Every insurance intermediary knows ICOBS exists. What few have addressed is its intersection with Consumer Duty, the IDD's product governance requirements, the IPID mandate, and the CASS 5 client money framework — simultaneously, across every distribution channel, for every customer category. The FCA's thematic reviews consistently find the same failures: inadequate needs assessments, IPIDs delivered late, commission disclosure deficiencies, client money segregation gaps, and Consumer Duty outcomes not monitored beyond the point of sale. The IPID is three pages. Getting it wrong costs considerably more.

What's included:

Full regulatory mapping: ICOBS 2–9, PRIN 2A (Consumer Duty), DISP 1, CASS 5, TC 2.1.1R, SYSC 4.1.1R/6.1.1R, SM&CR, UK GDPR/DPA 2018, and IDD

IPID framework: mandatory content, 3-page/10pt format standards, manufacturer vs distributor obligations, and delivery timing requirements — not at conclusion, but in good time

Consumer Duty implementation: four outcomes framework, fair value assessment, vulnerable customer identification, digital communication standards, and Board MI requirements

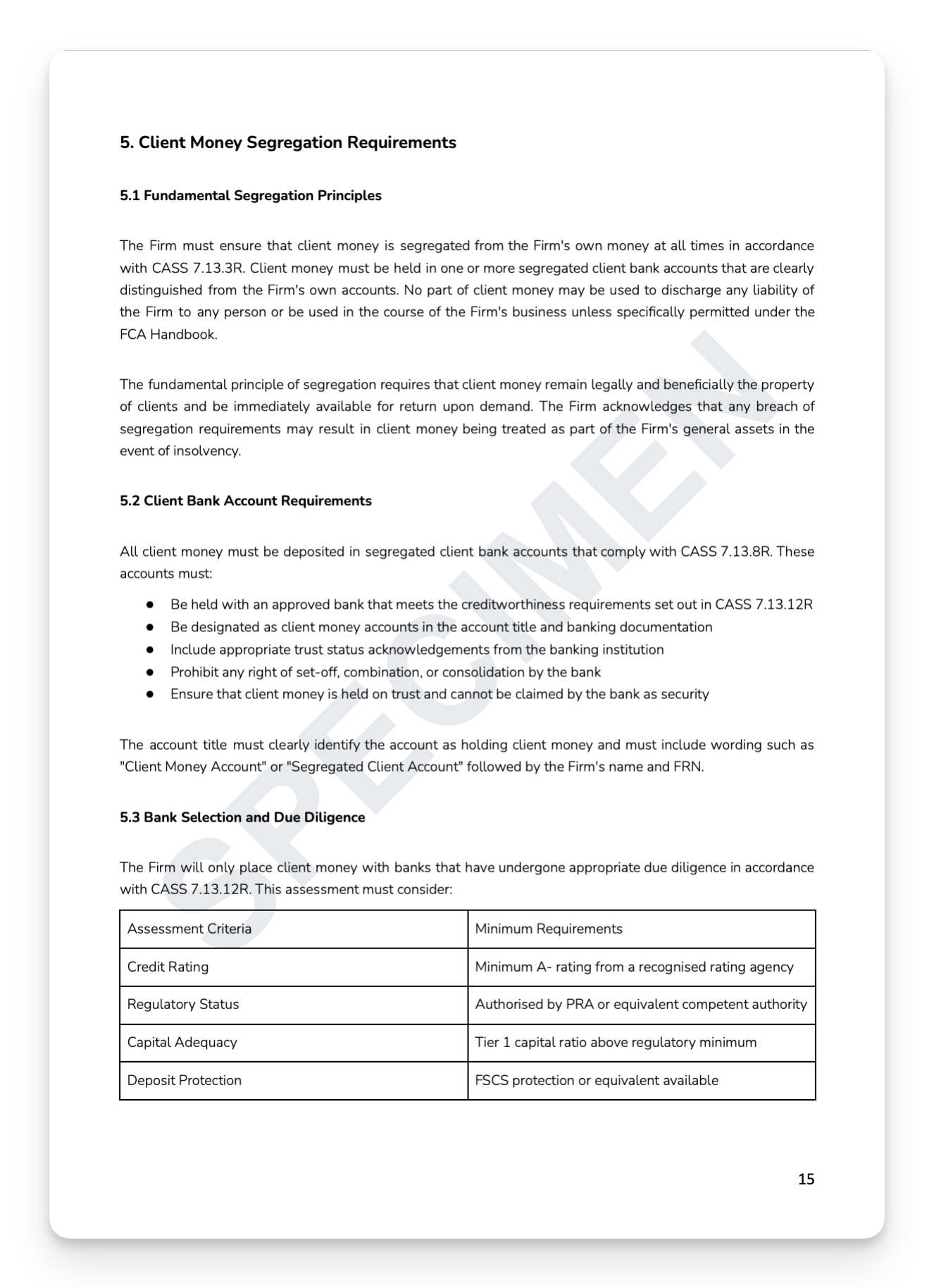

Client money framework: CASS 5 statutory trust obligations, immediate segregation, approved bank due diligence, daily reconciliation, and premium collection and claims payment procedures

Conflicts and commission: ICOBS 6.1A disclosure requirements, quantified monetary disclosure, volume incentive controls, churning prevention, and unusual sales pattern monitoring

