Sanctions is the one area where "we didn't know" is not a defence. Under the Sanctions and Anti-Money Laundering Act 2018, sanctions violations are a matter of strict liability. Civil penalties require no proof of intent — if your firm provides funds or economic resources to a designated person, you've breached UK law regardless of whether you knew. OFSI can fine you up to £1 million or 50% of the transaction value. Criminal prosecution carries up to seven years' imprisonment. The FCA can act on top of that for systems and controls failures. When strict liability applies, your only protection is a framework that works.

What's included:

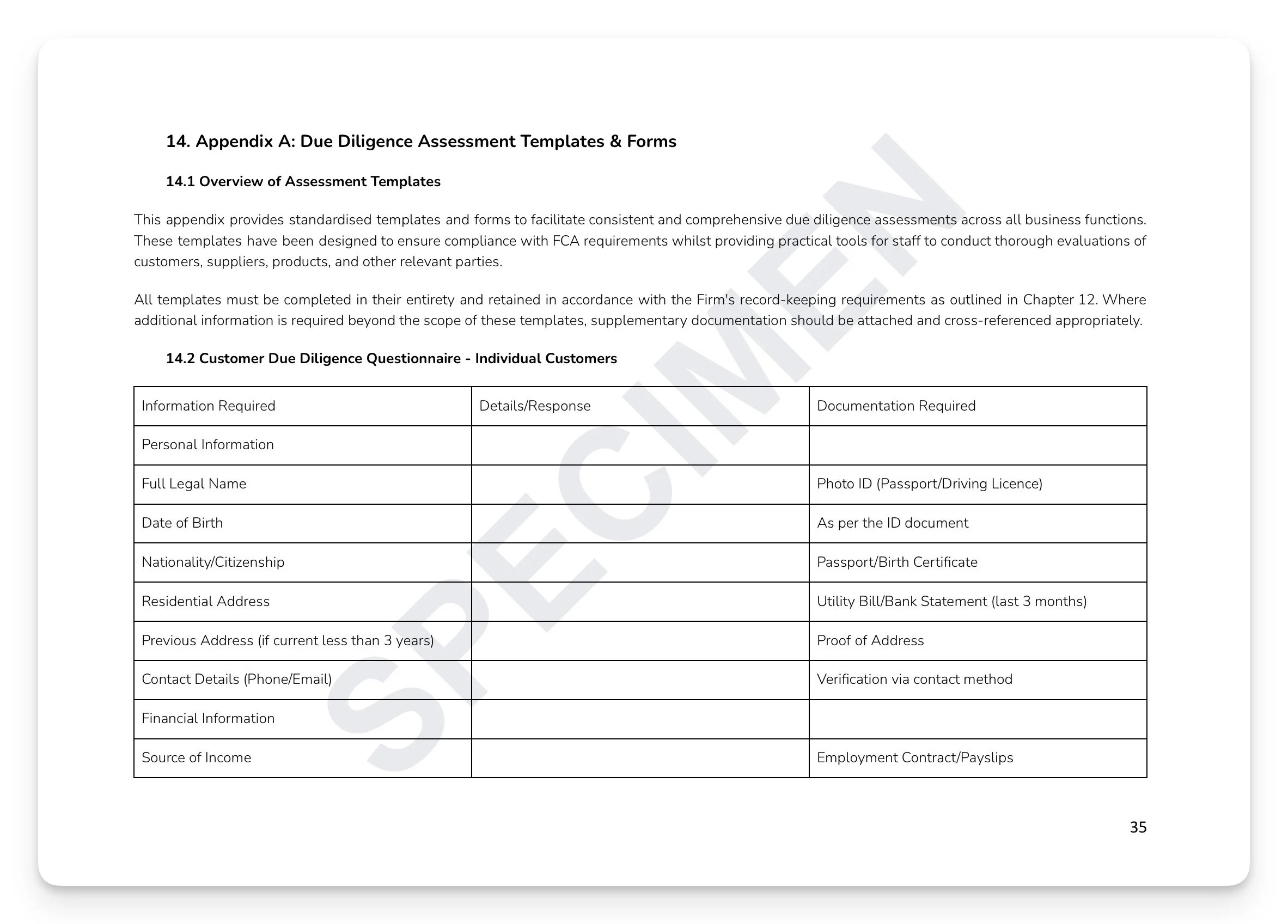

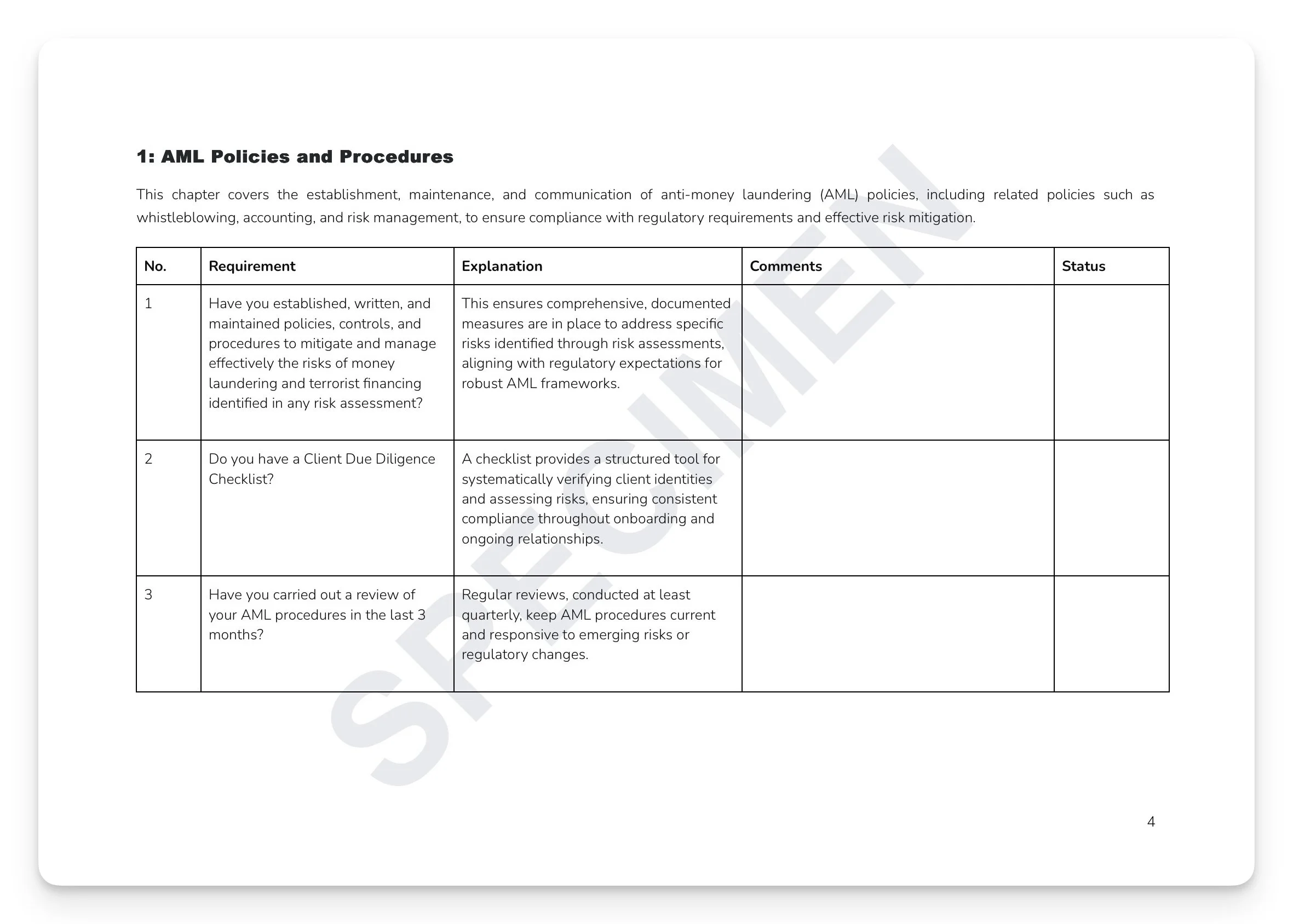

Full UK regulatory framework: SAMLA 2018 Sections 11/15/21/21C/34/64, SYSC 6.3.1R/6.3.7G, FCA Financial Crime Guide Chapter 7, OFSI General Guidance (June 2024 update), and FATF recommendations

Real-time transaction screening: 85% fuzzy matching threshold, 30-second maximum response time, and payment blocking procedures — with daily screening of existing customer databases against the OFSI Consolidated List, UN Security Council, and EU sanctions lists

