Your AML programme is only as strong as your last honest audit. When did you last do one? The FCA doesn't just want to see policies — it wants evidence you've tested them. Most firms conduct informal reviews when something goes wrong. Few have a structured, documented audit process that systematically tests every element of their AML and financial crime framework and produces the evidence a regulator can inspect. Over 300 requirements. One document. No gaps.

What's included:

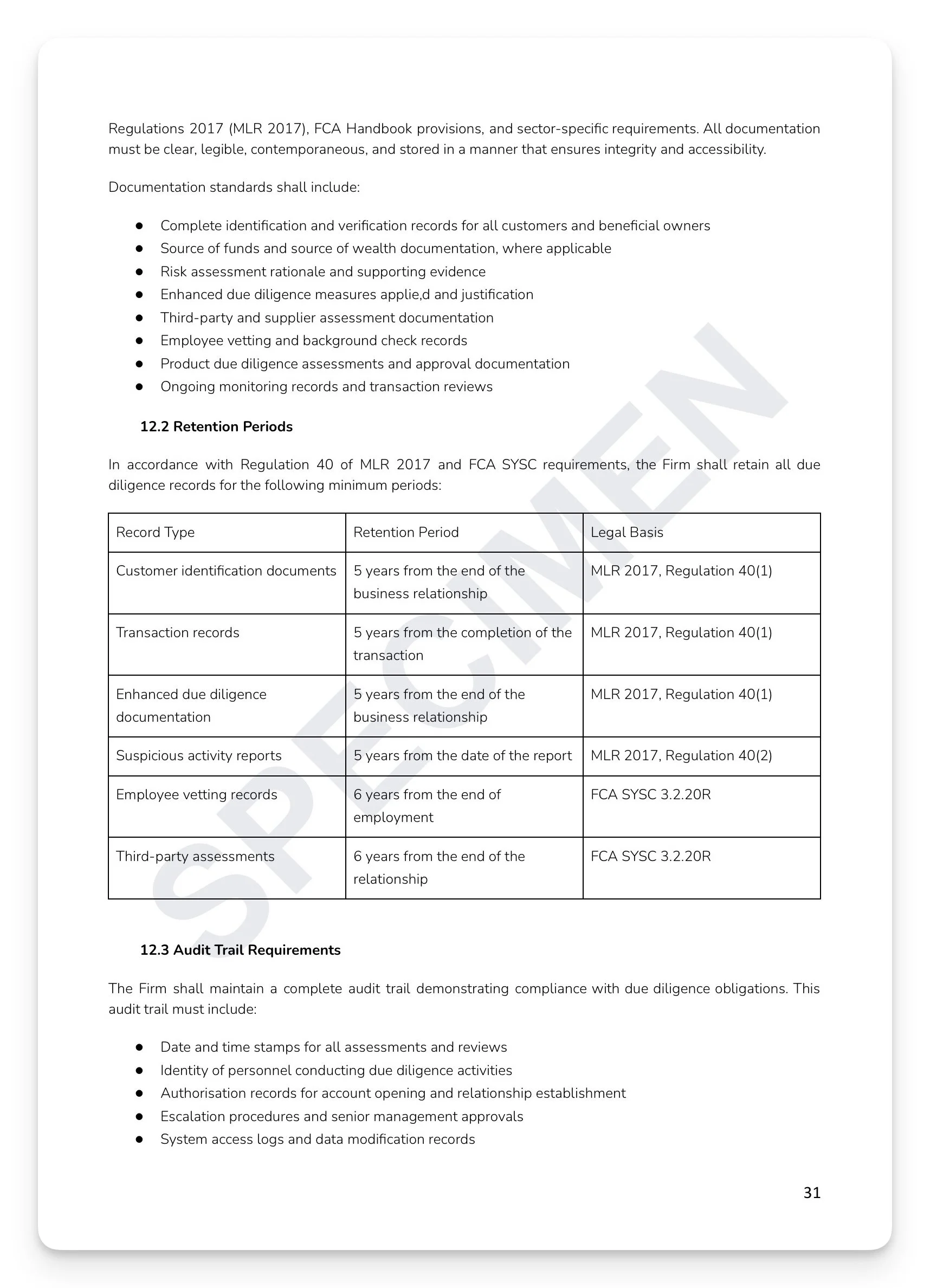

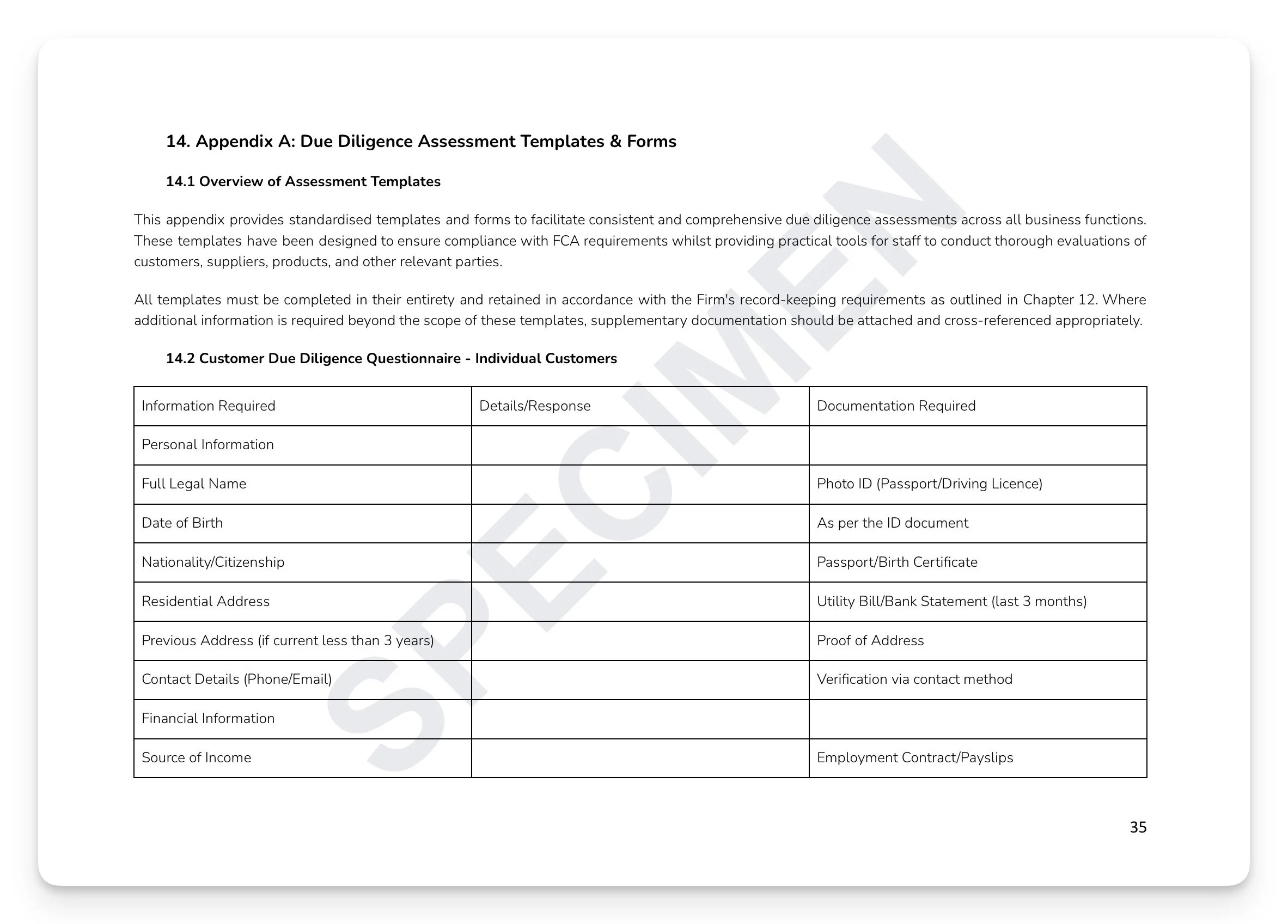

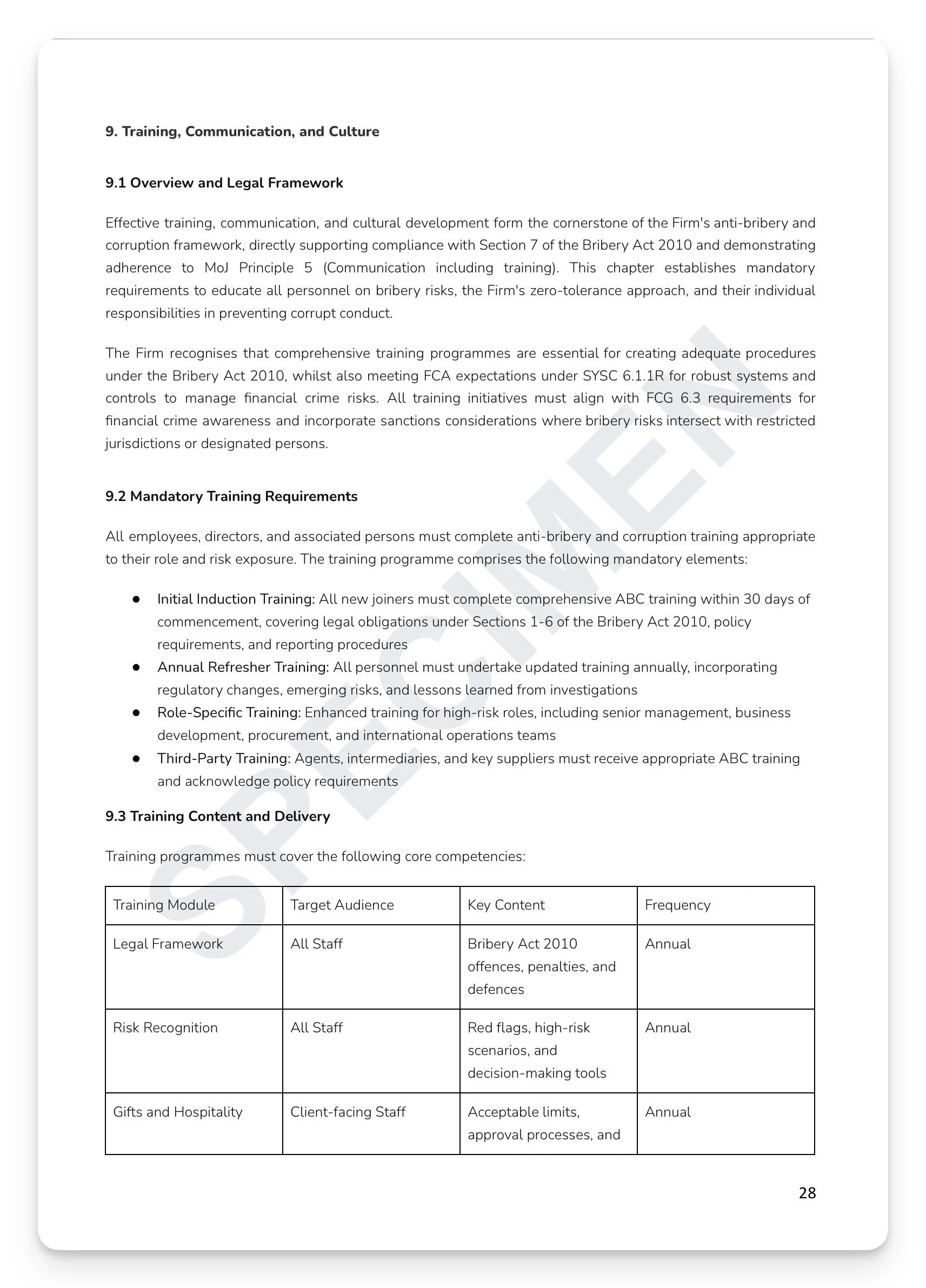

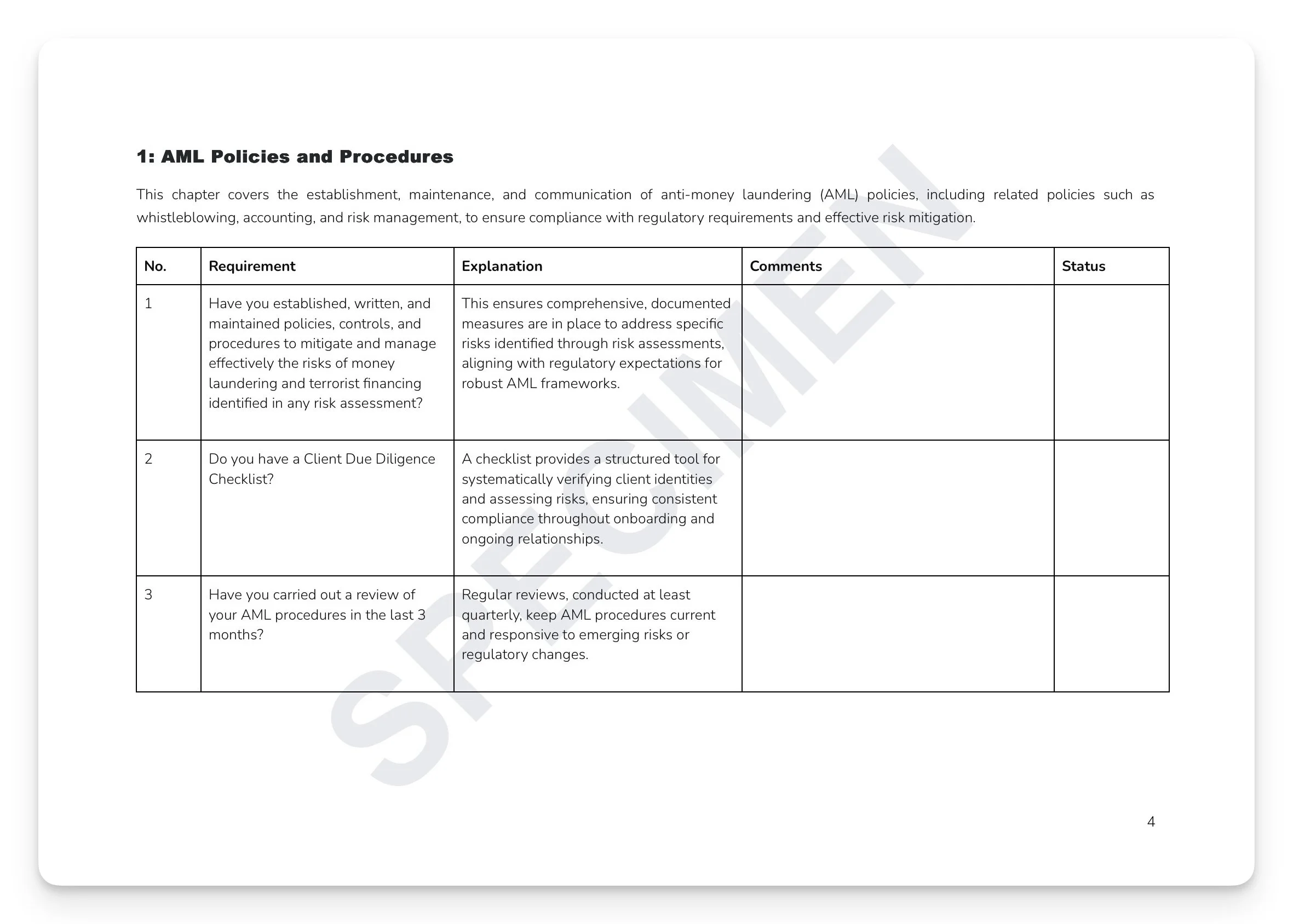

AML policies and procedures: 19 requirements covering policy completeness, approval, and review cycles — with MLRO and Nominated Officer governance covering appointment, fit and proper assessment, and accountability framework

Staff AML training programme: 31 requirements covering monthly sessions, role-specific content, assessment tests, induction, and refresher training — plus 27 employee screening requirements covering pre-employment checks, CRB, credit checks, and conflicts of interest

