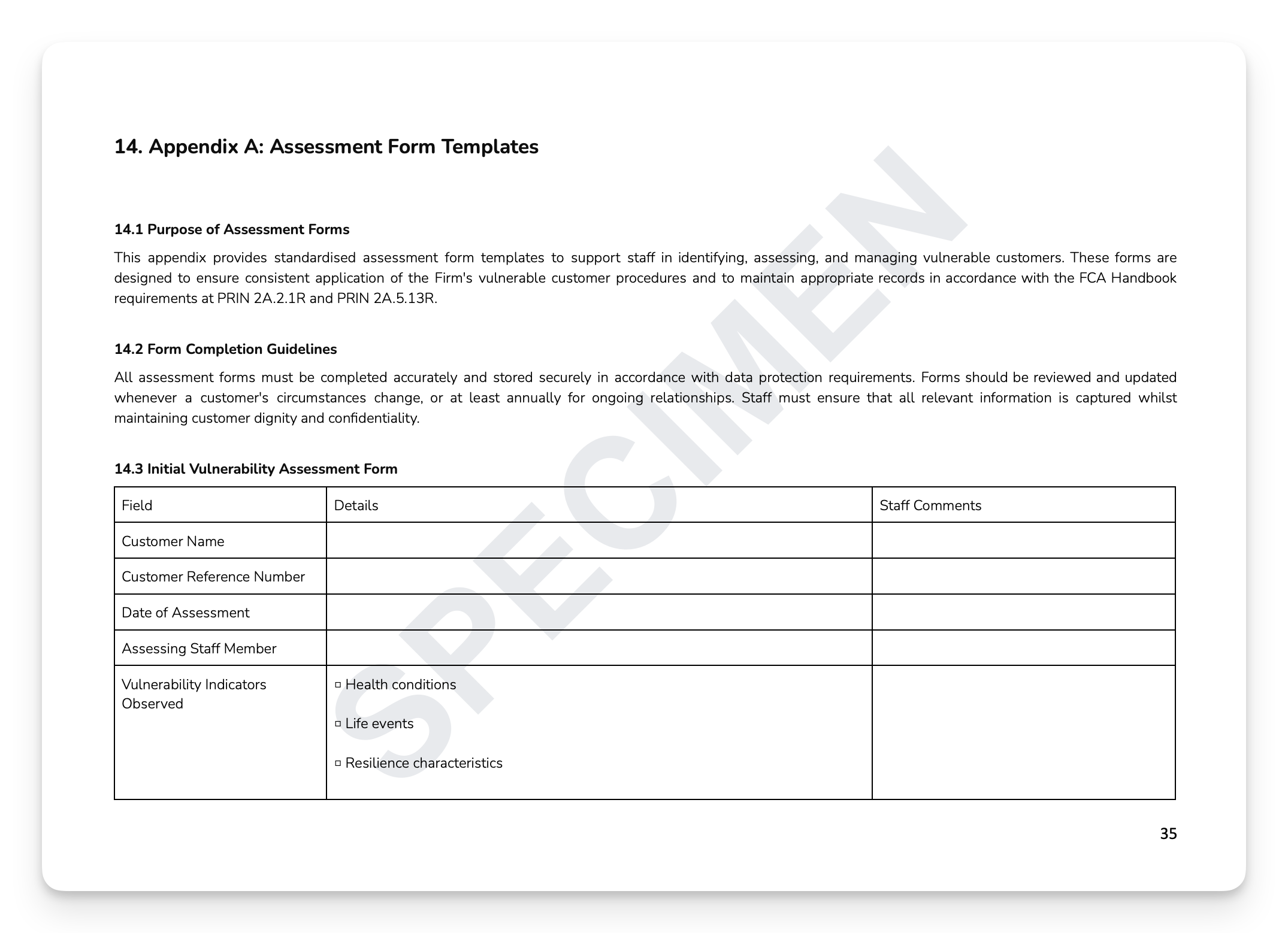

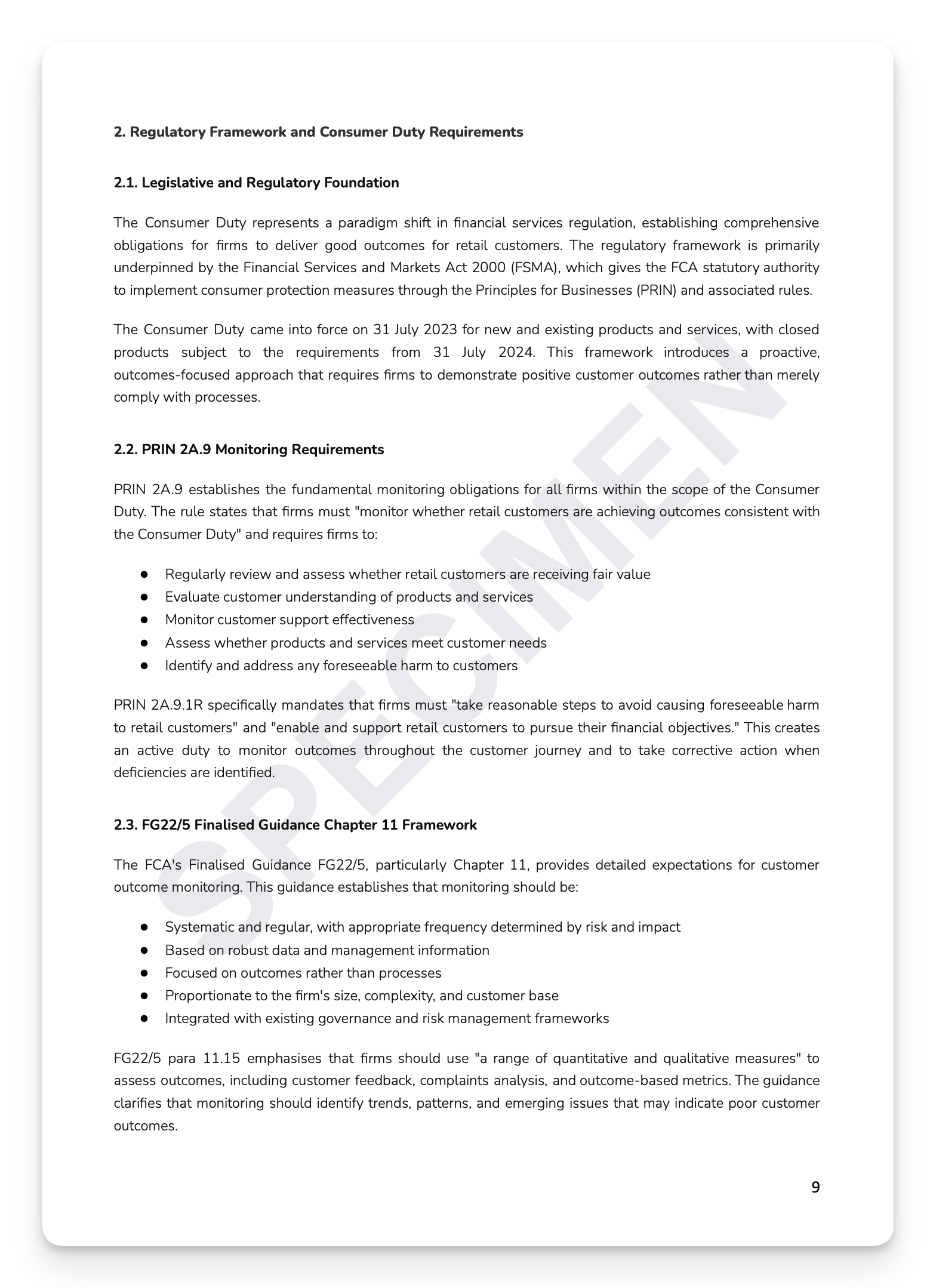

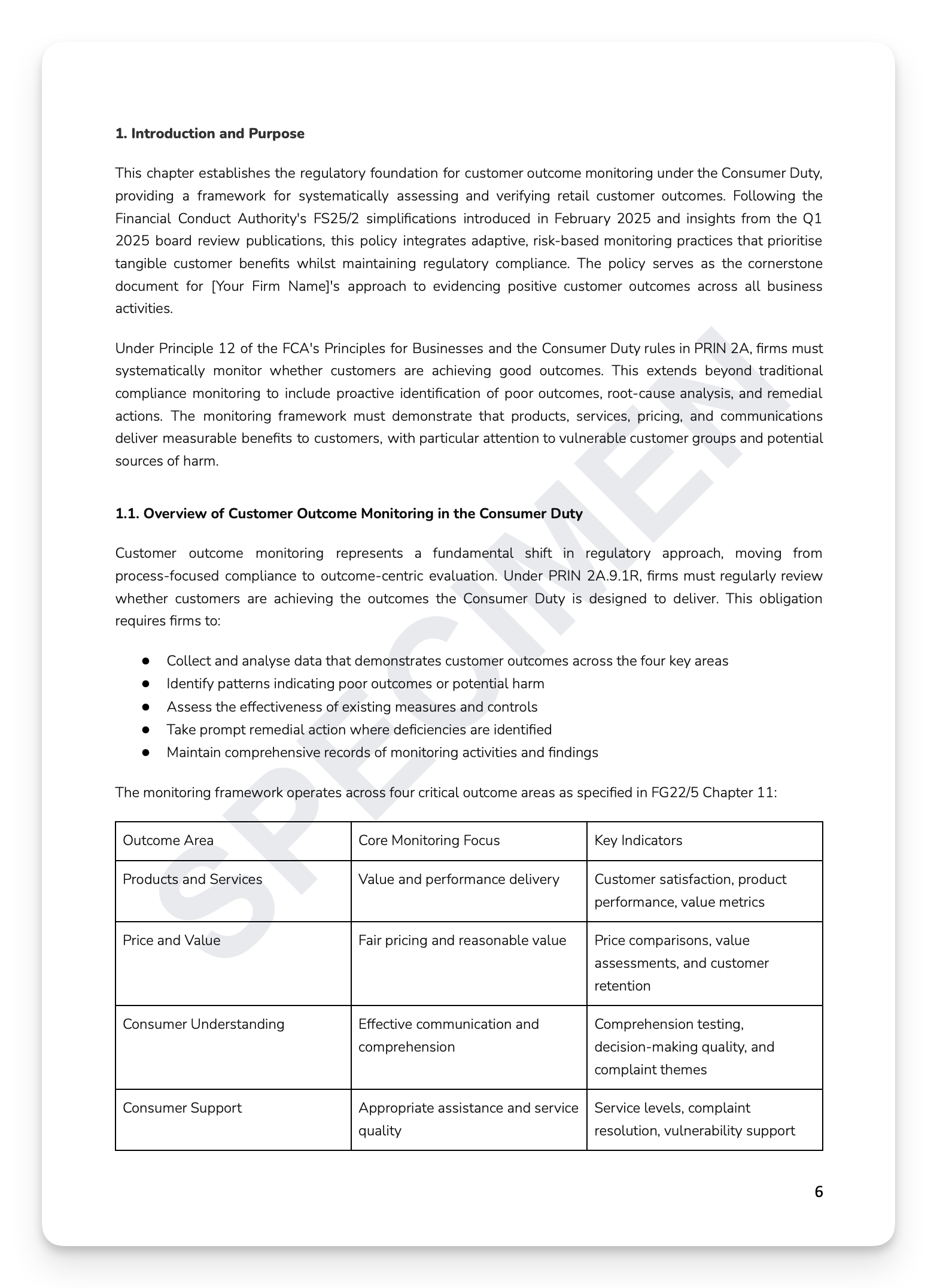

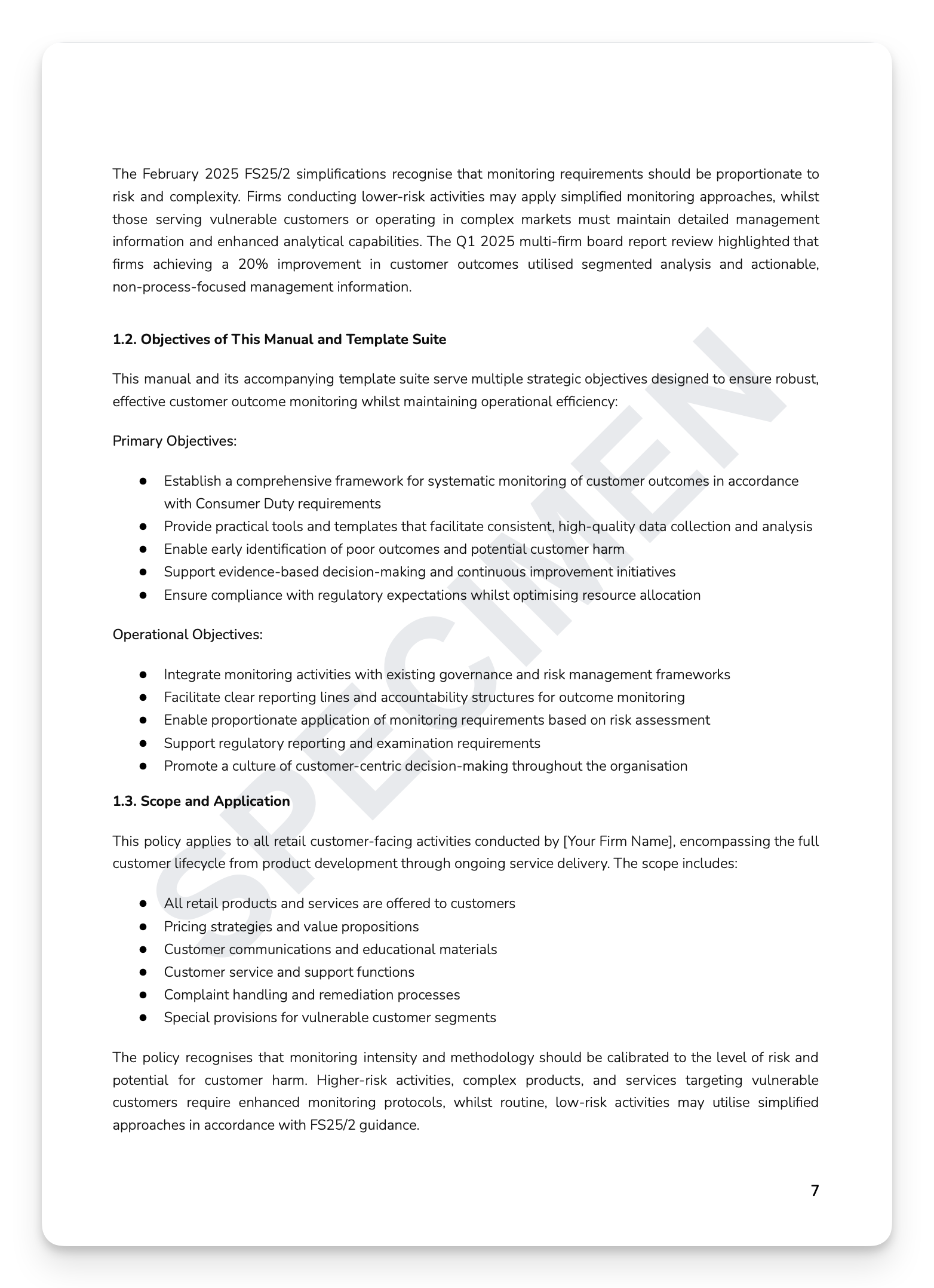

Identifying that something went wrong is the beginning, not the end. Under Consumer Duty, the FCA expects firms to understand why it went wrong, whether the same cause is producing harm elsewhere in the business, and what systemic changes will prevent recurrence. Firms that cannot evidence a structured RCA methodology are demonstrating exactly the kind of reactive compliance culture the Duty was designed to eliminate. The FCA doesn't wait.