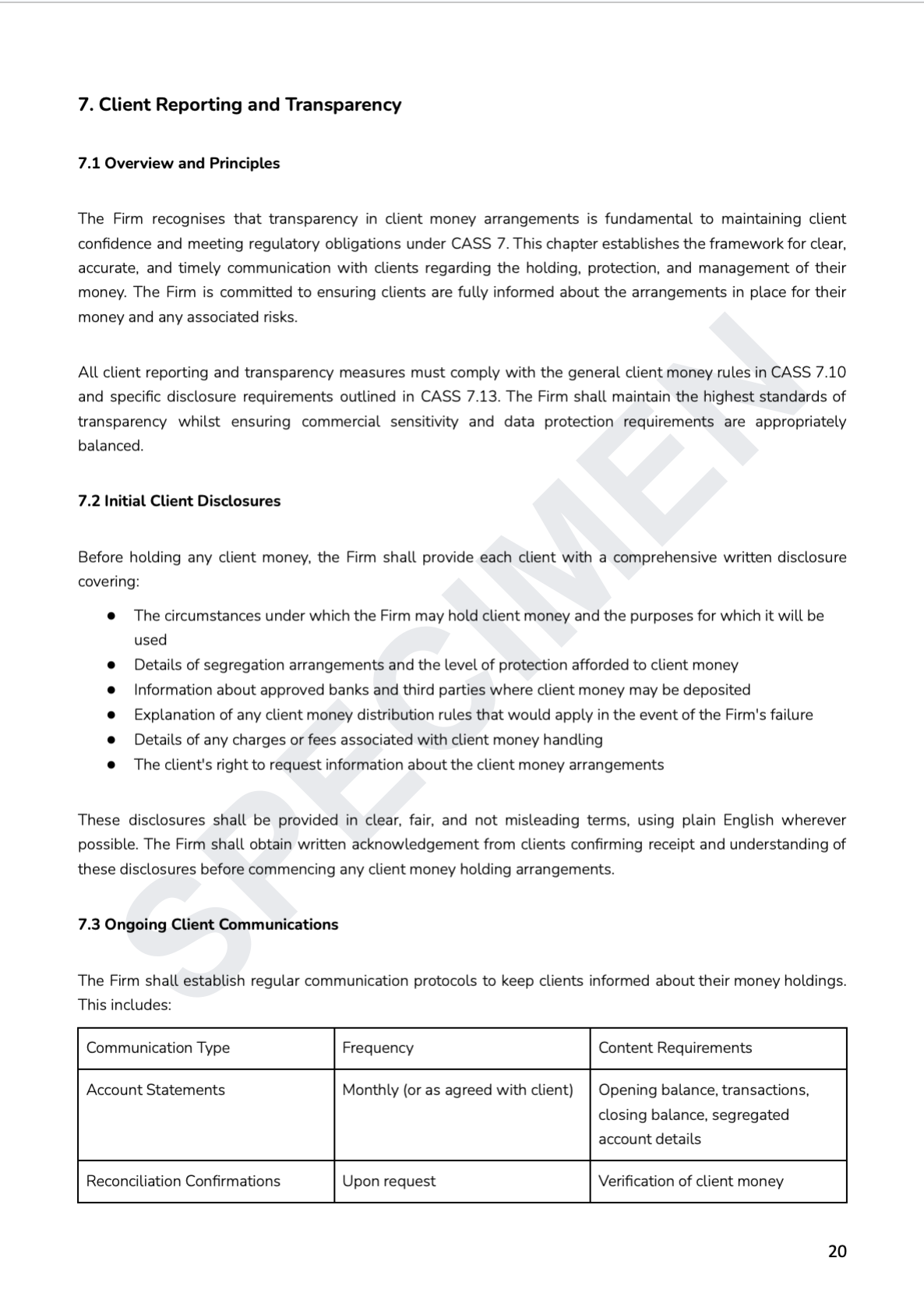

Complaints handling: DISP 1 written procedures, 5-day acknowledgement, 8-week final response, FOS referral rights, redress calculation, and 5-year record retention