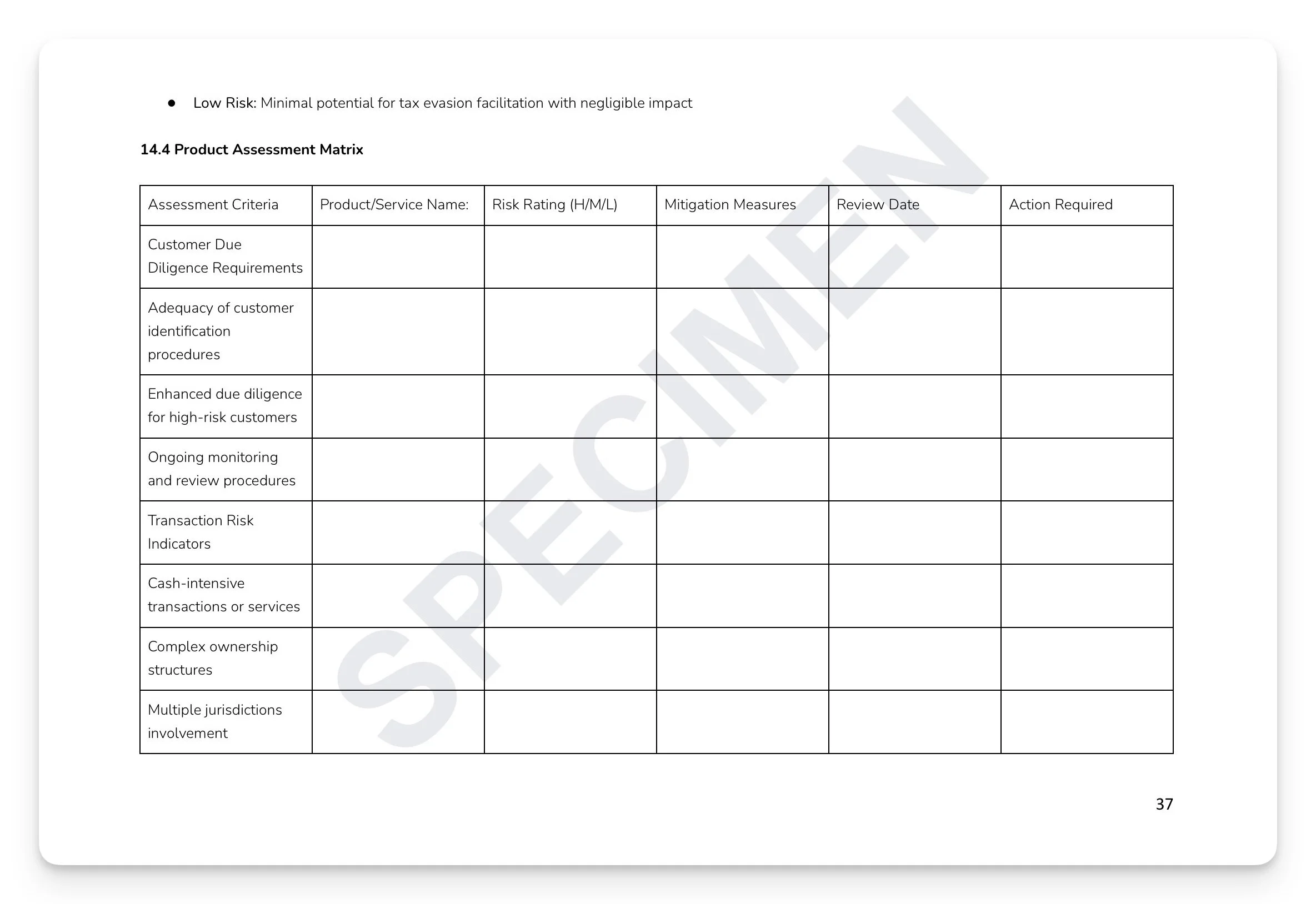

Financial crime risk assessment: 48 requirements covering customer risk profiling, transaction factors, FATF jurisdictions, sanctions risk, bribery and corruption risk, and horizon scanning