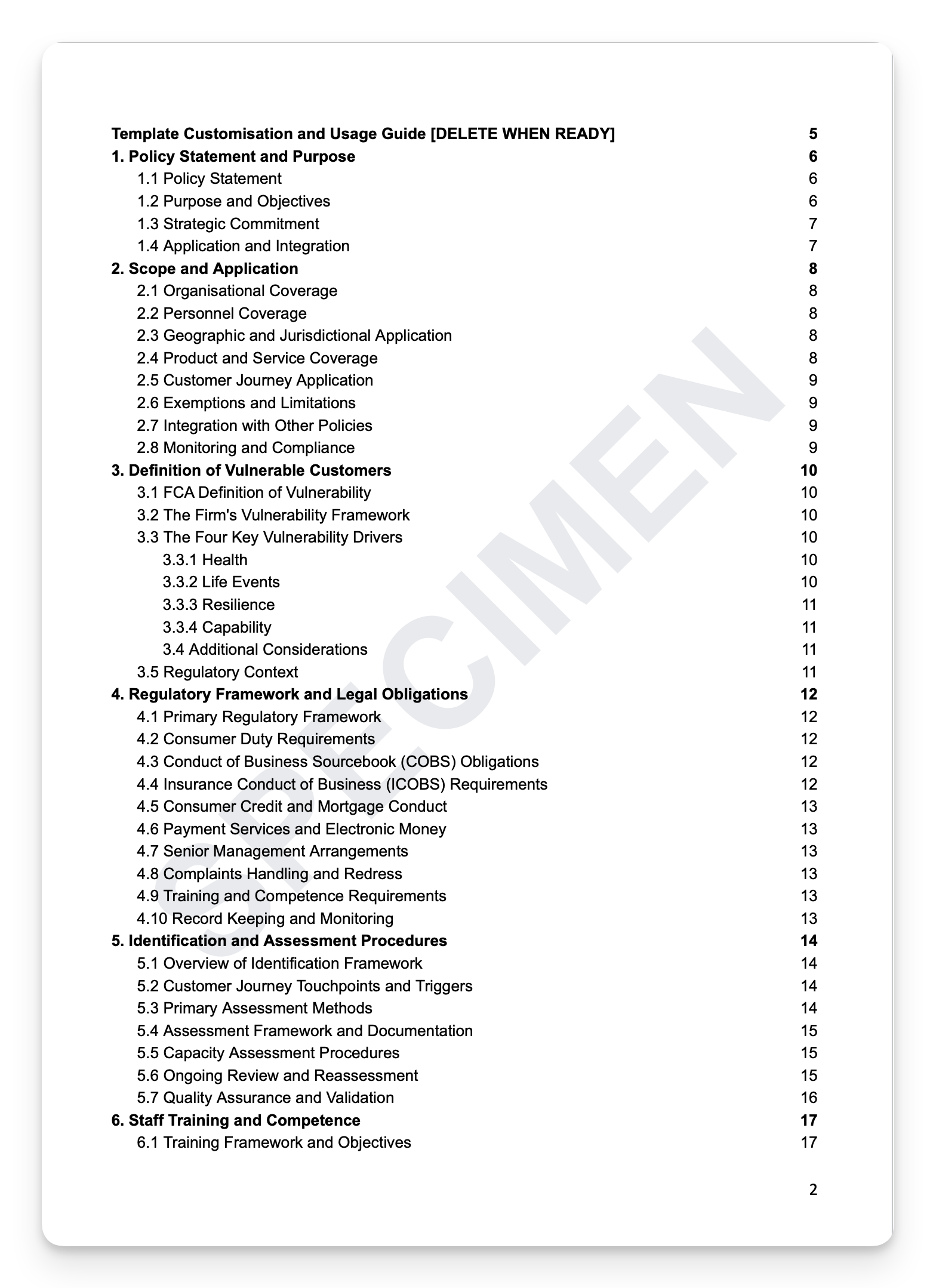

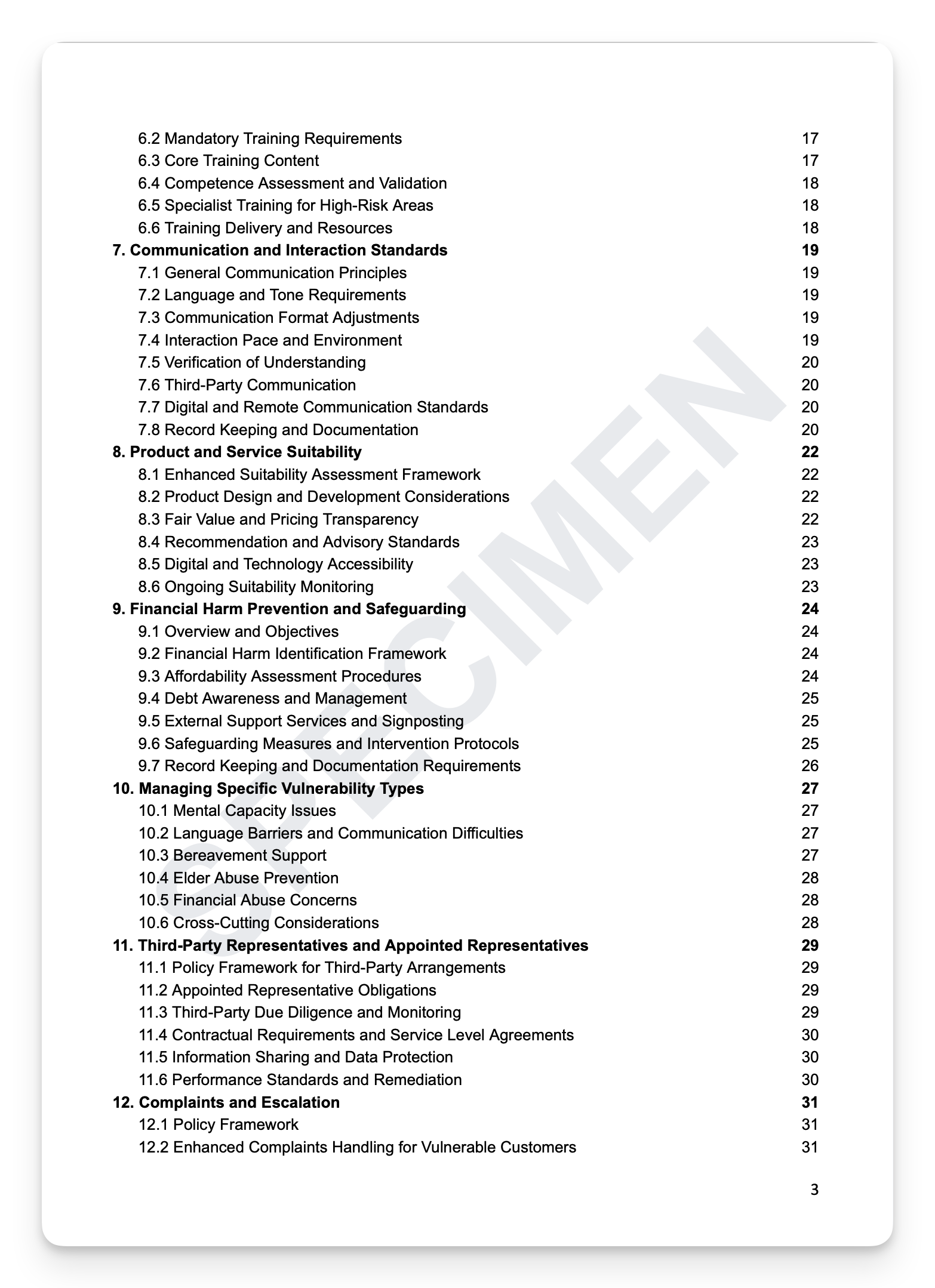

