Fraud costs UK financial services billions every year — and most firms' policies don't cover half of how it happens. The Fraud Act 2006 creates three distinct criminal offences, and your firm can face corporate liability for fraud committed by anyone acting on your behalf. Beyond the criminal exposure, the FCA treats fraud prevention as a core regulatory obligation under SYSC, PRIN, and Consumer Duty. Internal fraud, external fraud, financial crime integration, regulatory governance — most firms have fragments of a framework. Few have the full picture.

What's included:

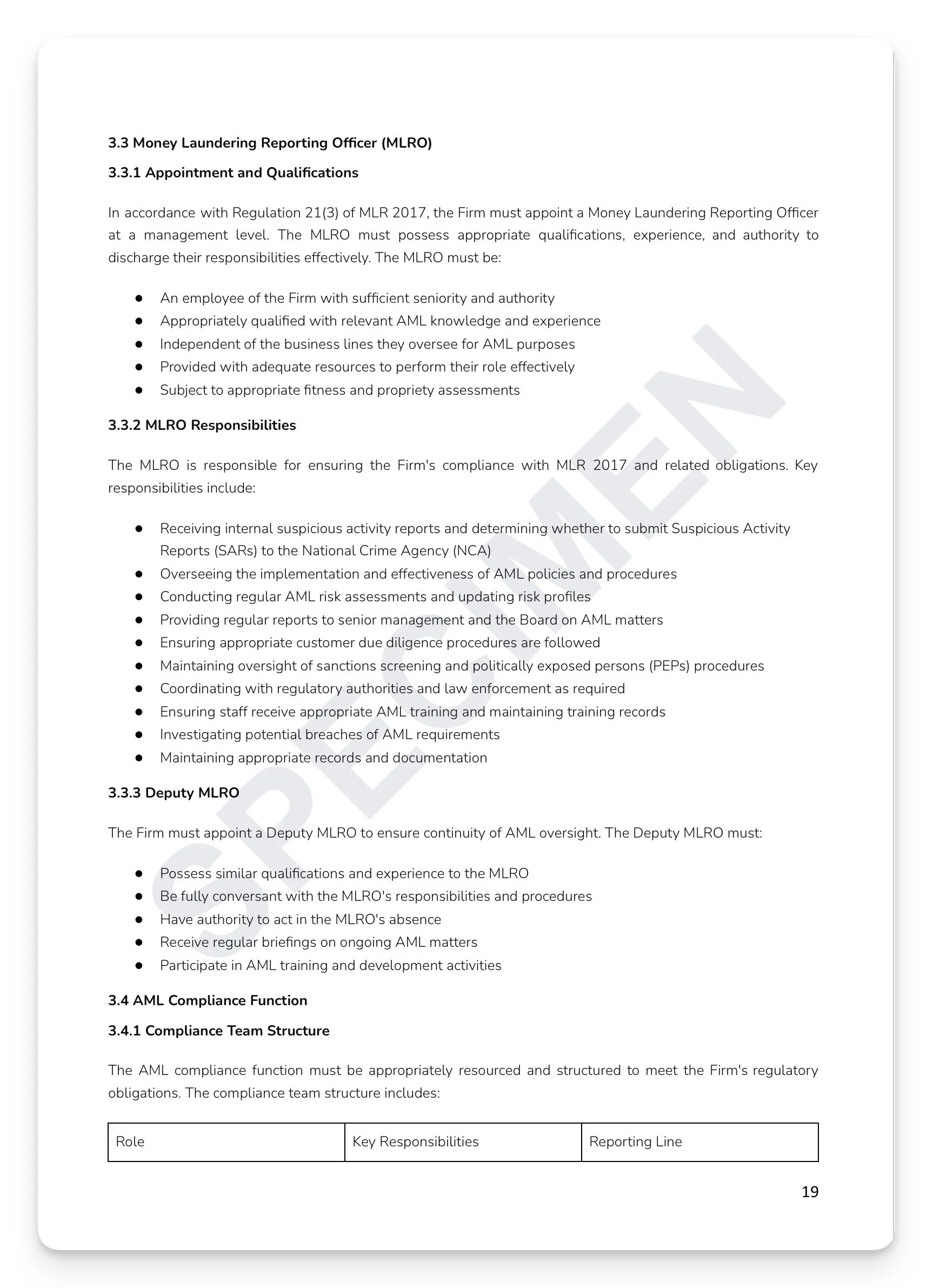

Full Fraud Act 2006 legal analysis: Sections 1–4 (false representation, failing to disclose, abuse of position), dishonesty test per Ivey v Genting Casinos [2017] UKSC 67, criminal penalties (10-year imprisonment, unlimited fines), and corporate liability framework under Section 12

