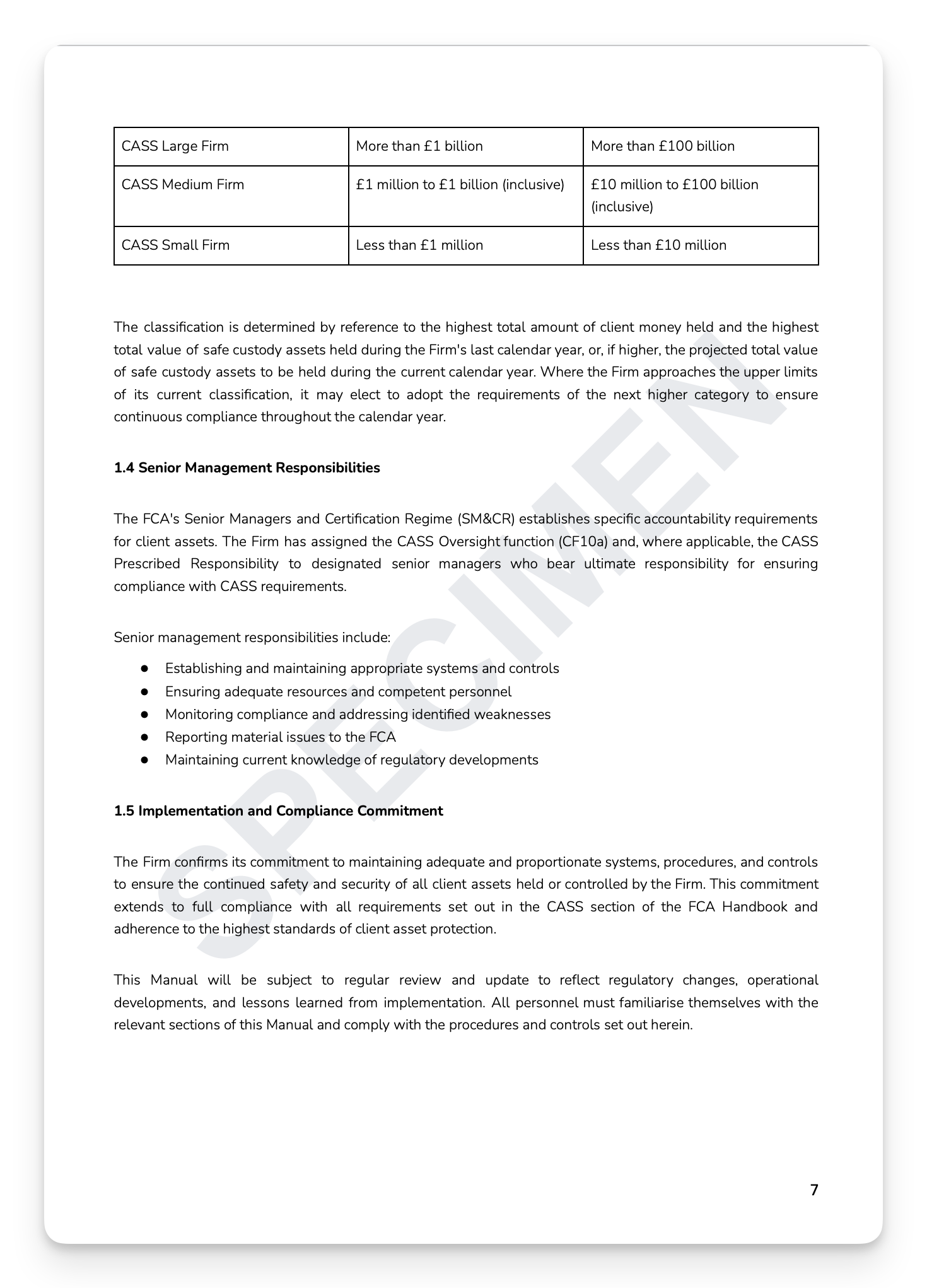

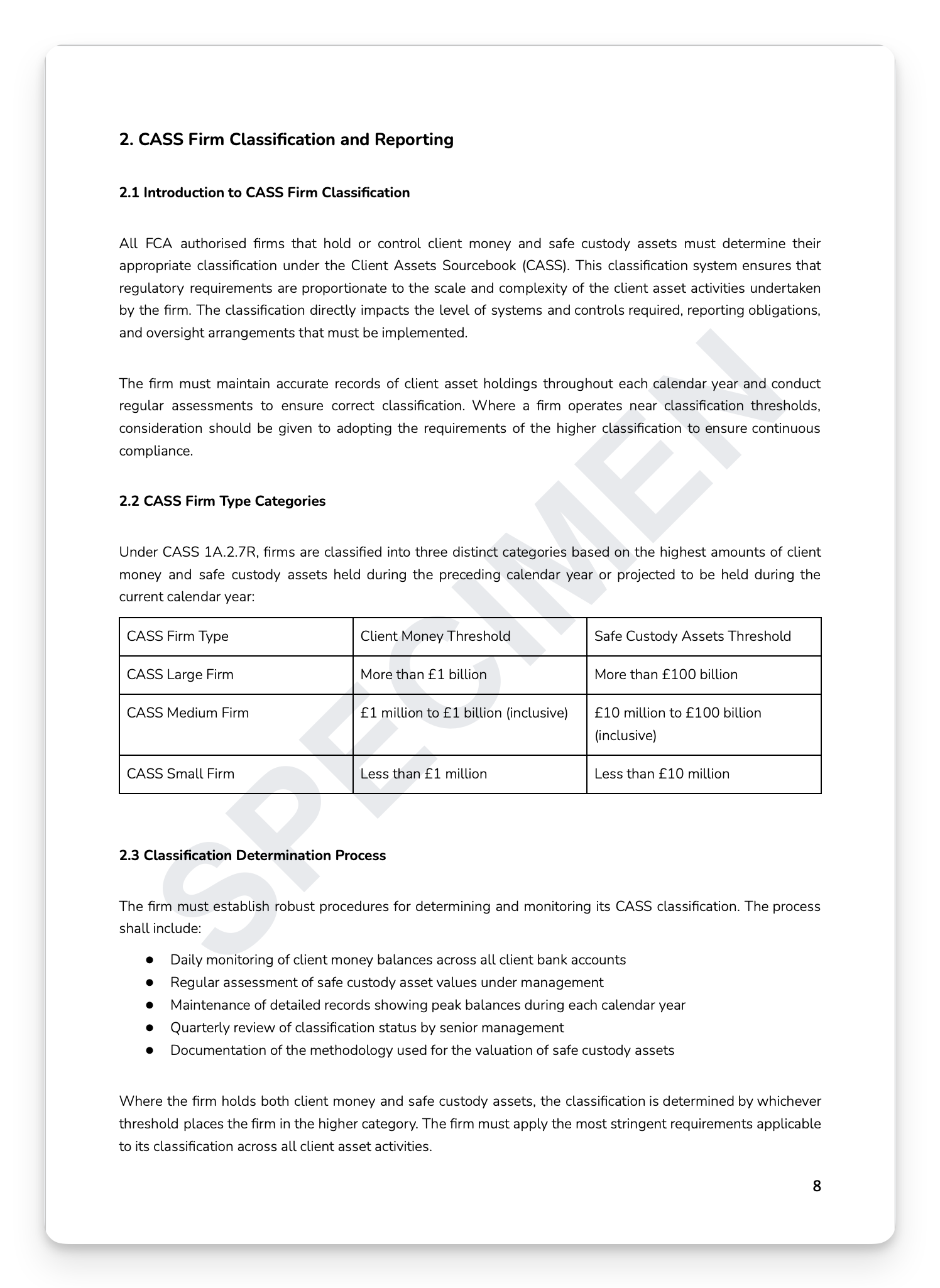

Client categorisation under COBS 3 isn't an admin exercise — it's the foundational regulatory decision that determines which conduct obligations apply to every interaction with every client. Mis-categorise a retail client as professional and you don't just have a categorisation failure — you simultaneously inherit suitability, appropriateness, disclosure, best execution, and product governance breaches for every service you subsequently provided. The FCA's supervisory work consistently finds the same failures: inadequate elective professional assessments, missing written warnings, and documentation that can't withstand scrutiny. The FCA doesn't wait.