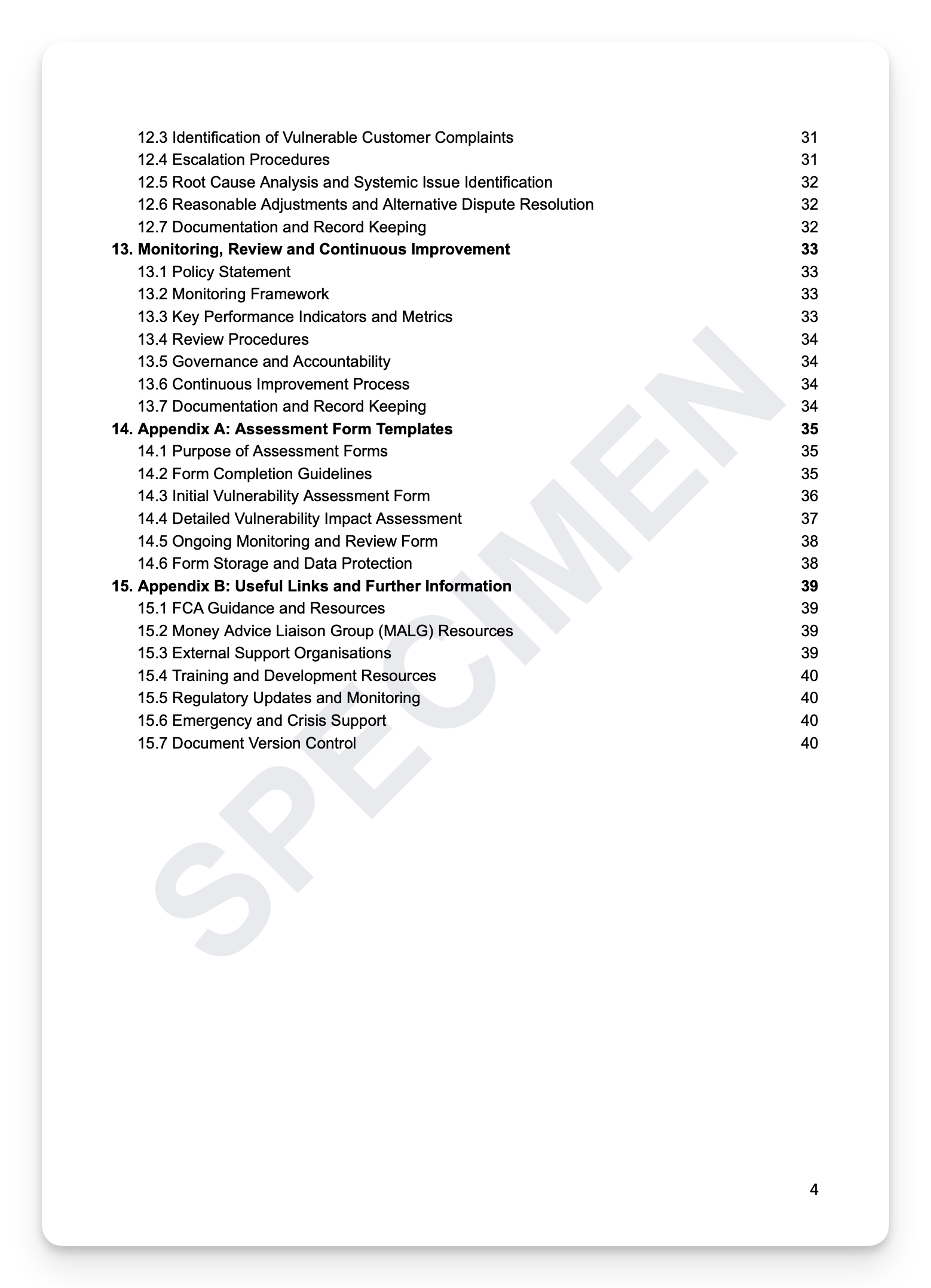

What's included:

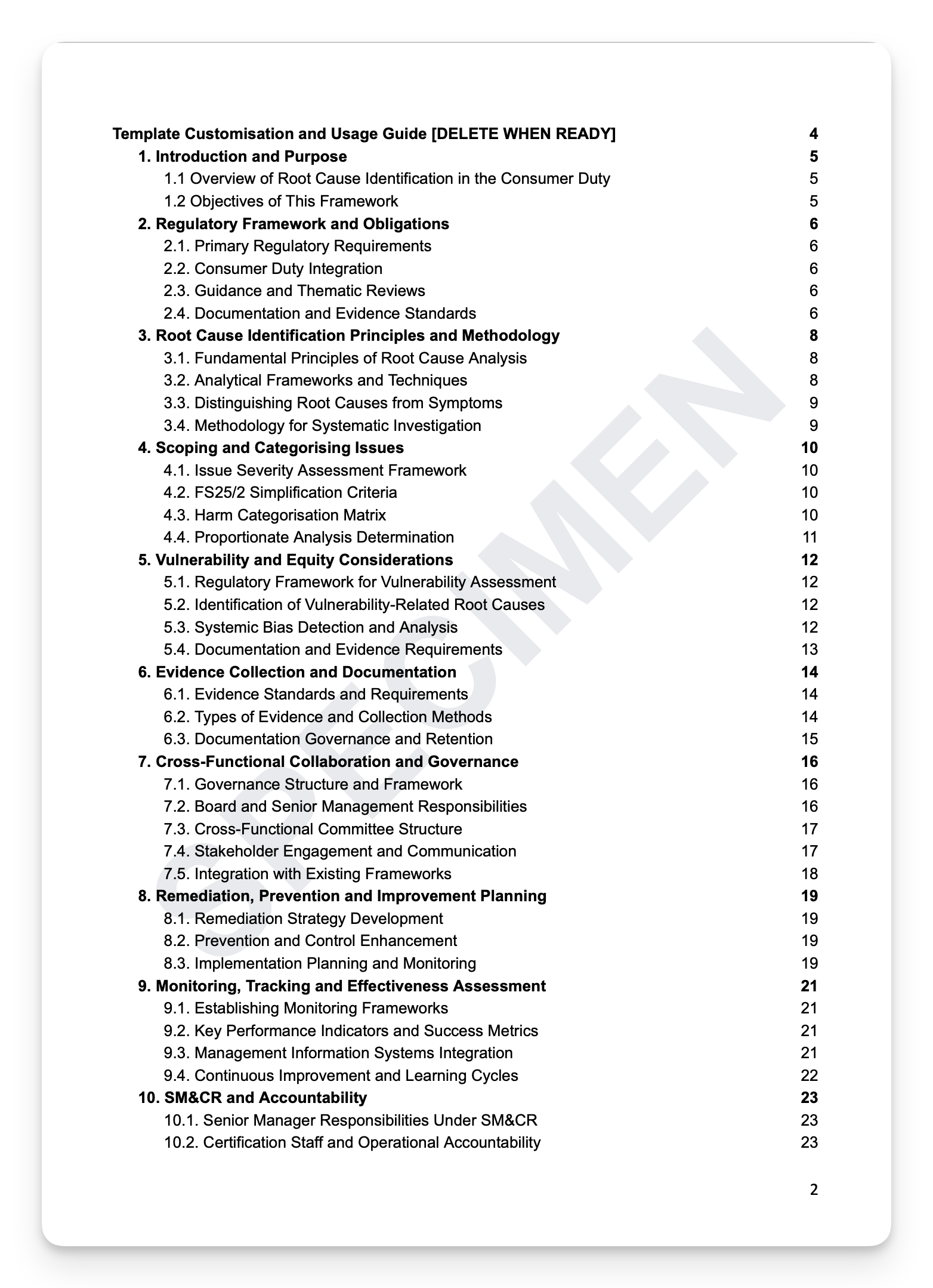

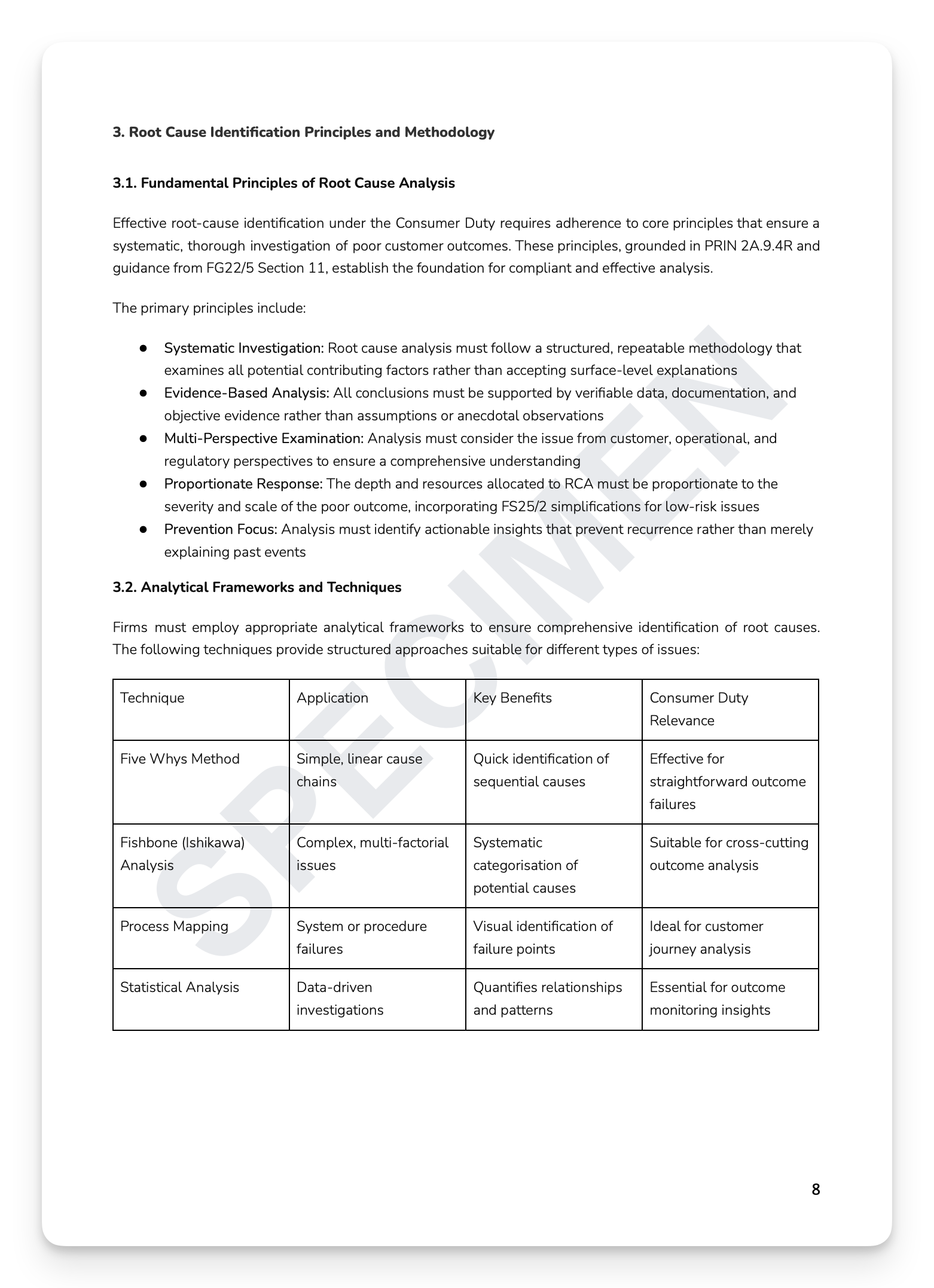

RCA methodology: fundamental principles, analytical frameworks (Five Whys, fishbone, fault tree), and systematic investigation methodology

Issue scoping and categorisation: severity assessment, FS25/2 simplification criteria, harm categorisation matrix, and proportionate analysis

Vulnerability and equity considerations: vulnerability-related root cause identification, systemic bias detection, and evidence requirements

Cross-functional governance: Board and Senior Management responsibilities, cross-functional committee structure, and integration with existing frameworks

Remediation and prevention: strategy development, control enhancement, implementation planning, and monitoring

SM&CR accountability: Senior Manager responsibilities, Certification Staff obligations, and documentation and sign-off requirements