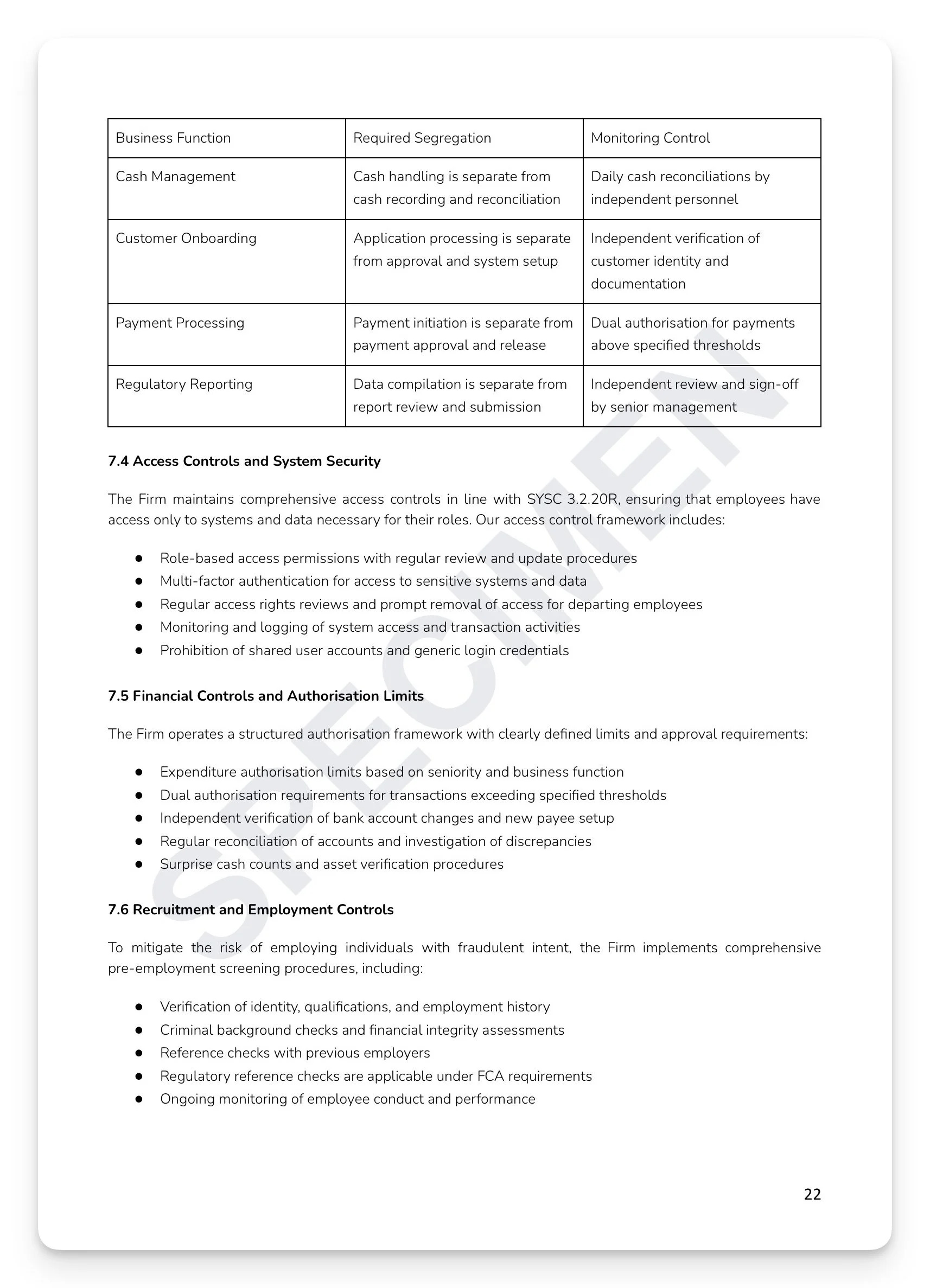

Internal fraud risk catalogue: asset misappropriation, payroll fraud, procurement fraud, expense fraud, and data theft — with segregation of duties matrix across cash management, onboarding, payments, and regulatory reporting

External fraud threat taxonomy: identity, application, payment, cyber, investment, insurance, first-party, and third-party fraud — with product vulnerability assessment framework and real-time transaction monitoring and behavioural analytics integration