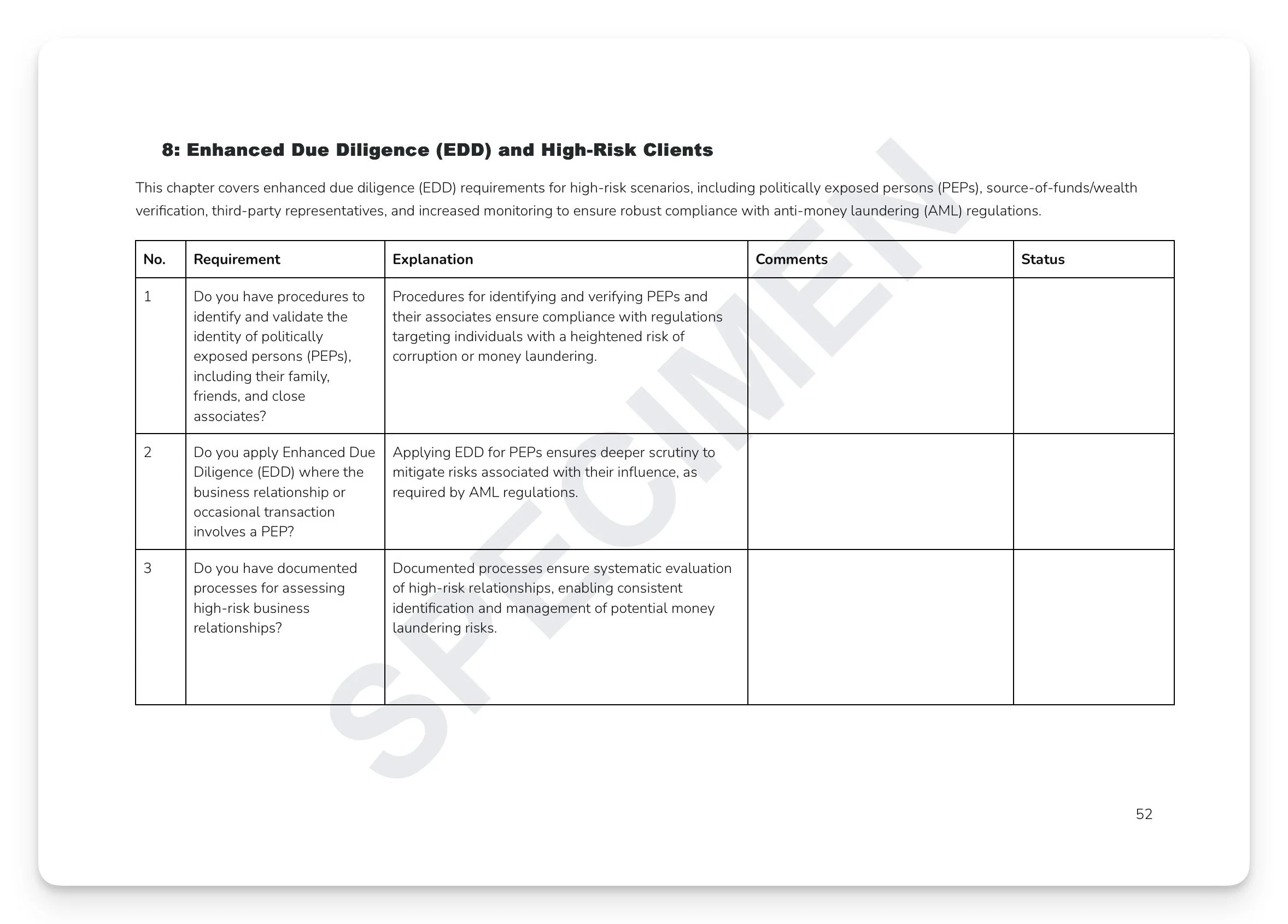

Sanctions evasion detection: structuring patterns, complex ownership structures, virtual asset circumvention, and jurisdictional arbitrage indicators

OFSI licensing framework: general licence compliance, specific licence application process, humanitarian exceptions, and wind-down licences — with SAMLA Section 21C immediate notification and 21-day detailed written report

Four-level internal escalation matrix: 2 hours, 4 hours, 8 hours, and 24 hours — with breach classification and FCA SUP 15.3 notification triggers

Third-party risk assessment: monthly through biennial monitoring frequencies — with mandatory contractual protections including sanctions warranty, ongoing screening obligation, audit rights, and immediate termination trigger

Ready-to-use appendices: product and service assessment template, quarterly sanctions compliance checklist, and key OFSI/FCA/NCA regulatory contacts

+ much more

Who is this for?

MLROs, Compliance Officers, SMF holders, and sanctions officers at FCA-regulated firms who need a complete, board-approved SAMLA 2018-compliant Sanctions framework with robust screening, breach response, and governance controls capable of withstanding regulatory examination.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Sanctions is the one area where "we didn't know" is not a defence. Under the Sanctions and Anti-Money Laundering Act 2018, sanctions violations are a matter of strict liability. Civil penalties require no proof of intent — if your firm provides funds or economic resources to a designated person, you've breached UK law regardless of whether you knew. OFSI can fine you up to £1 million or 50% of the transaction value. Criminal prosecution carries up to seven years' imprisonment. The FCA can act on top of that for systems and controls failures. When strict liability applies, your only protection is a framework that works.

