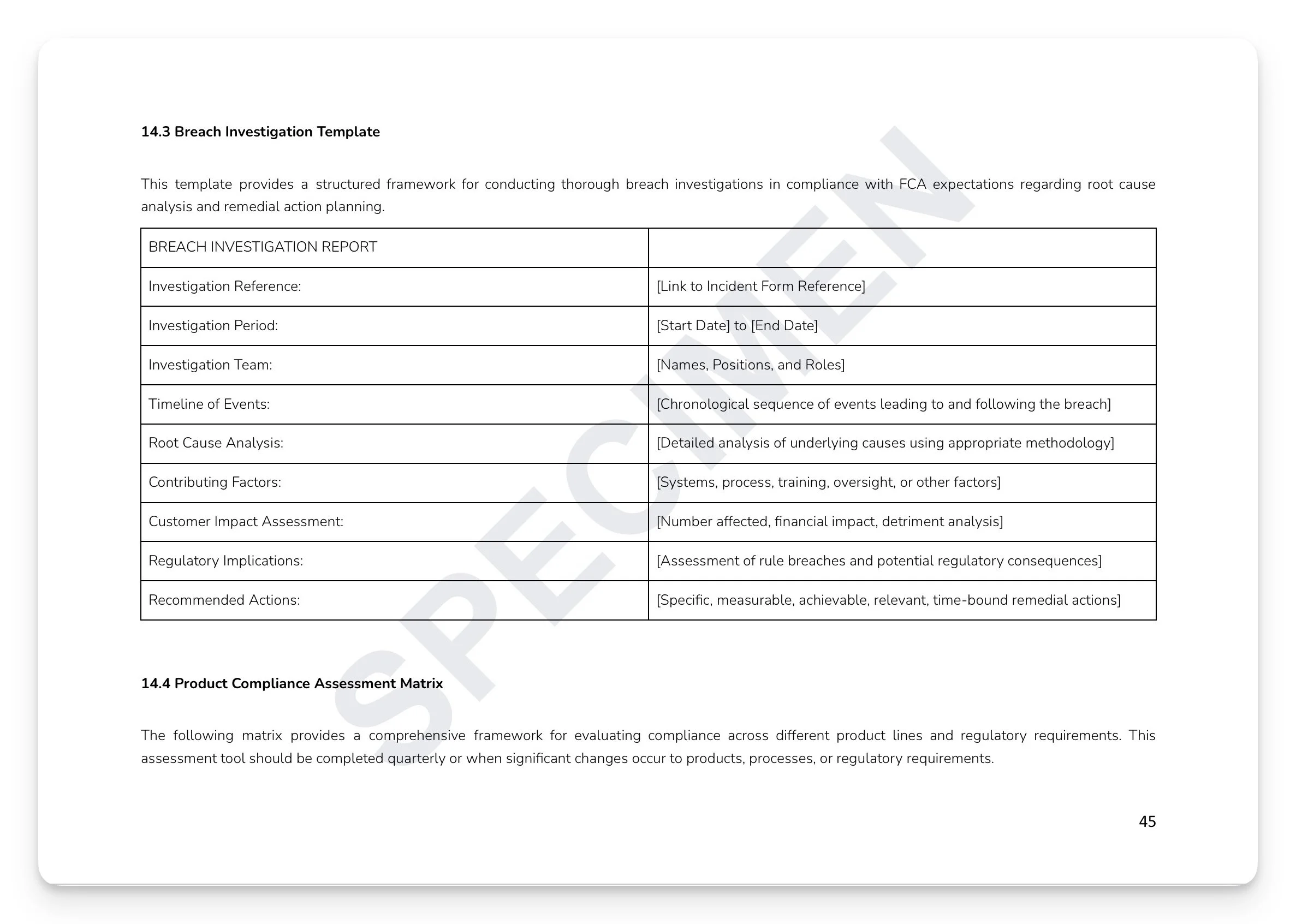

Three-phase investigation methodology: information gathering, analysis and assessment, and root cause analysis — with evidence chain of custody requirements and independence obligations

Customer remediation framework: identification, impact assessment, redress calculation, communication strategy, and payment processing

Ready-to-use appendices: Compliance Breach Incident Form with classification checkboxes, Breach Investigation Report Template, and Product Compliance Assessment Matrix across six regulatory regimes

+ much more

Who is this for?

Compliance Officers, SMF16/17 holders, Risk Managers, and Boards at FCA-regulated firms who need a complete, board-approved Compliance Breach Policy that satisfies regulatory supervisory expectations and gives the firm documented evidence of a functioning breach management culture.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Every FCA-regulated firm has compliance breaches. The ones that face enforcement tend to be the ones that didn't have a framework for managing them. Under SYSC 6.1.1R, every FCA-authorised firm must maintain effective compliance arrangements to identify and manage regulatory failures. When something goes wrong, the question the regulator asks isn't just what happened — it's whether the firm detected it, reported it correctly, investigated it thoroughly, remediated it properly, and prevented it from recurring. The FCA doesn't punish firms for having breaches. It punishes firms for not knowing how to handle them.

What's included:

Full regulatory mapping: SYSC 3.1.1R/4.1.1R/6.1.1R/9.1.1R/10.1.3R, SUP 15.3.1R/15.3.8R/15.11, PRIN 3/6/11, SM&CR SYSC 24/26/27, COCON 2.1.1R, UK GDPR/DPA 2018, and the ICO 72-hour obligation

Five breach categories: Conduct/Customer Treatment, Financial Crime/AML, Prudential/Capital, Governance/Systems, and Market Conduct/Integrity — with sector-specific examples across Consumer Credit, Insurance, Investment, Payment Services, and Cryptoassets

Four-tier severity classification: Critical (>£50,000 customer detriment), High (£10,000–£50,000), Medium (<£10,000), and Low (administrative) — with five-factor assessment matrix

Mandatory 2-hour verbal notification and 24-hour written report standard — with four-level escalation matrix from Line Manager through to Board Emergency Meeting

Three-phase investigation methodology: information gathering, analysis and assessment, and root cause analysis — with evidence chain of custody requirements and independence obligations

Customer remediation framework: identification, impact assessment, redress calculation, communication strategy, and payment processing

Ready-to-use appendices: Compliance Breach Incident Form with classification checkboxes, Breach Investigation Report Template, and Product Compliance Assessment Matrix across six regulatory regimes

+ much more

Who is this for?

Compliance Officers, SMF16/17 holders, Risk Managers, and Boards at FCA-regulated firms who need a complete, board-approved Compliance Breach Policy that satisfies regulatory supervisory expectations and gives the firm documented evidence of a functioning breach management culture.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 10

Image 1 of 10

Image 2 of 10

Image 2 of 10

Image 3 of 10

Image 3 of 10

Image 4 of 10

Image 4 of 10

Image 5 of 10

Image 5 of 10

Image 6 of 10

Image 6 of 10

Image 7 of 10

Image 7 of 10

Image 8 of 10

Image 8 of 10

Image 9 of 10

Image 9 of 10

Image 10 of 10

Image 10 of 10