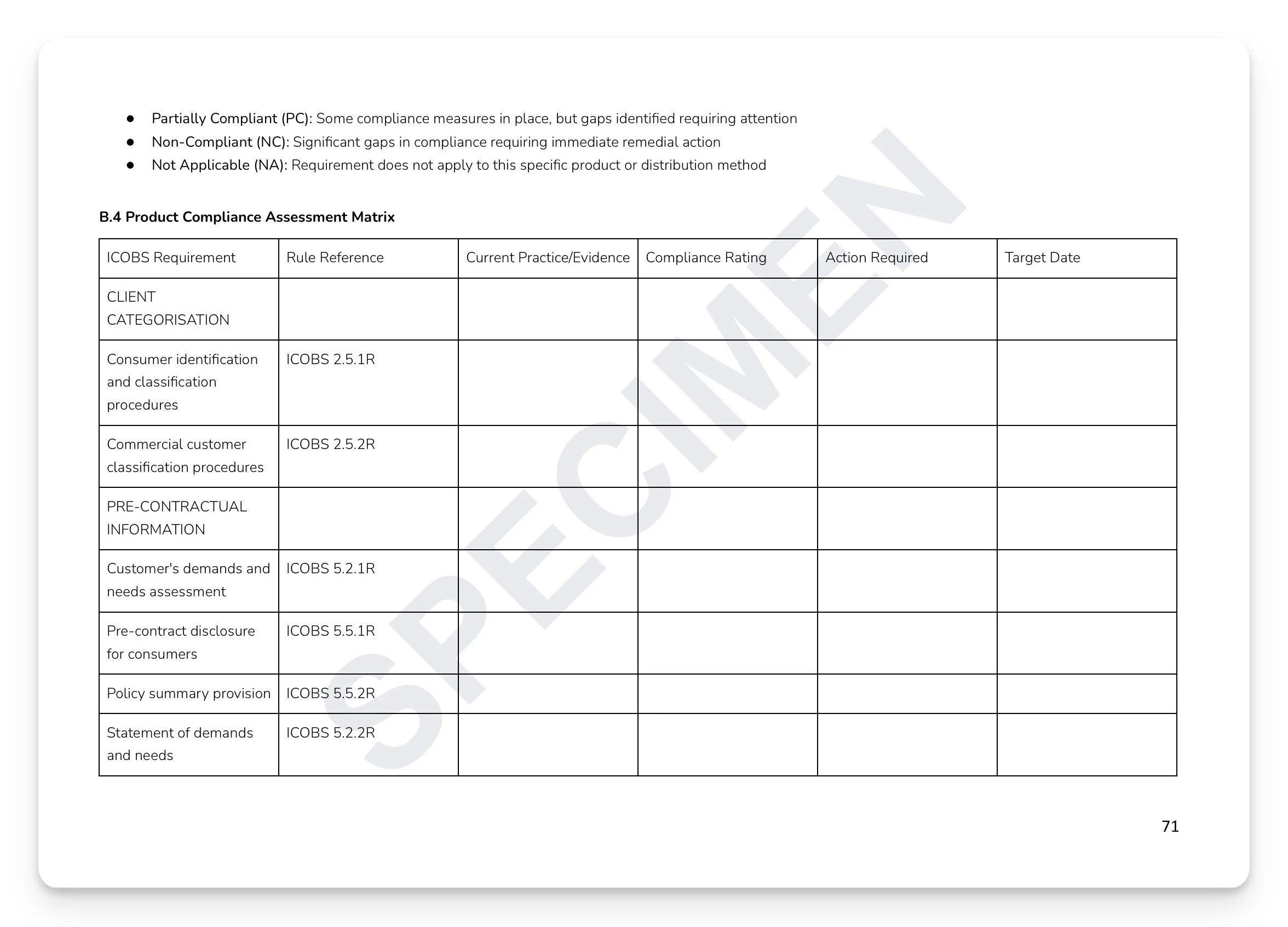

Ready-to-use appendices: Client Categorisation Assessment, Pre-Contractual Information Checklist, Consumer Duty Fair Value Assessment Template, Distance Selling Verification, MI Dashboard, and full Product Compliance Assessment Matrix

+ much more

Who is this for?

Compliance Officers, SMF16 holders, insurance intermediaries, general insurance and protection distributors, and governance teams at FCA-regulated firms who need a complete, board-approved ICOBS compliance manual with working templates that double as evidence for supervisory review.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Every insurance intermediary knows ICOBS exists. What few have addressed is its intersection with Consumer Duty, the IDD's product governance requirements, the IPID mandate, and the CASS 5 client money framework — simultaneously, across every distribution channel, for every customer category. The FCA's thematic reviews consistently find the same failures: inadequate needs assessments, IPIDs delivered late, commission disclosure deficiencies, client money segregation gaps, and Consumer Duty outcomes not monitored beyond the point of sale. The IPID is three pages. Getting it wrong costs considerably more.

What's included:

Full regulatory mapping: ICOBS 2–9, PRIN 2A (Consumer Duty), DISP 1, CASS 5, TC 2.1.1R, SYSC 4.1.1R/6.1.1R, SM&CR, UK GDPR/DPA 2018, and IDD

IPID framework: mandatory content, 3-page/10pt format standards, manufacturer vs distributor obligations, and delivery timing requirements — not at conclusion, but in good time