What's included:

Full regulatory mapping: COBS 3, COBS 2 & 6, COBS 9A, COBS 10A, COBS 11.2A, COBS 16A, PROD 3, SYSC 9 & 10, and MiFID II

Complete category framework: Retail (default), Per Se Professional, Elective Professional, Per Se ECP, and Elective ECP — with full definitional precision

Elective Professional opt-up procedure: quantitative assessment (portfolio €500k+, 10+ transactions/quarter, 1 year financial sector experience), written request, written warning, and documented consent

Notification requirements: timing, content, durable medium, and plain English — prominently disclosed before any designated investment business

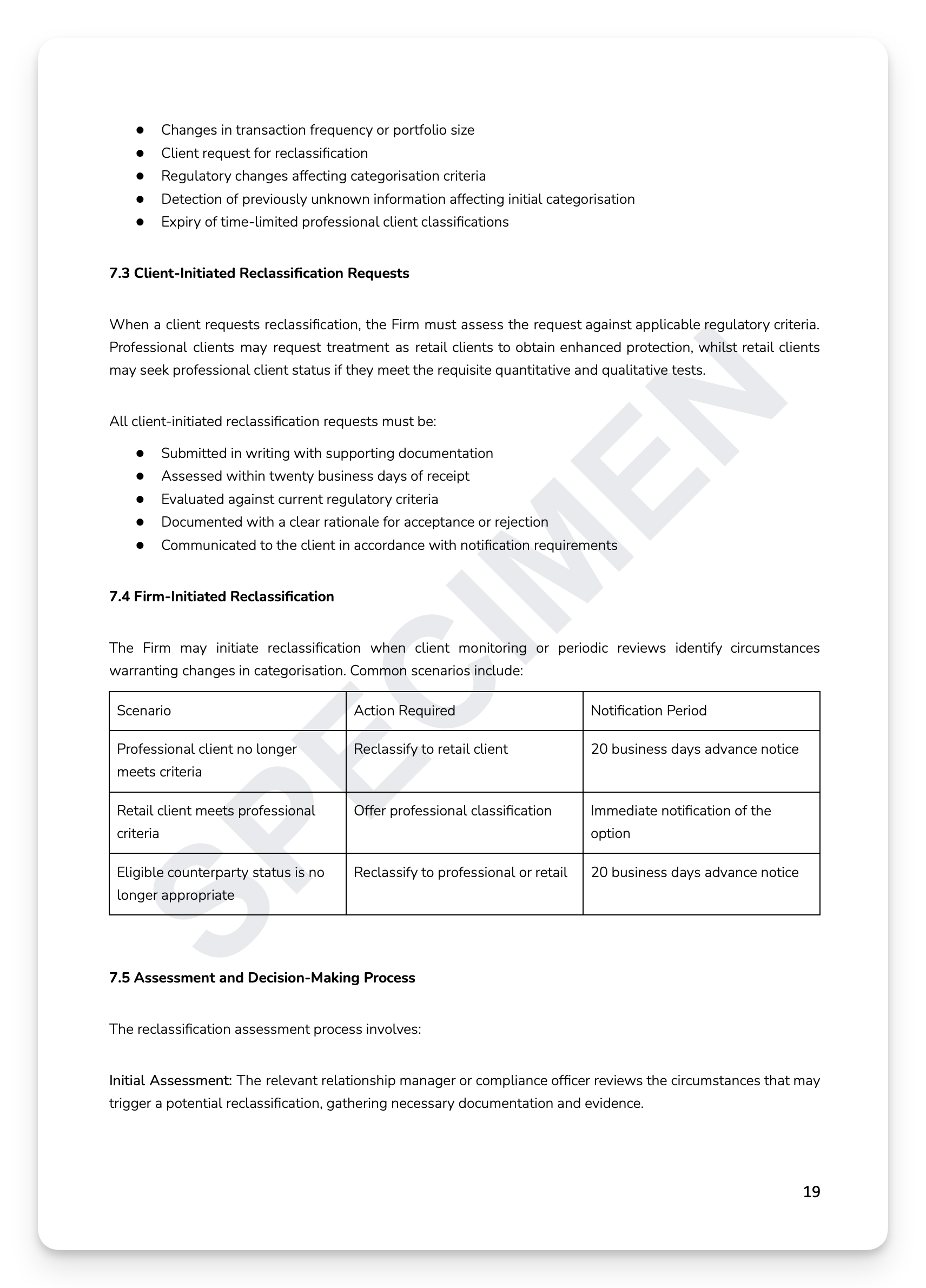

Eight reclassification triggers: 20-day assessment timelines, documented rationale, and advance notice requirements

Downstream regulatory interaction matrix: how categorisation flows into suitability, appropriateness, disclosure, best execution, and product governance

Compliance monitoring matrix: monthly file sampling, quarterly categorisation testing, semi-annual system controls verification, and annual training assessment

+ much more

Who is this for?

Compliance Officers, Heads of Investment Services, SMF holders, and relationship managers at FCA-authorised investment firms who need a complete, board-approved Client Categorisation Policy that is evidenced, defensible, and right.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Client categorisation under COBS 3 isn't an admin exercise — it's the foundational regulatory decision that determines which conduct obligations apply to every interaction with every client. Mis-categorise a retail client as professional and you don't just have a categorisation failure — you simultaneously inherit suitability, appropriateness, disclosure, best execution, and product governance breaches for every service you subsequently provided. The FCA's supervisory work consistently finds the same failures: inadequate elective professional assessments, missing written warnings, and documentation that can't withstand scrutiny. The FCA doesn't wait.

What's included:

Full regulatory mapping: COBS 3, COBS 2 & 6, COBS 9A, COBS 10A, COBS 11.2A, COBS 16A, PROD 3, SYSC 9 & 10, and MiFID II