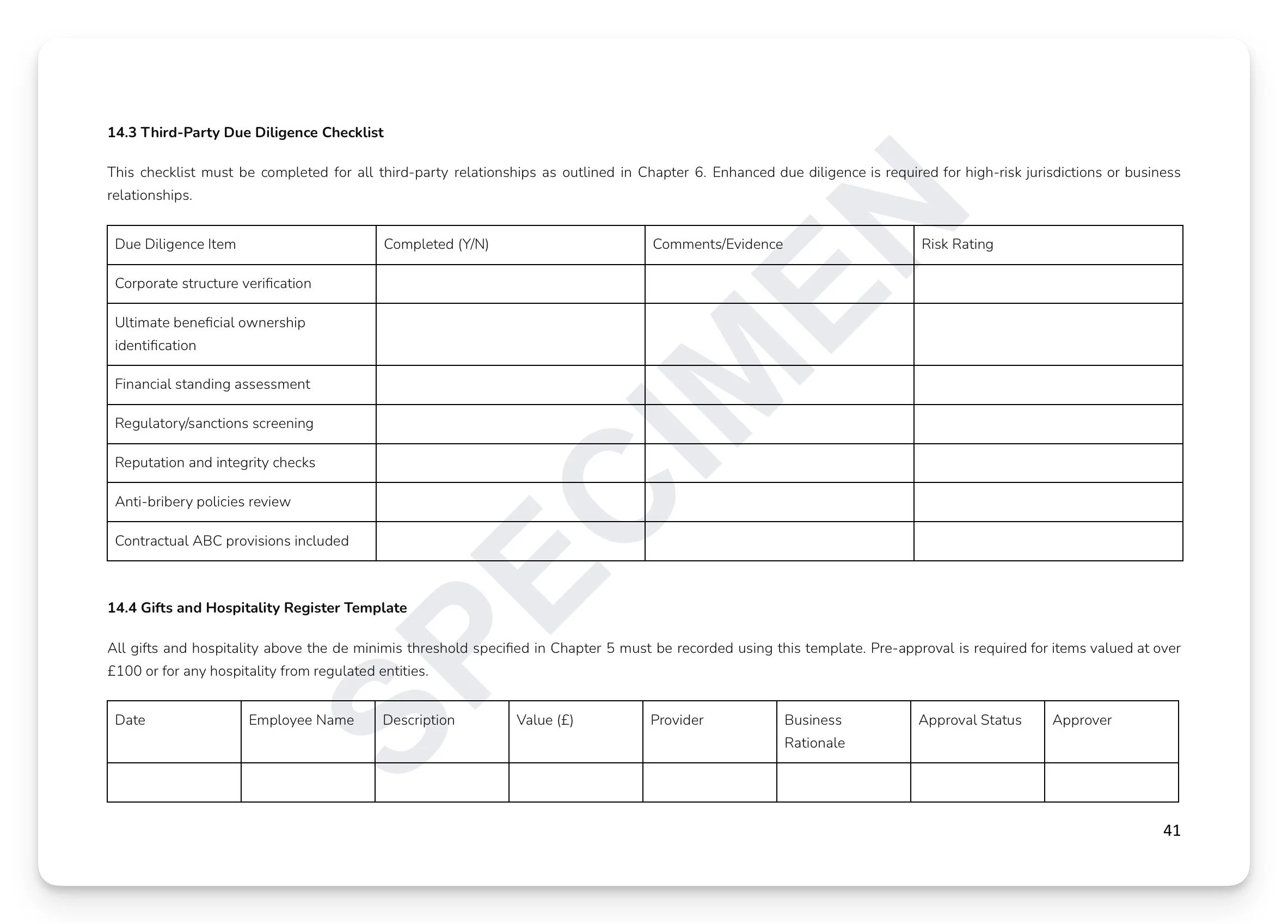

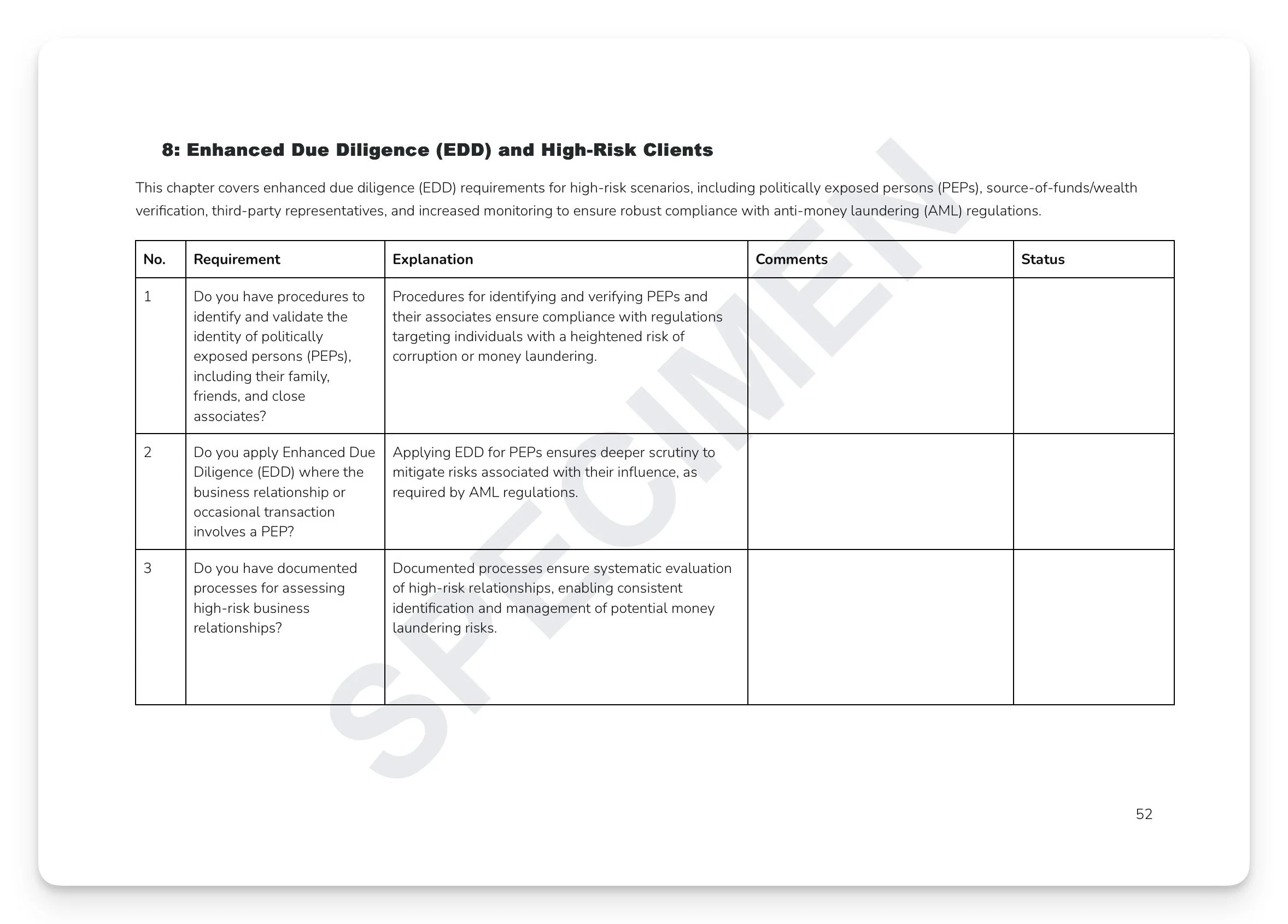

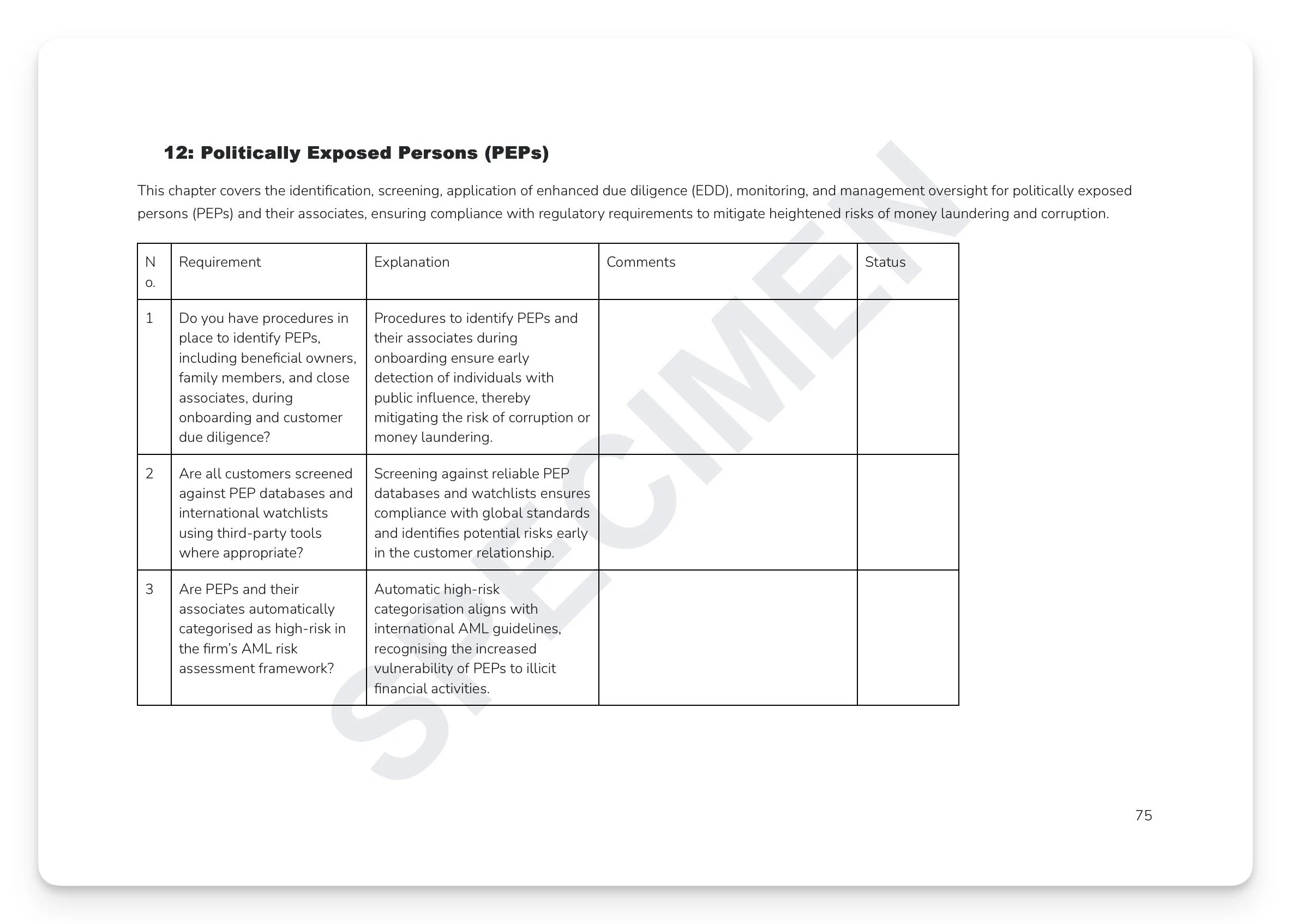

Customer Due Diligence and EDD: 19 CDD requirements covering identification, verification, and ongoing monitoring — plus 21 EDD requirements covering PEPs, source of funds and wealth, and third-party representatives

Sanctions compliance: 166 requirements covering SAMLA, OFSI, FCA SYSC 6.3, screening tool calibration, beneficial ownership, asset freezing, and vendor oversight