What's included:

Full UK regulatory framework: SAMLA 2018 Sections 11/15/21/21C/34/64, SYSC 6.3.1R/6.3.7G, FCA Financial Crime Guide Chapter 7, OFSI General Guidance (June 2024 update), and FATF recommendations

Real-time transaction screening: 85% fuzzy matching threshold, 30-second maximum response time, and payment blocking procedures — with daily screening of existing customer databases against the OFSI Consolidated List, UN Security Council, and EU sanctions lists

Sanctions evasion detection: structuring patterns, complex ownership structures, virtual asset circumvention, and jurisdictional arbitrage indicators

OFSI licensing framework: general licence compliance, specific licence application process, humanitarian exceptions, and wind-down licences — with SAMLA Section 21C immediate notification and 21-day detailed written report

Four-level internal escalation matrix: 2 hours, 4 hours, 8 hours, and 24 hours — with breach classification and FCA SUP 15.3 notification triggers

Third-party risk assessment: monthly through biennial monitoring frequencies — with mandatory contractual protections including sanctions warranty, ongoing screening obligation, audit rights, and immediate termination trigger

Ready-to-use appendices: product and service assessment template, quarterly sanctions compliance checklist, and key OFSI/FCA/NCA regulatory contacts

+ much more

Who is this for?

MLROs, Compliance Officers, SMF holders, and sanctions officers at FCA-regulated firms who need a complete, board-approved SAMLA 2018-compliant Sanctions framework with robust screening, breach response, and governance controls capable of withstanding regulatory examination.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7