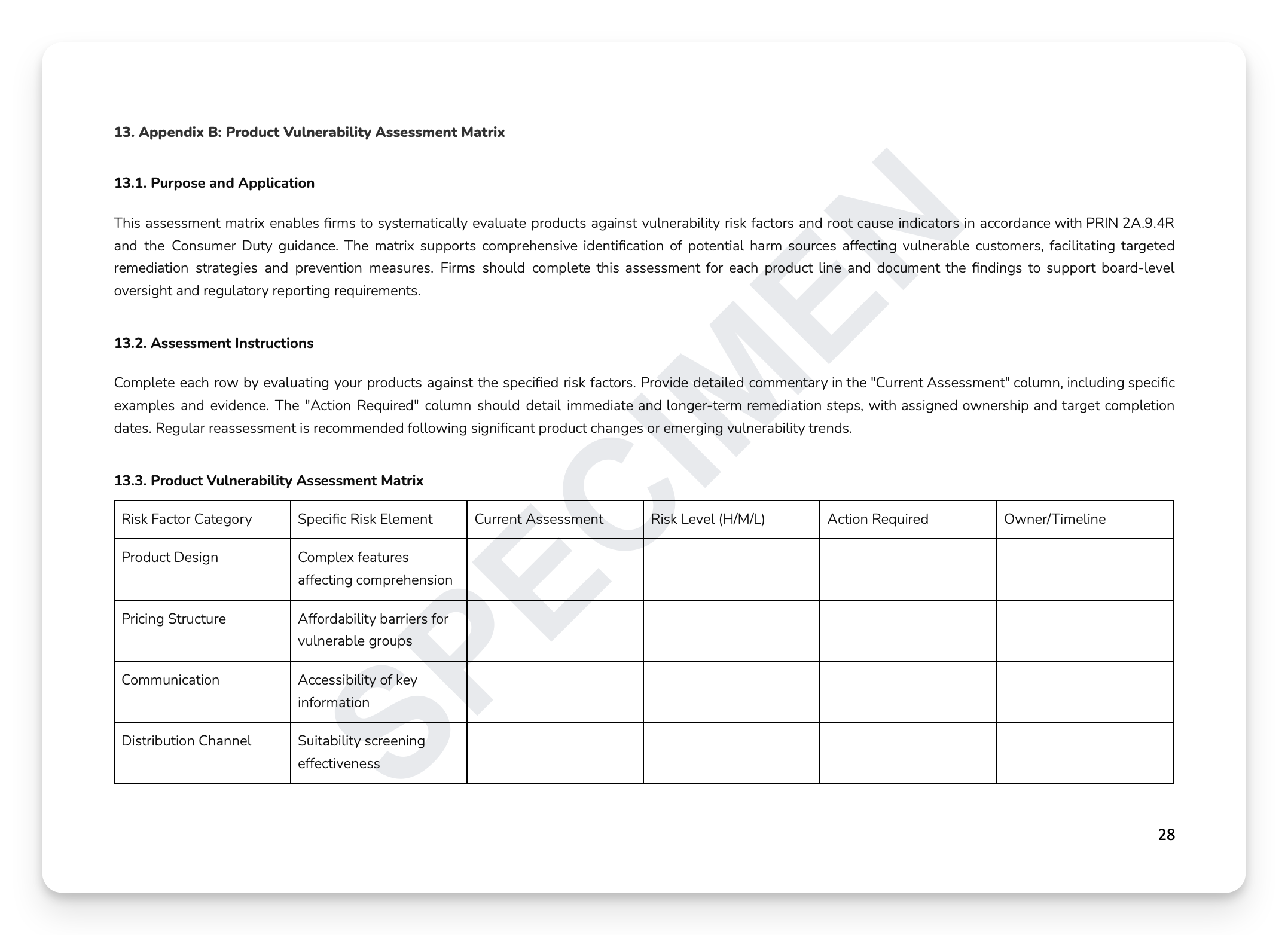

Ready-to-use appendices: Initial Issue Assessment Template, Evidence Collection Checklist, Multi-Business Line Impact Assessment, and Product Vulnerability Assessment Matrix

+ much more

Who is this for?

Compliance Officers, Consumer Duty leads, Risk Managers, SMF holders, and Boards at FCA-regulated firms.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Identifying that something went wrong is the beginning, not the end. Under Consumer Duty, the FCA expects firms to understand why it went wrong, whether the same cause is producing harm elsewhere in the business, and what systemic changes will prevent recurrence. Firms that cannot evidence a structured RCA methodology are demonstrating exactly the kind of reactive compliance culture the Duty was designed to eliminate. The FCA doesn't wait.

What's included:

RCA methodology: fundamental principles, analytical frameworks (Five Whys, fishbone, fault tree), and systematic investigation methodology

Issue scoping and categorisation: severity assessment, FS25/2 simplification criteria, harm categorisation matrix, and proportionate analysis

Vulnerability and equity considerations: vulnerability-related root cause identification, systemic bias detection, and evidence requirements

Cross-functional governance: Board and Senior Management responsibilities, cross-functional committee structure, and integration with existing frameworks

Remediation and prevention: strategy development, control enhancement, implementation planning, and monitoring

SM&CR accountability: Senior Manager responsibilities, Certification Staff obligations, and documentation and sign-off requirements

Ready-to-use appendices: Initial Issue Assessment Template, Evidence Collection Checklist, Multi-Business Line Impact Assessment, and Product Vulnerability Assessment Matrix

+ much more

Who is this for?

Compliance Officers, Consumer Duty leads, Risk Managers, SMF holders, and Boards at FCA-regulated firms.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7