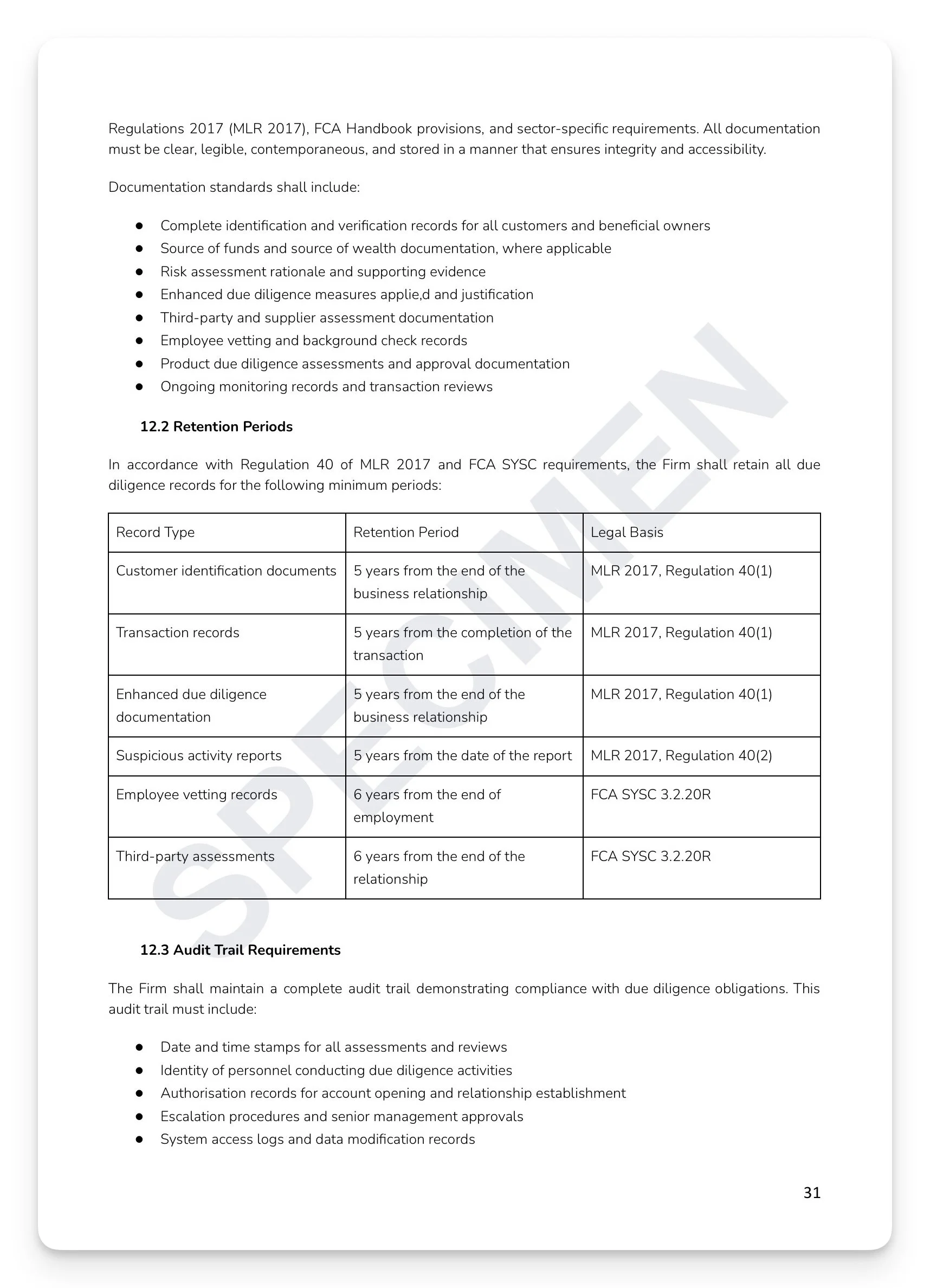

POCA 2002 predicate offence and SAR reporting triggers — with AML/MLR 2017 integration covering CDD, EDD, transaction monitoring alignment, and sanctions screening (SAMLA/OFSI)

Four-tier escalation matrix by fraud value: under £10k through to full Board — with 48-hour investigation initiation requirement and one-business-day FCA notification triggers

Whistleblowing protection: PIDA 1998 and SYSC 18 integration with multi-channel reporting

Three-lines-of-defence governance model with Board, Risk Committee, and Audit Committee fraud reporting schedule — with SM&CR accountability framework and PRIN obligations mapping (Principles 1/2/3/6/11)

+ much more

Who is this for?

Compliance Officers, MLROs, risk functions, and Boards at FCA-regulated firms who need a complete, board-approved Fraud Act-compliant Anti-Fraud framework integrated with their existing financial crime programme.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Fraud costs UK financial services billions every year — and most firms' policies don't cover half of how it happens. The Fraud Act 2006 creates three distinct criminal offences, and your firm can face corporate liability for fraud committed by anyone acting on your behalf. Beyond the criminal exposure, the FCA treats fraud prevention as a core regulatory obligation under SYSC, PRIN, and Consumer Duty. Internal fraud, external fraud, financial crime integration, regulatory governance — most firms have fragments of a framework. Few have the full picture.

What's included:

Full Fraud Act 2006 legal analysis: Sections 1–4 (false representation, failing to disclose, abuse of position), dishonesty test per Ivey v Genting Casinos [2017] UKSC 67, criminal penalties (10-year imprisonment, unlimited fines), and corporate liability framework under Section 12