Complete category framework: Retail (default), Per Se Professional, Elective Professional, Per Se ECP, and Elective ECP — with full definitional precision

Elective Professional opt-up procedure: quantitative assessment (portfolio €500k+, 10+ transactions/quarter, 1 year financial sector experience), written request, written warning, and documented consent

Notification requirements: timing, content, durable medium, and plain English — prominently disclosed before any designated investment business

Eight reclassification triggers: 20-day assessment timelines, documented rationale, and advance notice requirements

Downstream regulatory interaction matrix: how categorisation flows into suitability, appropriateness, disclosure, best execution, and product governance

Compliance monitoring matrix: monthly file sampling, quarterly categorisation testing, semi-annual system controls verification, and annual training assessment

+ much more

Who is this for?

Compliance Officers, Heads of Investment Services, SMF holders, and relationship managers at FCA-authorised investment firms who need a complete, board-approved Client Categorisation Policy that is evidenced, defensible, and right.

How it works

Step 1 — Read it. Every section exists for a reason, grounded in a specific regulatory obligation.

Step 2 — Understand it. Map the content against your current practices. Identify where you're strong and where gaps exist.

Step 3 — Make it yours. Tailor the language to reflect how your organisation actually operates. A policy that sounds like your firm is a policy your people will follow.

Step 4 — Take ownership. Assign clear accountability — Board approval, named SMF holder, designated policy owner. A policy without an owner is a liability, not an asset.

Step 5 — Operationalise it. Embed the policy into your governance calendar, training programme, and annual review cycle. This is where compliance becomes culture.

Or, get this free with RegTechPRO

Access this alongside the full compliance policy library — SM&CR, COBS, AML, Consumer Duty, GDPR, and more — for a fraction of the cost of consultancy.

View RegTechPRO pricing and packages →

Image 1 of 7

Image 1 of 7

Image 2 of 7

Image 2 of 7

Image 3 of 7

Image 3 of 7

Image 4 of 7

Image 4 of 7

Image 5 of 7

Image 5 of 7

Image 6 of 7

Image 6 of 7

Image 7 of 7

Image 7 of 7