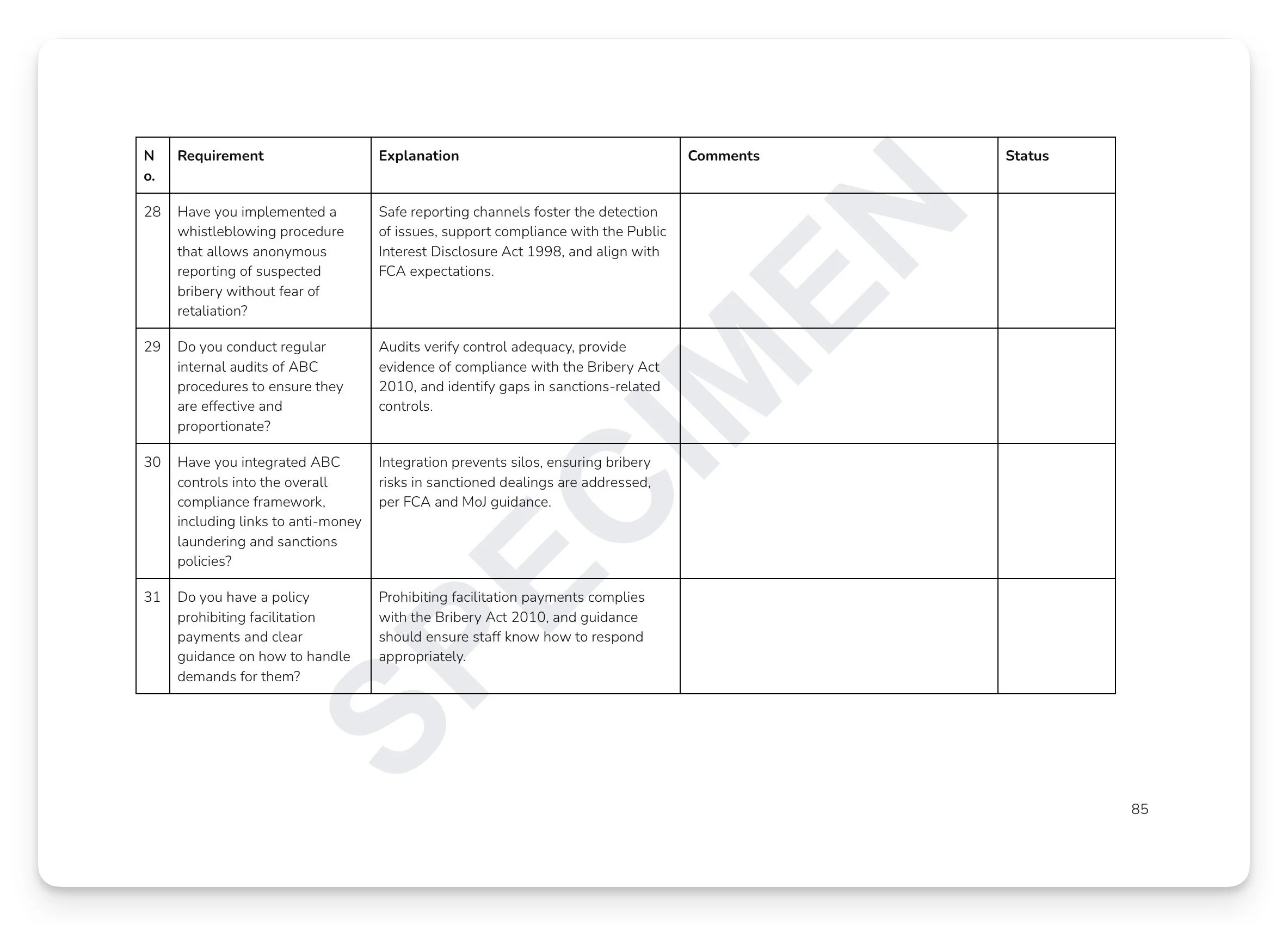

Anti-Bribery and Corruption programme: 85 requirements covering Bribery Act 2010, gifts and hospitality register, facilitation payments, whistleblowing, and breach response

Each requirement includes a plain-English explanation of why it matters and a status and comments column for audit tracking

+ much more

Who is this for?

MLROs, Compliance Officers, internal audit teams, and senior management at FCA-regulated and HMRC-supervised firms conducting structured AML programme reviews — quarterly for internal use, annually for the MLRO report, or ahead of regulatory visits.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Your AML programme is only as strong as your last honest audit. When did you last do one? The FCA doesn't just want to see policies — it wants evidence you've tested them. Most firms conduct informal reviews when something goes wrong. Few have a structured, documented audit process that systematically tests every element of their AML and financial crime framework and produces the evidence a regulator can inspect. Over 300 requirements. One document. No gaps.

What's included:

AML policies and procedures: 19 requirements covering policy completeness, approval, and review cycles — with MLRO and Nominated Officer governance covering appointment, fit and proper assessment, and accountability framework

Staff AML training programme: 31 requirements covering monthly sessions, role-specific content, assessment tests, induction, and refresher training — plus 27 employee screening requirements covering pre-employment checks, CRB, credit checks, and conflicts of interest

Financial crime risk assessment: 48 requirements covering customer risk profiling, transaction factors, FATF jurisdictions, sanctions risk, bribery and corruption risk, and horizon scanning

Customer Due Diligence and EDD: 19 CDD requirements covering identification, verification, and ongoing monitoring — plus 21 EDD requirements covering PEPs, source of funds and wealth, and third-party representatives

Sanctions compliance: 166 requirements covering SAMLA, OFSI, FCA SYSC 6.3, screening tool calibration, beneficial ownership, asset freezing, and vendor oversight

Anti-Bribery and Corruption programme: 85 requirements covering Bribery Act 2010, gifts and hospitality register, facilitation payments, whistleblowing, and breach response

Each requirement includes a plain-English explanation of why it matters and a status and comments column for audit tracking

+ much more

Who is this for?

MLROs, Compliance Officers, internal audit teams, and senior management at FCA-regulated and HMRC-supervised firms conducting structured AML programme reviews — quarterly for internal use, annually for the MLRO report, or ahead of regulatory visits.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7