Internal fraud risk catalogue: asset misappropriation, payroll fraud, procurement fraud, expense fraud, and data theft — with segregation of duties matrix across cash management, onboarding, payments, and regulatory reporting

External fraud threat taxonomy: identity, application, payment, cyber, investment, insurance, first-party, and third-party fraud — with product vulnerability assessment framework and real-time transaction monitoring and behavioural analytics integration

POCA 2002 predicate offence and SAR reporting triggers — with AML/MLR 2017 integration covering CDD, EDD, transaction monitoring alignment, and sanctions screening (SAMLA/OFSI)

Four-tier escalation matrix by fraud value: under £10k through to full Board — with 48-hour investigation initiation requirement and one-business-day FCA notification triggers

Whistleblowing protection: PIDA 1998 and SYSC 18 integration with multi-channel reporting

Three-lines-of-defence governance model with Board, Risk Committee, and Audit Committee fraud reporting schedule — with SM&CR accountability framework and PRIN obligations mapping (Principles 1/2/3/6/11)

+ much more

Who is this for?

Compliance Officers, MLROs, risk functions, and Boards at FCA-regulated firms who need a complete, board-approved Fraud Act-compliant Anti-Fraud framework integrated with their existing financial crime programme.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 8

Image 1 of 8

Image 2 of 8

Image 2 of 8

Image 3 of 8

Image 3 of 8

Image 4 of 8

Image 4 of 8

Image 5 of 8

Image 5 of 8

Image 6 of 8

Image 6 of 8

Image 7 of 8

Image 7 of 8

Image 8 of 8

Image 8 of 8