Consumer Duty implementation: four outcomes framework, fair value assessment, vulnerable customer identification, digital communication standards, and Board MI requirements

Client money framework: CASS 5 statutory trust obligations, immediate segregation, approved bank due diligence, daily reconciliation, and premium collection and claims payment procedures

Conflicts and commission: ICOBS 6.1A disclosure requirements, quantified monetary disclosure, volume incentive controls, churning prevention, and unusual sales pattern monitoring

Complaints handling: DISP 1 written procedures, 5-day acknowledgement, 8-week final response, FOS referral rights, redress calculation, and 5-year record retention

Ready-to-use appendices: Client Categorisation Assessment, Pre-Contractual Information Checklist, Consumer Duty Fair Value Assessment Template, Distance Selling Verification, MI Dashboard, and full Product Compliance Assessment Matrix

+ much more

Who is this for?

Compliance Officers, SMF16 holders, insurance intermediaries, general insurance and protection distributors, and governance teams at FCA-regulated firms who need a complete, board-approved ICOBS compliance manual with working templates that double as evidence for supervisory review.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 13

Image 1 of 13

Image 2 of 13

Image 2 of 13

Image 3 of 13

Image 3 of 13

Image 4 of 13

Image 4 of 13

Image 5 of 13

Image 5 of 13

Image 6 of 13

Image 6 of 13

Image 7 of 13

Image 7 of 13

Image 8 of 13

Image 8 of 13

Image 9 of 13

Image 9 of 13

Image 10 of 13

Image 10 of 13

Image 11 of 13

Image 11 of 13

Image 12 of 13

Image 12 of 13

Image 13 of 13

Image 13 of 13